The United States added 236,000 jobs in March, signaling increased economic activity for specific sectors of the economy despite FED efforts to slow down the economy and cool the labor market, thus avoiding the creation of additional pent-up demand and buying power from these added employees.

The outliers in the size of jobs added, broken down by sector and sub-industry, are focused on the wholesale trade industry. Employment in the nondurable goods sector saw the most significant employee additions within the wholesale trade industry, while durable goods came in second.

The transportation and warehousing sector reported a total of 10,400 jobs added in March, with the air transportation and truck transportation sectors seeing the benefits in bulk, adding 5,700 new jobs each.

This dynamic is extremely important for companies operating within the wholesale and retail sector, given that these job additions could signal higher demand expectations moving forward and the need for a robust logistics and transportation network to fulfill this added demand.

This environment can be one of the reasons why Costco (NASDAQ: COST) management has bumped the company's cash position by nearly USD 2.8 billion in the past quarter. In addition, some may speculate that the wholesale giant may be preparing to scoop up cheaper inventory in the coming months as logistics and supplies become more abundant.

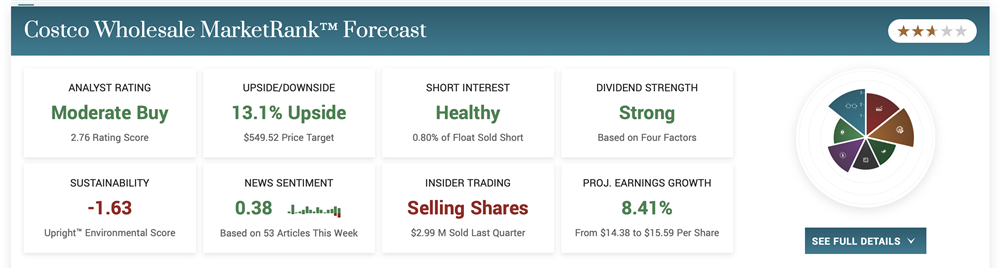

The Indicator King Said This About Costco

Retail and wholesale operations alike, for a vertical of industries, suffer from the same judgment when it comes to measurable performance indicators. The comparable sales metric is one of the widely followed figures by analysts, investors and markets in order to figure out the true direction of the underlying business in question.

A company that may be opening 10 stores a month but adding zero percent revenue month over month to each of those 10 new stores can be suffering from implied demand contraction or other issues when compared to a company that opens a fraction of the stores in a month but increased its established store revenue by 10% on a regular basis, which speaks more to market share expansion or effective marketing practices.

As reported by Costco's management, this indicator came in at 0.9% for the five-week lookback period in U.S. stores, reportedly the slowest growth in the past three years. Additionally, the entire company saw comparable sales growth of 2.6% considering international operation results, excluding the adverse effects of foreign currency and lower fuel prices, adding to the lower revenue generation from Costco members.

It is important to note where the sales did go, as this can help connect the dots with previously presented job data. Within the March sales report, management does state that E-commerce sales contracted by 11.6% as people are coming into their locations more and more.

Additionally, the bump in food sales came from their fresh food and produce segments, thus implying that people may be choosing to cook at home more rather than choosing the alternative of eating out. Within Costco's non-food segments, only the essential items such as tires, apparel, health, and beauty found a sales bottom and saw slight growth.

Gearing Up for a Down Cycle

Costco has successfully built the proverbial "moat" that Warren Buffett always refers to when explaining what makes an attractive investment prospect. This moat has allowed the company to pass down benefits to its members and shareholders more than the need to pass down costs. These achievements also reflect on a fundamental level as the company seems to showcase low cyclicality in their ROIC (return on invested capital) metrics and leverage; however, this non-cyclical character may be facing a stress test soon.

On a five-year lookback period, reflecting the normality of pre-pandemic operations versus the carnage that a quick pivot and adaptation may have left in the business figures, investors may find the key to what could come next. Management has decreased inventory levels in the past quarter by USD 1.8 billion, bringing the line item down to 24% of total assets from 27.9% just a quarter prior. Inventory represented 24% of assets in 2021 and 25.1% in 2019.

This decrease can translate to management returning to inventory levels historically adjusted for economic slowdown periods, pinned to the U.S. manufacturing PMI index as both 2021 and 2023 saw the index readings come below 50%, signaling economic contractions.

This may not necessarily mean bad news for Costco, as perhaps some of this inventory may be reduced to more discretionary items while others (like fresh food and produce or essentials like tires and health) may be receiving the bulk of the incoming inventory orders to adjust to market needs during an economic slowdown.

However, for reference to investors, when the PMI index and subsequent inventory levels behaved like this, the company still delivered ROIC in the tunes of 13-15% and sustained its dividend yield, which currently offers nearly 1%, keeping in mind that management will also be inclined to buy back a significant amount of shares when they become "cheaper" during such a slowdown.