LAS VEGAS, May 6, 2015 /PRNewswire/ -- MGM Resorts International (NYSE: MGM) today announced that it has sent a letter to shareholders in connection with its 2015 Annual Meeting to be held on May 28, 2015.

The full text of the letter is as follows:

May 6, 2015

Dear Fellow MGM Shareholders:

Your Board and management are focused on continuing to ensure MGM fulfills its full potential and delivers sustainable value to its shareholders. However, as you know, 0.38% shareholder Land & Buildings ("L&B") is trying to gain four seats on your Board, and as part of its campaign it has made many inaccurate and misleading statements about the Company, its Board and management. While we do not believe it is productive to address every mischaracterization and distortion made by L&B, we do feel it is very important that shareholders understand some key facts about your Board:

- We are ALWAYS receptive to any shareholder with a constructive view on how to create value

- We have for some time been actively evaluating all strategic initiatives for the Company, including a potential partial or total REIT strategy

- We are demonstrably committed to best corporate governance practices and are very proactive in our oversight of the Company to ensure it delivers sustainable value to shareholders

- We have ensured that your Company has performed very well against its actual peers and is extremely well positioned for future success

MGM HAS BEEN – AND CONTINUES TO – ACTIVELY EVALUATE ALL STRATEGIC INITIATIVES FOR THE COMPANY

As we have said on numerous occasions, your Board has proactively evaluated the REIT concept for many years and we are very thoroughly doing so again now. In the past we have decided not to pursue this strategy for a number of reasons. That said, we are acutely aware that our business and the markets in which we operate continuously evolve and it is crucial to our future success that we regularly evaluate all avenues to unlock value, which we are doing.

As such, your Board and management have engaged a team of industry leading investment bankers, legal advisors and tax consultants to once again complete a thorough review of a potential REIT conversion transaction for the Company. In recent weeks we announced the addition of Evercore Group L.L.C. to that team. MGM is a complex, global business and it will take some time to thoroughly and properly evaluate this opportunity, but we are actively doing so.

MGM'S OPERATING PERFORMANCE IS STRONG

MGM has delivered significant value to its shareholders, and when compared to its peers, MGM has performed well:

MGM has outperformed its gaming peers and the Dow Jones U.S. Gaming Index on a one and three-year basis. Since bottoming during the financial crisis, MGM has also significantly outperformed its gaming peers and the Dow Jones U.S. Gaming Index.

As of year end 2014 | Total Shareholder Returns | |||

1 Year | 3 Year | 5 Year | Mar-09 (2) | |

DJ U.S. Gaming Index | (18.8%) | 54.1% | 148.0% | 556.3% |

Gaming Peers Median Returns (1) | (17.7%) | 59.5% | 147.8% | 446.5% |

MGM Resorts International | (9.1%) | 105.0% | 134.4% | 940.2% |

(1) Gaming Peers include: LVS, WYNN, BYD, PENN (inclusive of GLPI), CZR and PNK | ||||

(2) TSR performance for the gaming peer stocks since MGM's stock bottomed on March 5, 2009 |

- MGM's EV/EBITDA 2014 multiple was about 10.5x, which is above the median industry multiple of 9.5x

EV / EBITDA | |||||||||||

2010 | 2011 | 2012 | 2013 | 2014 | 2015E | 2016E | |||||

Gaming Peer EBITDA Multiple | |||||||||||

MGM Resorts International | 17.0x | 12.1x | 10.9x | 11.4x | 10.5x | 12.0x | 11.1x | ||||

Las Vegas Sands Corp. | 20.3x | 13.0x | 13.5x | 15.4x | 10.2x | 12.1x | 11.5x | ||||

Wynn Resorts, Limited | 14.1x | 10.4x | 10.2x | 13.3x | 11.5x | 13.0x | 10.8x | ||||

Caesars Entertainment Corporation | NA | NA | 28.6x | 12.0x | 13.5x | 10.3x | 10.3x | ||||

Boyd Gaming Corporation | 10.9x | 9.1x | 12.5x | 8.9x | 7.8x | 8.6x | 8.2x | ||||

Penn National Gaming, Inc. | 7.8x | 8.1x | 10.8x | 2.7x | 7.5x | 7.3x | 6.4x | ||||

