LOS ANGELES, Oct. 31, 2013 /PRNewswire/ -- Legion Partners Asset Management, LLC ("Legion Partners"), together with IRS Partners No. 19, L.P. and certain other stockholders of RCM Technologies, Inc. (NASDAQ: RCMT), which has nominated two director nominees to the Board of Directors of RCM at the 2013 annual meeting of stockholders, today issued the following letter to all stockholders:

October 31, 2013

Dear Fellow RCM Technologies, Inc. Stockholders:

INTERESTS OF STOCKHOLDER GROUP LED BY LEGION PARTNERS ARE DIRECTLY ALIGNED WITH ALL RCM STOCKHOLDERS

Do Not be Misled by RCM's Recent Cosmetic Changes

Please Sign and Return the Enclosed GOLD Proxy Card Today to Support Truly Independent Directors Committed to Maximizing the Value of Your Investment

Legion Partners Asset Management, LLC ("Legion Partners"), together with IRS Partners No. 19, L.P. ("IRS Partners") and several others, have formed a group which collectively is the largest stockholder of RCM Technologies, Inc. (NasdaqGM: RCMT), referred to herein as "RCM" or the "Company." Our group has combined ownership of approximately 13.3% of the outstanding shares of RCM. We have nominated two independent directors for election to the Board of Directors of RCM (the "Board") at the 2013 annual meeting of stockholders, scheduled to be held on December 5, 2013 (the "2013 Annual Meeting"), due to our serious concerns with the perennial financial deterioration of the Company over the past decade. In addition to corporate profits in free-fall, we are alarmed by the Company's abysmal capital allocation track record and poorly aligned compensation and corporate governance practices, including, among other things, the granting of upwards of $6.1 million in severance to Leon Kopyt, the Company's Chairman and CEO, if even one of our nominees is elected to the Board and he is terminated without cause or leaves for good reason. It is unfortunate to see RCM's Board and management resort to this level of entrenchment—effectively allowing them to hold the Company hostage by curtailing stockholders' right to democracy through the threat of Mr. Kopyt's platinum parachute.

In an effort to look responsive to stockholders, the Board has recently adopted some corporate governance reforms based on the proposals we submitted to the Company and intended to bring before the 2013 Annual Meeting. As a result of our repeated calls to return capital to stockholders, the Company announced a special dividend and a stock buy. We urge stockholders not to be misled. The Board has acted only when faced with the prospect of a proxy contest and pressure from its largest stockholder to make these changes. While we believe there is significant value to be unlocked at RCM, we believe such value can only be unlocked with immediate change to the status quo, starting with the election of our two highly-qualified independent director nominees Roger H. Ballou and Bradley S. Vizi.

- Operations/Strategy—Roger H. Ballou is a retired executive with over 30 years of industry experience, including almost a decade as the CEO of RCM's closest public competitor, CDI Corp. Mr. Ballou was also instrumental in turning around and building several businesses, including Alamo Rent-a-Car and American Express's Travel Services Group.

- Stockholder Value/Accountability—Bradley S. Vizi, a founder of Legion Partners, is a public and private equity investor whose investment background encompasses capital allocation, corporate governance and executive compensation. As a member of the stockholder group, led by Legion Partners, with a combined ownership of approximately 13.3% of the outstanding shares of RCM, Mr. Vizi has significant "skin in the game" to promote greater accountability and maximize stockholder value.

We are frustrated with the Board's readiness to waste stockholder capital to engage in an election contest with us. Despite the Board's mischaracterization of our settlement discussions regarding the timing to declassify the Board (which was our initiative in the first place), we were amenable to declassifying the Board at the 2013 Annual Meeting if the Company in turn agreed that all directors would stand for re-election to serve one-year terms at the 2014 annual meeting of stockholders (not just our two nominees). We note that while the Company has agreed to declassify the Board at the 2013 Annual Meeting, only two director seats are up for election at the 2013 Annual Meeting and the other incumbent directors who were previously appointed to three-year terms (including one director who was appointed by the Board mid-2013 and has never stood for election and a vote of stockholders) will continue to serve until the end of their terms, which expire in 2014 and 2015.

