Financial News

3 Precious Metals Miners To Buy With Raging Inflation, Geopolitical Tensions

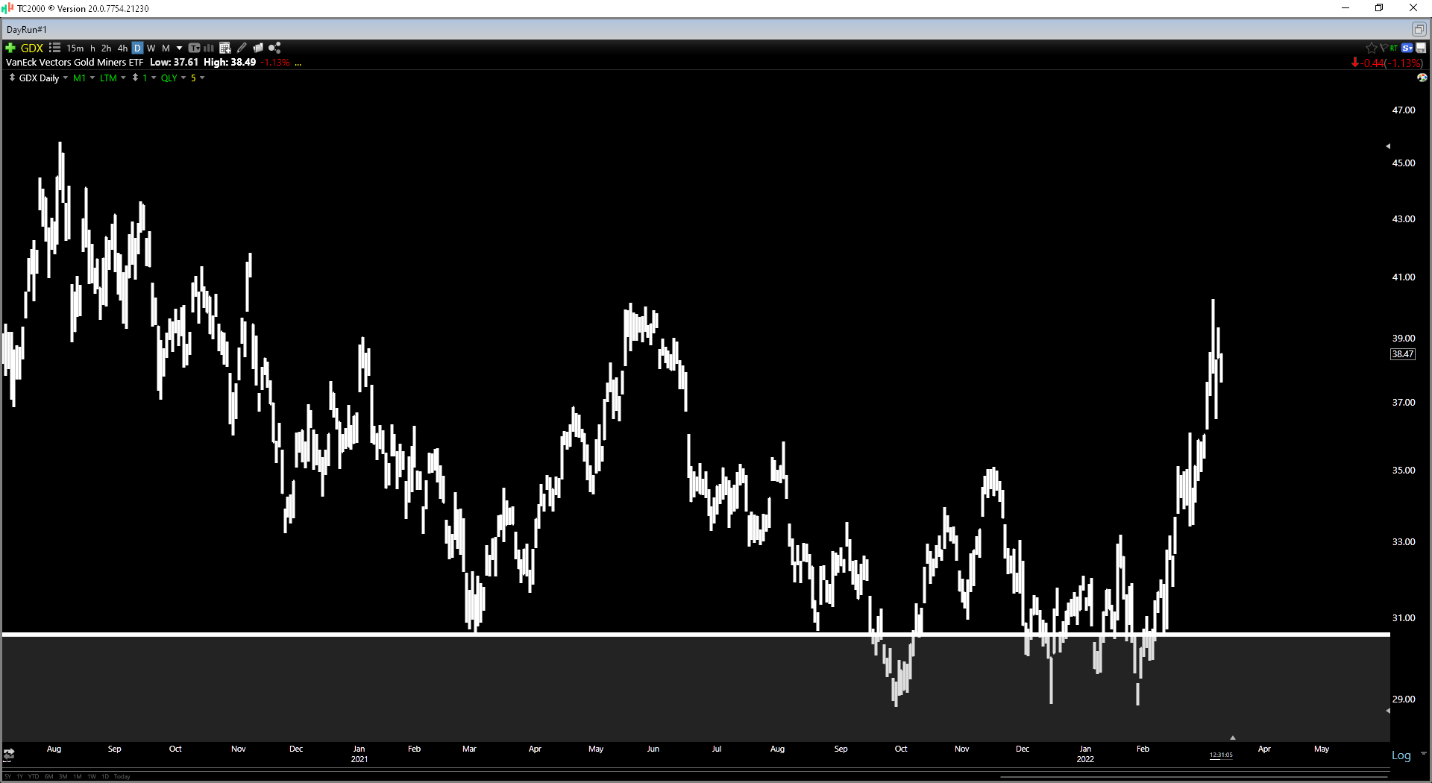

It’s been an impressive start to the year for the Gold Miners Index (GDX), with the ETF up over 15% year-to-date, trouncing the S&P-500’s performance. While this sharp rally might have many investors thinking that they’ve missed the move, this doesn’t appear to be the case, assuming history plays out similarly. This is because when GDX has only begun to outperform the S&P-500 after years of underperformance, we have typically seen multi-quarter advances. Given that this has changed to a buy-the-dip environment, we’ll look at three names that should be leaders in this bull market.

(Source: TC2000.com)

Skeena Resources (SKE), SilverCrest Metals (SILV), and Barrick Gold (GOLD) have little in common, but they do share two key traits - industry-leading reserve grades and exceptional margins or projected margins. However, they differ in the sense that one is a development stage company, one is a near-term single-asset producer, and one is a diversified producer with multiple mines. Let’s take a closer look at the three companies below, and what makes them special.