Pinnacle Entertainment, Inc. | 8.6x | 7.3x | 8.1x | 15.4x | 8.9x | 9.6x | 9.5x | ||||

Gaming Peer Median Multiple | 10.9x | 9.1x | 11.6x | 12.7x | 9.5x | 9.9x | 9.9x | ||||

MGM Relative Performance | 6.1x | 3.0x | (0.8x) | (1.3x) | 1.0x | 2.0x | 1.2x | ||||

Source: Company filings; FactSet | |||||||||||

- MGM's Adjusted Property EBITDA margins were a solid 24.5% in 2014, which is higher than the industry median

EBITDA Margins | |||||

2010 | 2011 | 2012 | 2013 | 2014 | |

MGM Resorts International | 17.8% | 22.3% | 21.8% | 24.0% | 24.5% |

Las Vegas Sands Corp. | 28.2% | 34.4% | 30.5% | 32.4% | 35.5% |

Wynn Resorts, Limited | 24.6% | 26.7% | 27.2% | 29.6% | 29.1% |

Penn National Gaming, Inc. | 23.7% | 25.4% | 23.5% | 22.6% | 9.8% |

Boyd Gaming Corporation | 18.4% | 18.9% | 16.9% | 20.0% | 21.1% |

Pinnacle Entertainment, Inc. | 18.3% | 20.7% | 22.0% | 18.2% | 25.2% |

Caesars Entertainment Corporation | 19.8% | 20.6% | 21.1% | 20.8% | 16.6% |

Gaming Peer Median | 21.7% | 23.1% | 22.7% | 21.7% | 23.2% |

MGM Relative Performance | (4.0%) | (0.8%) | (0.9%) | 2.3% | 1.3% |

Source: Company Management; company filings | |||||

- In L&B's latest presentation, it selectively chose to compare MGM to WYNN and LVS, but these are very different companies due to our varied geographic footprints, revenue sources and overall size

- Geographic footprint: MGM receives approximately 70% of its Adjusted EBITDA from the U.S., compared to <30% for WYNN and <10% for LVS – these are clearly different geographic footprints

- Revenue sources: Casino revenues represented 54% of MGM's 2014 gross revenue, as compared to 73% and 78% for WYNN and LVS, respectively

- Size: MGM's $12 billion equity value is comparable in scale to WYNN's $14 billion; however, it is considerably smaller than LVS's $44 billion

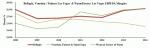

- A more relevant analysis would be on a property specific basis as Bellagio is more fairly compared to Wynn/Encore and Venetian/Palazzo in Las Vegas, and in this regard Bellagio has performed in line, if not better than, its peers

Source: Company filings

MGM HAS A HISTORY OF MAKING STRONG ROIC INVESTMENTS, HAS DRAMATICALLY IMPROVED ITS BALANCE SHEET & HAS FURTHER OPPORTUNITIES TO DE-LEVER

- History of strong ROIC investments:

- MGM China:

- MGM investment in MGM China is $341 million

- Distributions and dividends to date to MGM = $1.3 billion

- MGM owns 51% of MGM China's public market capitalization of $7.6 billion, equaling $3.9 billion in value to the Company

- MGM Detroit:

- Total spend on current MGM Detroit facility of $800 million

- MGM Detroit is generating stabilized Adjusted Property EBITDA of ~$150 million (reflects average over the trailing two years)

- ROIC: 19%

- Consistent market leader with over 40% market share

- MGM China:

- MGM has made significant progress in improving its balance sheet:

- Net leverage on the Company's wholly owned domestic resorts (restricted group) has decreased from 10.1x to 8x pro forma for the conversion of the convertible notes in April 2015. Consolidated net leverage pro-forma for the conversion of the notes is now less than 5x

- Significant improvements to credit profile, resulting in Moody's and S&P upgrading our corporate credit ratings by three levels to B2 / B+

- Reducing the cost of long-term bond issuances from 11.9% in 2009 to 6% in 2014

- MGM's Board has also been proactive in selling assets and de-risking its portfolio:

- Management sold: Golden Nugget, Primm, Laughlin, 50% of CityCenter, and Treasure Island

- Further opportunities to de-lever the balance sheet in the near term include:

- Regular dividend policy at MGM China and CityCenter

- Continued free cash flow growth

L&B LACKS CREDIBILITY & DOES NOT DESERVE REPRESENTATION ON MGM'S BOARD

L&B has made inaccurate and misleading claims about MGM's business, its Board and even L&B's own proposal. In determining whether to elect L&B's nominees to our diverse and experienced Board, we ask shareholders to consider the following:

Flawed Proposal – L&B's initial proposal was riddled with errors and inaccurate assumptions. We believe it was widely disregarded by Wall Street analysts and L&B had to significantly revise it.