We Believe the Continued Decline in RCM's Profits to be Cause for Significant Concern and Immediate Action

The current Board and management team have overseen a decline in sales from $214.2 million in 2007 to $155.5 million in the last twelve-month period ending June 29, 2013, a drop of approximately 27%. Over the same period, EBITDA (operating earnings excluding depreciation and amortization) has declined from $11.6 million to $7.3 million, a drop of approximately 37%. The Company's long-term performance demonstrates an even more alarming trend of deteriorating financials and value destruction. From 2000 through the last twelve months ending June 29, 2013, the Company's sales have declined from $305.4 million to $155.5 million, or approximately 49%. Over the same period, EBITDA has decreased from $23.6 million to $7.3 million, or approximately 69%. It is important to note that the decline in revenue and EBITDA would be even more substantial if the additive impact of failed acquisitions were taken into account. We urge stockholders to support the election of our director nominees before the Company falls into an irreversible state of disrepair.

Click below to view graph:

(Photo: http://photos.prnewswire.com/prnh/20131031/SF08110-a)

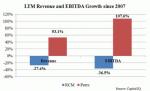

RCM Has Consistently Underperformed Its Peers

When considering RCM's financial results against its peer set1, the case for change is even more evident. On average, peers have significantly improved their performance over the past five years vs. RCM whose EBITDA has declined by more than one-third. Since 2007, the peer set has grown its revenue and EBITDA 53% and 108%, respectively; while, RCM's revenue and EBITDA have declined 27% and 37%, respectively. Furthermore, the Company's average return on invested capital over the last five years of 5.3% is approximately 42% below its peer set at 9.3%. This dismal absolute and relative financial performance serves as a clarion call for investors to take action by electing our nominees who are committed to maximizing the value of RCM for all stockholders.

Click below to view graph:

(Photo: http://photos.prnewswire.com/prnh/20131031/SF08110-b)

We Believe a Disciplined Approach to Capital Allocation Is Essential to Stop the Hemorrhaging of Stockholder Value

In addition to the prolific value destruction reflected in RCM's income statement, the incumbent management team and members of the Board have overseen an ill-advised acquisition strategy that has resulted in nearly $150 million of write-offs associated with goodwill and other intangibles from 2000 to 2008, despite spending approximately $160 million on acquisitions since 1997. In other words, the Company has written off nearly three times (3x) its current enterprise value (and five times (5x) the enterprise value from when we began accumulating shares and engaging in discussions with the Company in 2011) with nothing to show for it but a 69% decline in EBITDA. Furthermore, when taking into account these write-offs, the Company has failed to earn its cost of capital in any single year going back to 2000 as demonstrated by disappointing historical returns on invested capital.

Click below to view graph:

(Photo: http://photos.prnewswire.com/prnh/20131031/SF08110-c)

When we first met with the Company in April 2011, we raised the concept of a special dividend in light of the free cash flow the business was generating, its over-capitalized balance sheet, and the recurring absence of total return for investors. At the time, approximately 40% of the Company's market cap was in cash and the Board and management had no history of returning cash to stockholders in the form of a dividend. We explained that cash on the balance sheet of companies with questionable capital allocation track records is often valued at or near zero by the market and, in some instances, may actually demonstrate a negative value. Only after several such discussions with us over an 18-month period did the Company finally pay its first cash dividend to stockholders in December 2012. With the prospect of an election contest in roughly five weeks, the Board has now announced, on October 28, 2013, a $5 million stock buy-back program as a means to return capital to stockholders. Once again, we see evidence of a Board slow to act unless pressured by a significant stockholder advocating for change.