Click here to check out our Gold and Silver Industry Report for 2022

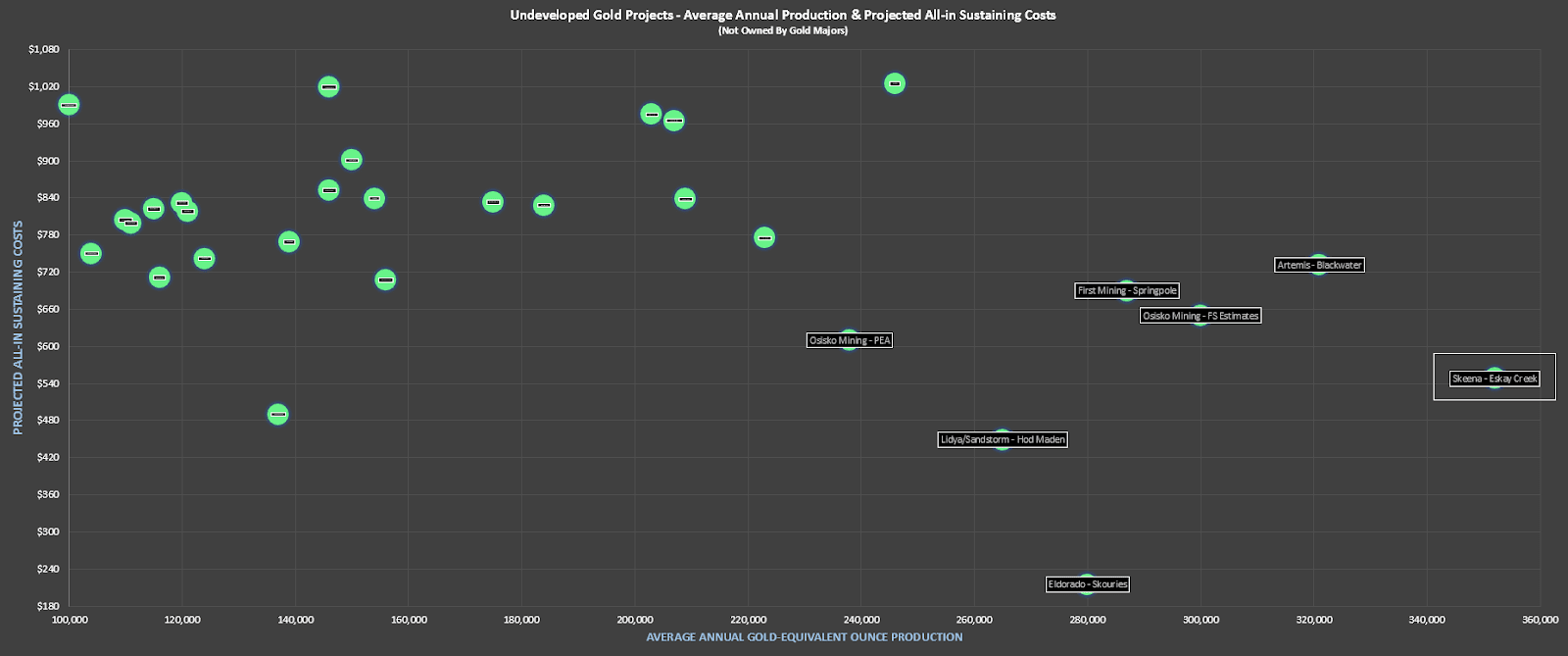

Beginning with Skeena Resources (“Skeena”), the company is busy delineating its Eskay Creek Project in British Columbia and is getting ready to release a Feasibility Study this year. While inflationary pressures are likely to contribute to an increase in upfront capex and operating costs, the project is still one of a kind, set to produce over 300,000 gold-equivalent ounces [GEOs] per annum at costs below $700/oz. This cost profile could make Skeena one of the lowest-cost producers sector-wide by 2025, with a production profile that most developers would salivate over, given that the average production profile comes in below 200,000 GEOs per annum.

As the chart below shows, Skeena lies in the most attractive quadrant among its peers from a cost/production standpoint, and this could make the stock a takeover target. This is because many producers are sitting on large cash positions and hungry to grow. Given Eskay Creek’s estimated industry-leading margins ($700/oz vs. $1,100/oz), modest initial capex ($400 million), and what should be a straightforward permitting process, it makes for an attractive bolt-on acquisition for a large producer.

(Source: Company Filings, Author’s Chart)

So, with takeover premiums ranging from 30% to 60% and Skeena’s neighbor (Pretium) being acquired for over $3.5BB in Q4 2021, Skeena is arguably a top-5 takeover target with its sub $1.0BB market cap. To summarize, if the stock were to trade back below US$10.50, I would view this as a buying opportunity.