To name just a few substantive revisions to L&B's plan:

- The high end of L&B's pro forma valuation of MGM was lowered by 40% from $55 in its initial proposal to $33 in its revised draft

- The MGM China dividend decreased by over 60%, from $2.6 billion in its original proposal, to $1 billion in its latest

- EBITDA multiples for OpCo and PropCo were reduced by half to one whole turn

Despite all of this, L&B's revised proposal is still flawed and leaves critical items unaddressed or improperly accounted for, including:

- Not providing a clear description of lease terms and mechanics between OpCo and PropCo

- Using a lodging REIT model rather than traditional net lease model without clarifying how this is possible

- Overstating rent payments and understating corporate expenses

- Not accounting for debt repayment on assumed asset sales

- Ignoring that MGM China would still be overlevered vs. direct peers even with L&B's revised $1 billion dividend

- Failing to address E&P purge and related funding requirements, and related party ownership rules

L&B Nominees Are WRONG For its Own Campaign and For MGM's Board – When L&B initially launched its campaign, it said its Board nominees would be able to "properly evaluate the strategic options for MGM's real estate and capital structure." Following Wall Street's negative reaction to L&B's proposal and MGM's highlighting of the mistakes in their analysis, L&B has backed off its plan, saying "this election is not a vote on our proposed REIT structure."

L&B's unwarranted proxy contest has switched to attacking MGM's performance and Board's oversight. However, L&B's nominees are neither corporate governance nor gaming industry experts.

Dead Hand Put – It is important to note that the dead hand put language was requested by the lenders and never the MGM Board. While L&B has attempted to take credit for raising this issue – it is public information that MGM had been pursuing an amendment to its credit agreement and as of May 4, 2015, has now done so.

- On March 2, 2015 MGM's 10K filing states: "… agreed to extend the deadlines… until April 7, 2015, to allow the Company and Bank of America to pursue amendment of the credit agreement in the second quarter of 2015…"

- On April 20, 2015 in a press release from L&B: L&B began pointing to a "dead hand put" in our credit agreements, and since described it as an "egregious entrenchment technique"

- As of Monday, May 4, 2015, the Company amended its credit facility thereby eliminating this provision

Compensation – Contrary to L&B's assertions, MGM has achieved excellent executive-shareholder alignment with its compensation program.

- The Compensation Committee is chaired by Dan Taylor, a Tracinda representative on your Board, and he and the committee have worked closely with F.W. Cook to design a program that aligns managements' interests with those of shareholders

- ISS has issued a compensation practices Quickscore rating of 2, which is the second best decile rating and indicates a "low concern level"

- A significant portion of executive compensation at MGM is tied to achievement of performance goals or the Company's stock price (79% of target compensation for the CEO is based on performance goals and stock performance)

- For 2014, the majority of our CEO's compensation (57.9%) was in the form of long-term incentives tied to stock performance

- Our Compensation Committee regularly evaluates our program in light of input from shareholders and current best practices

- L&B initially indicated its intention to vote in favor of our executive compensation program but then reversed course arbitrarily

- Concocted compensation concerns seem to be yet another attempt to shift focus from L&B's ill-informed strategic proposal

False insinuations made against Roland Hernandez and comments made by L&B nominee Richard Kincaid call into question L&B's integrity:

- On April 30, 2015, in a press release from L&B: "A board led by Lead Independent Director Roland Hernandez pressured one of our nominees, Richard Kincaid from the Vail Resorts, Inc. Board of Directors"