The current Board has proven incapable of delivering returns to stockholders. We believe a reconstituted Board committed to a disciplined, well-vetted approach to capital allocation is an essential remedial step to prevent repeating past woes and to maximize the value of RCM going forward. However, a commitment toward driving ROIC to higher levels and enhancing stockholder value must go beyond the regular evaluation of alternative uses of capital and serve as the cornerstone of a well-designed compensation program.

Misguided Compensation Practices Demonstrate Asymmetric Potential Payoff to Management at the Cost of Stockholders

We believe RCM's compensation practices are a hallmark of a company where the interests of stockholders take a back seat to those of the Board and management team. Despite poor operating performance, on December 27, 2012, the Company adopted executive severance agreements for Rocco Campanelli, the Company's Executive Vice President, and Kevin Miller, the Company's Chief Financial Officer. These agreements provide for, among other things, severance upon termination related to a change in control and a change in control payment, in each case equal to two (2) times each executive's respective annual base salary and bonus. These agreements are in addition to the Company's termination benefits agreement with Leon Kopyt, the Chairman, President and Chief Executive Officer of the Company, which provides for, among other things, a severance package consisting of five years of annual base salary and bonus in addition to however many years are remaining on his employment agreement if he is terminated (without cause) or if he resigns for good reason following a change in control. If Mr. Kopyt were terminated in 2013, he would be entitled to a payment representing approximately eight years of salary and bonus (including tax gross up and other benefits) under his termination benefits agreement.

The definition of "change in control" under Kopyt's termination benefits agreement (as well as Mr. Kopyt's severance agreement discussed below) includes the appointment of just one nominee to the Board in connection with a proxy contest. In other words, if stockholders choose to exercise their right of democratic process which results in the election of just one stockholder-nominated director to the Board, and Mr. Kopyt is thereafter terminated (without cause) or leaves the Company for "good reason," he is entitled to receive a windfall payout of more than $6 million or roughly 10% of the current enterprise value of RCM (20% at the beginning of our accumulation of shares and engagement in discussions with the Company).

In addition to this termination benefits agreement, the Board has also adopted a separate severance agreement for Mr. Kopyt if he is terminated (without cause) or leaves for "good reason." Under his severance agreement, "good reason" includes the right of Mr. Kopyt to resign at his discretion during the one-month period commencing twelve (12) months following a "change in control." As a result, if we are successful in electing just one of our director nominees to the Board, Mr. Kopyt would have the ability to wait one year, abandon his position as President and CEO for any or no reason whatsoever, and collect $4.5 million under his severance agreement (calculated as of December 29, 2012).

It is deeply disturbing that the Board would approve executive severance arrangements for Messrs. Campanelli and Miller, when the projected cash payment calculated as of December 29, 2012 under the Kopyt's termination benefits agreement alone is approximately 200% of the Company's net income for fiscal 2012. We do not believe these pay packages are reasonable or warranted given the Company's poor financial performance and dismal return on capital to stockholders and we are not alone in our belief. In 2010, Institutional Shareholder Services ("ISS"), a leading proxy advisory firm, recommended WITHHOLD votes from the Company's current director nominee, Robert B. Kerr, for serving on the Company's compensation committee that has maintained "executive agreements that contain overly generous severance payments." ISS considers outsized change-in-control provisions problematic as they can potentially lead to packages that are so generous that they fail to hold executives accountable for poor performance. Noting the Company's "problematic pay practices policy," ISS stated, "[it] finds [these] outsized severance packages to be concerning," and recommended WITHHOLD votes for Mr. Kerr and also existing Board member Lawrence Needleman, who the Board recently announced would not be standing for re-election at the 2013 Annual Meeting.