On May 1, 2015, in a press release from Vail Resorts: "Vail Resorts governance guidelines require that before directors accept an invitation to serve on another public board of directors, they should inform the Nominating & Governance Committee…Mr. Kincaid indicated that regardless of the views of the Vail Resorts Board of Directors, he would not withdraw from the MGM situation. Mr. Kincaid indicated that if asked, he would resign from the Vail Resorts Board of Directors, but Mr. Kincaid cautioned that if he was asked to resign, Land and Buildings would likely attempt to make Vail Resorts an "issue" in the MGM situation, which could be detrimental to Vail Resorts. After reviewing Mr. Kincaid's actions and statements, the Vail Resorts Board of Directors (excluding Mr. Hernandez) discussed the situation and asked Mr. Kincaid to resign, which he did…"

Corporate governance practice, and equally importantly privileged gaming licenses, requires Directors to be stewards of the Company, displaying honesty, integrity and candor. Based on L&B's comments and actions to date, as highlighted in this letter, we do not believe that the L&B nominees have demonstrated these qualities.

MGM HAS STRONG CORPORATE GOVERNANCE PRACTICES &

SHAREHOLDER PERSPECTIVE ON OUR BOARD TO ENSURE EFFECTIVE OVERSIGHT

Your Board is committed to best practices in corporate governance. In addition to significant shareholder representation on the Board, MGM received a favorable ISS governance and executive compensation report in 2014, and as of May 1, 2015, enjoys an ISS Governance Quickscore of 1 (the best possible). MGM's Board has also been significantly refreshed, bringing in additional perspectives, including adding four new directors in the past five years.

Our goal is to ensure that MGM meets its full potential for the benefit of all shareholders, and that is exactly what we are focused on achieving. MGM's highly-skilled, independent and diverse group of experienced Directors is deeply familiar with the Company's business, has been licensed in multiple jurisdictions, and is highly qualified to provide effective oversight and lead the Company in formulating its strategy. The Board has extensive c-suite and government experience, expertise in gaming, lodging, real estate and finance, as well as public company directorship.

Removing the targeted directors would result in MGM losing critical experience in labor and government relations, gaming and hospitality, media, international business, public utilities, energy, sustainability, and diversity programs, among other areas that are of critical importance to our business. Each of the four targeted directors makes extremely valuable contributions to our Board and we would be at a disadvantage with the departure of any one of them and the subsequent substitution by a candidate on L&B's slate. In fact, two of the L&B nominees only have public company board experience of short duration resulting from activist campaigns they were personally associated with.

JOIN THE MGM INVESTORS WHO HAVE PUBLICLY SUPPORTED MGM'S BOARD

We are very encouraged by our recent conversations with our fellow shareholders and the support they have voiced for our four highly qualified nominees. In fact, shareholders representing 25% percent of MGM's total shares outstanding have publicly supported the Company.

- Tracinda Corporation, MGM's largest shareholder, publicly supported MGM on May 1, 2015, saying, "We are very confident that the current Board and management team are committed to – and more than capable of – evaluating all avenues to deliver sustainable value […] Based on the Board's commitment, as well as the strong performance of the business since the financial crisis we intend to vote our shares for the current Board's nominees."

- Infinity World, beneficial owners of approximately 26 million shares. MGM CEO Jim Murren disclosed in a Bloomberg interview on May 4, 2015 that Infinity World supports the MGM Board nominees.

- John Paulson of Paulson & Co., beneficial owners of approximately 7 million shares, also publicly supported MGM's Board when asked about a REIT conversion on April 29, 2015, saying, "That is worth exploring […] And the Company is exploring it." Furthermore, in the same interview, Paulson is described as "…opposing [L&B's] board slate pressing MGM Resorts International to create a real estate investment trust."

YOUR VOTE IS IMPORTANT – VOTE THE WHITE PROXY CARD TODAY!

REJECT L&B'S BID FOR YOUR VOTE – DO NOT VOTE ON THE GOLD PROXY CARD

Sincerely,

The Board of Directors of MGM Resorts International

Robert Baldwin, William Bible, Mary Chris Gay, William Grounds, Alexis Herman, Roland Hernandez, Anthony Mandekic, Rose McKinney-James, James Murren, Gregory Spierkel, and Daniel Taylor

If you have any questions or require assistance voting your proxy, |

About MGM Resorts International

MGM Resorts International (NYSE: MGM) is one of the world's leading global hospitality companies, operating a portfolio of destination resort brands including Bellagio, MGM Grand, Mandalay Bay and The Mirage. The Company is in the process of developing MGM National Harbor in Maryland and MGM Springfield in Massachusetts. The Company also owns 51 percent of MGM China Holdings Limited, which owns the MGM Macau resort and casino and is developing a gaming resort in Cotai, and 50 percent of CityCenter in Las Vegas, which features ARIA Resort & Casino. For more information about MGM Resorts International, visit the Company's website at www.mgmresorts.com.