Recent Board Actions Set Disturbing Precedent to Disenfranchise Stockholders

In a desperate attempt to insulate itself from change, the Board has undertaken a disturbing set of actions to disenfranchise stockholders:

- The current Board delayed the 2013 Annual Meeting by six months in response to our nomination of two director candidates and three business proposals. By delaying the 2013 Annual Meeting by six months and scheduling it in the middle of the 2013 holiday season, we believe the Board is attempting to impede stockholders' right to a democratic process. When coupled with the fact that special meetings of stockholders may only be called by stockholders holding at least 80% entitled to vote at such meeting and stockholders can only act by unanimous written consent, the Board has made it particularly difficult for stockholders to hold the Board accountable in a timely manner.

- Within just weeks of receiving our nominations and business proposals, the current Board adopted a shareholder rights plan, or poison pill, with a 15% ownership limitation, just above our group's then current ownership in the Company of 12.8% of the outstanding shares, and without stockholder approval. Notwithstanding its prior announcement that it would submit the rights plan for ratification at the 2013 Annual Meeting (an announcement prompted by our public criticism of the rights plan), the Board is once again disenfranchising stockholders by not allowing stockholders to vote on the plan. With a termination date in January 2014, just one month after the 2013 Annual Meeting, we hope that the Board will not act unilaterally to extend the rights plan, when it currently has the opportunity to let stockholders approve the plan and any extension thereto at the 2013 Annual Meeting.

Moreover, the Board maintained a classified Board for the past 18 years and only recently agreed to destagger the Board after we, in private and public communications, advocated for the Board to be declassified. Do not be misled by the Company's mischaracterizations of our settlement discussions alleging that we sought to delay the implementation of our very own proposal to declassify the Board. To set the record straight - we were amenable to the implementation of the declassification proposal at the 2013 Annual Meeting if the Company in turn agreed that all directors would stand for re-election to serve one-year terms at next year's annual meeting of stockholders (not just our 2 director nominees). Ironically, the Board not only failed to disclose the settlement discussions surrounding our alternative proposal, but also failed to disclose its blatant rejection thereof. The Board also failed to disclose that it requested a covenant not to sue and a release of all claims as a condition to its settlement proposal. What could the Board be so worried about to demand these conditions? Do they have something to hide that they need to request not only a covenant not to sue but also a release of all claims? The Board's efforts to now paint a different picture is a sad attempt to divert stockholders attention from the real issues at hand – that being the historical underperformance of this Company and the Board's lack of accountability to stockholders.

The Board Needs an Independent Chairman to Hold Management Accountable

Given this Board's recent actions to disenfranchise stockholders, its approval of outrageous compensation packages for senior management, and the Company's significant underperformance, all led under Chairman and CEO, Leon Kopyt, we find it even more crucial than ever that the Board adopt a policy that the Board's Chairman be an independent director according to the definition set forth in the NASDAQ listing standards. The Company's proposal to appoint a lead independent director does not go far enough, particularly since its choice to serve in such role is Robert B. Kerr, a director for over 19 years and the second longest serving director on the Board (behind Mr. Kopyt himself). How independent can Mr. Kerr be given his long tenure with the Company?

We urge stockholders to approve our non-binding proposal to separate the roles of Chairman and CEO at the 2013 Annual Meeting. If approved, our director nominees, if elected, will remain committed to further corporate governance reforms promoting greater stockholder accountability at the Company.

The Board's Cosmetic Changes Do Not Go Far Enough

While the Board may have made some cosmetic changes to its corporate governance (by declassifying the Board and providing that directors be elected by a majority vote standard, in each case based on our proposals that we intended to bring before the 2013 Annual Meeting), we caution stockholders that given the reactionary nature and long history of poor corporate governance practices, the Company's move appears to be an attempt to merely whitewash its dismal corporate governance structure. The Company still maintains a number of unfriendly stockholder policies, including the inability of stockholders to effectively call a special meeting of stockholders (given the 80% threshold) or act by written consent (given the unanimous threshold), the inability of stockholders to remove directors without a supermajority vote of 2/3rds of stockholders, and the inability of stockholders to fill director vacancies even upon removal by stockholders. Consider further that not until this year, did the Company establish a formal nominating and corporate governance committee, despite ISS recommending WITHHOLD votes from directors in each of the last two annual meetings of stockholders for lack of a nominating committee and, with respect to Richard D. Machon in 2012, for serving as a non-independent member of key board committees. ISS has noted that the presence of non-independent directors on key committees may diminish a committee's ability to oversee management objectively. Clearly this has been the case. We note that if the Company had adopted a majority vote standard for the election of directors back in 2011, Leon Kopyt would not have been re-elected to the Board, as 66% of stockholder WITHHELD their votes from him. Furthermore, we question the Company's last minute appointment of Michael E.S. Frankel to the Board given the long standing track record of its 'hand-picked' nominees.

No Independent Director Holds Meaningful Share Ownership in the Company

We believe a culture focused on long-term value creation and stockholder accountability requires placing stockholder representatives on the Board who have a significant financial commitment to the Company along with relevant experience. This requirement ensures the proper alignment of interests between the Board and stockholders. Based upon our review of the Company's public filings, we believe as a group the independent members of the Board own just over 1% of the outstanding shares of the Company (excluding shares underlying stock option grants and similar awards). In fact, only one director, Maier Fein, has reported open market purchases of the Company's shares. We are concerned that the lack of significant actual equity ownership by the independent directors and the minimal real investment dollars they have at risk may contribute to a lack of commitment to maximizing stockholder value.

By contrast, Legion Partners and its constituents have invested approximately $9 million to accumulate approximately 13.3% of the Company's common stock, making it RCM's largest investor. We believe our substantial ownership not only results in optimal long-term alignment of interests with stockholders but also demonstrates our motivation to maximize the value of RCM for its stockholders.

Our Nominees Are Truly Independent and Will Act in Your Best Interest

Roger Ballou is an independent nominee with no commercial relationship with the Company or Legion Partners and its constituents. Bradley Vizi has no affiliation with RCM, other than his group's 13.3% ownership interest. Our nominees have strong relevant backgrounds, are highly regarded in their industries, and have the right mix of operating and financial experience to deliver value to all stockholders. Both bring unique perspectives and ideas that we believe will aid directly in the realization of value at RCM. Both of our nominees are "independent directors" as defined by the rules of the NASDAQ Stock Market.

We have no preconceived agenda or aspiration to acquire or otherwise control RCM, despite claims made by the Board and RCM's management team whose iron grip on the Company is in jeopardy. Not only does the Company's claim lack foundation, but it also lacks any semblance of precedent. We ask stockholders to disregard the Company's distorted chronology and outlandish conspiracy claims as nothing more than a 'Hail Mary' pass on behalf of the Board and management team, meant to divert attention away from the serious issues facing the Company and the Board's long, undeniable track record of stockholder neglect and value destruction.

We are seeking minority representation on the Board in an effort to protect the economic interest of all stockholders, which includes our own $9 million investment in RCM. If our nominees are elected to the Board, rest assured that they fully understand their fiduciary duties and will represent the interests of ALL stockholders.

If you have any questions, or need assistance in voting your shares, please call our proxy solicitor, Okapi Partners LLC, whose contact information is below. Thank you in advance for your support.

Sincerely,

Bradley S. Vizi

Managing Director

Legion Partners Asset Management, LLC

VOTE FOR CHANGE AT RCM -- PLEASE SIGN, DATE AND MAIL THE ENCLOSED GOLD PROXY CARD TODAY

OKAPI PARTNERS LLC

437 Madison Avenue, 28th Floor

New York, NY 10022

(212) 297-0720

Call Toll-Free at: (877) 566-1922

E-mail: info@okapipartners.com

If you have any questions, require assistance with submitting your GOLD proxy card or need additional copies of the proxy materials, please contact:

Okapi Partners LLC

(212) 297-0720

(877) 869-0171 (toll-free)

info@okapipartners.com.

1 CTG, PRFT, HCKT, AFAM, AGX, CDI

SOURCE Legion Partners Asset Management, LLC