Forward-Looking Statements

Statements in this release that are not historical facts are forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995 and involve risks and/or uncertainties, including those described in the Company's public filings with the Securities and Exchange Commission. MGM has based forward-looking statements on management's current expectations and assumptions and not on historical facts. Examples of these statements include, but are not limited to, statements regarding strategic transactions MGM may pursue in the future and expected EV/EBITDA multiples. These forward-looking statements involve a number of risks and uncertainties. Among the important factors that could cause actual results to differ materially from those indicated in such forward-looking statements include effects of economic conditions and market conditions in the markets in which MGM operates and competition with other destination travel locations throughout the United States and the world, the design, timing and costs of expansion projects, risks relating to international operations, permits, licenses, financings, approvals and other contingencies in connection with growth in new or existing jurisdictions and additional risks and uncertainties described in MGM's Form 10-K, Form 10-Q and Form 8-K reports (including all amendments to those reports). In providing forward-looking statements, MGM is not undertaking any duty or obligation to update these statements publicly as a result of new information, future events or otherwise, except as required by law. If MGM updates one or more forward-looking statements, no inference should be drawn that it will make additional updates with respect to those other forward-looking statements.

Important Additional Information

MGM has filed a proxy statement on Schedule 14A and other relevant documents with the Securities and Exchange Commission ("SEC") in connection with the solicitation of proxies for its 2015 Annual Meeting of Stockholders or any adjournment or postponement thereof (the "2015 Annual Meeting") and has mailed the definitive proxy statement and a WHITE proxy card to each stockholder of record entitled to vote at the 2015 Annual Meeting. STOCKHOLDERS ARE STRONGLY ADVISED TO READ MGM's 2015 PROXY STATEMENT (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO) AND ANY OTHER DOCUMENTS FILED WITH THE SEC WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Stockholders may obtain a free copy of the 2015 proxy statement, any amendments or supplements to the proxy statement and other documents that MGM files with the SEC from the SEC's website at www.sec.gov or MGM's website at http://mgmresorts.investorroom.com/ as soon as reasonably practicable after such materials are electronically filed with, or furnished to, the SEC.

Participants in Solicitation

MGM, its directors, its executive officers and its nominees for election as director may be deemed participants in the solicitation of proxies from stockholders in connection with the matters to be considered at the 2015 Annual Meeting. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of MGM's stockholders in connection with the 2015 Annual Meeting, and their direct or indirect interests, by security holdings or otherwise, which may be different from those of MGM's stockholders generally, are set forth in MGM's definitive proxy statement for the 2015 Annual Meeting on Schedule 14A that has been filed with the SEC and the other relevant documents filed with the SEC.

Use of Non-GAAP Measures

Adjusted EBITDA and Adjusted Property EBITDA are non-GAAP financial measures. A reconciliation to the GAAP measures and other information for the three year period ended December 31, 2014 can be found on pages 39 through 41 of the "Management's Discussion and Analysis of Financial Condition and Results of Operations" section of MGM's Annual Report on Form 10-K for the fiscal year ended December 31, 2014, filed with the SEC on March 2, 2015. A reconciliation to the GAAP measures and other information for the three year period ended December 31, 2011 can be found on pages 49 through 51 of the "Management's Discussion and Analysis of Financial Condition and Results of Operations" section of MGM's Annual Report on Form 10-K for the fiscal year ended December 31, 2011, filed with the SEC on February 29, 2012.

CONTACTS:

News Media

JIM BARRON/JARED LEVY/EMILY DEISSLER/BEN SPICEHANDLER

Sard Verbinnen & Co

(212) 687-8080

Investment Community

SARAH ROGERS

MGM Resorts International

Vice President, Investor Relations

(702) 693-8654

Photo - http://photos.prnewswire.com/prnh/20150505/214054-INFO

To view the original version on PR Newswire, visit:http://www.prnewswire.com/news-releases/mgm-sends-letter-to-shareholders-300078289.html

SOURCE MGM Resorts International