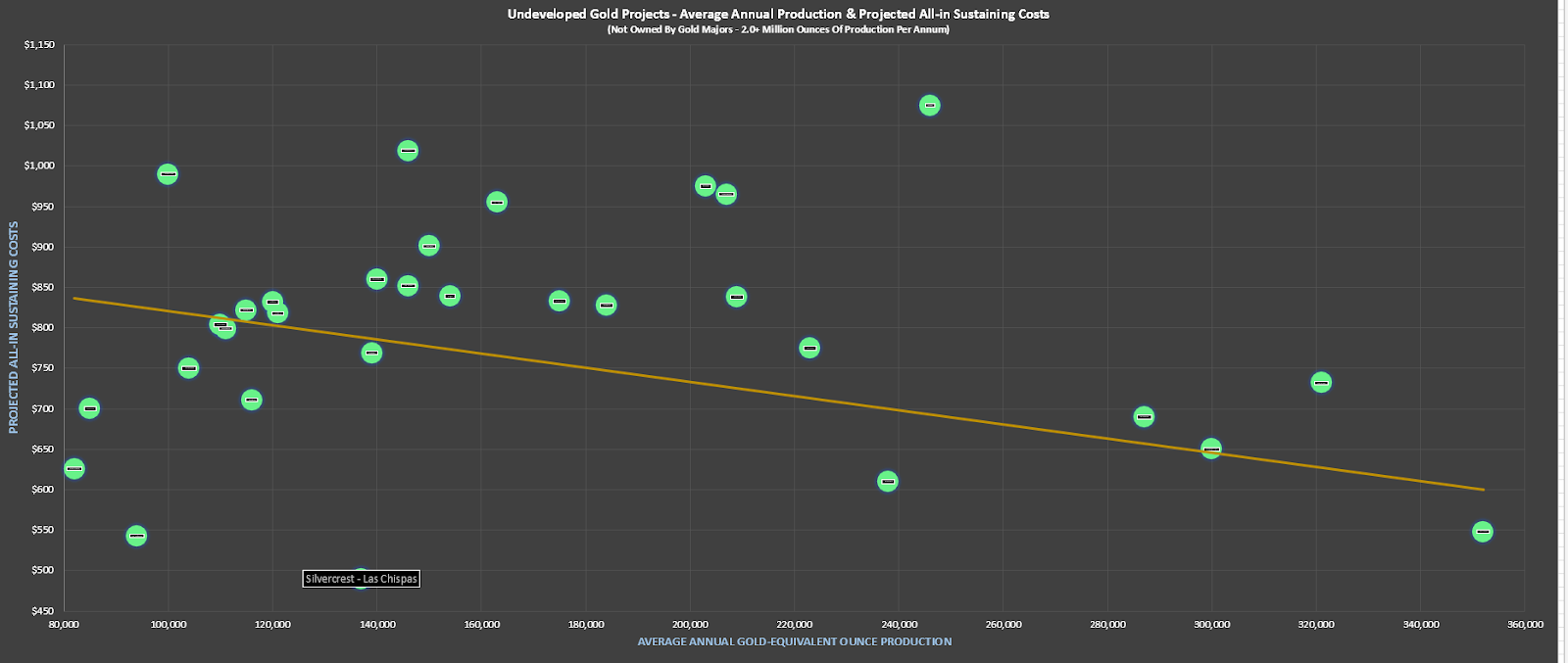

The second name on the list is SilverCrest Metals (SILV), an ultra high-grade precious metals company that’s gearing up to begin production this summer. On a gold-equivalent basis, SilverCrest will be a top-10 producer from a reserve grade standpoint, with a reserve grade of more than 9 grams per tonne gold-equivalent. These exceptional grades should translate to costs below $650/oz, giving SILV 65% plus margins at a $1,950/oz gold price.

(Source: Company Filings, Author’s Chart)

As it stands, SILV remains on budget and schedule for first production this summer despite COVID-19 headwinds, a testament to the strength of the management team. This is because many less experienced teams have seen cost overruns, delays, and significant share dilution by not buying themselves enough flexibility from a liquidity standpoint ahead of the construction period.

Given SILV’s industry-leading margins, grades, and the fact that it has significant untapped exploration potential with multiple untested veins at its Las Chiapas Project, I see the stock as a buy on any weakness. Assuming metals prices stay at these levels, SILV would trade at a more than 15% free FY2023 cash flow yield, a dirt-cheap valuation for a bonanza-grade producer.

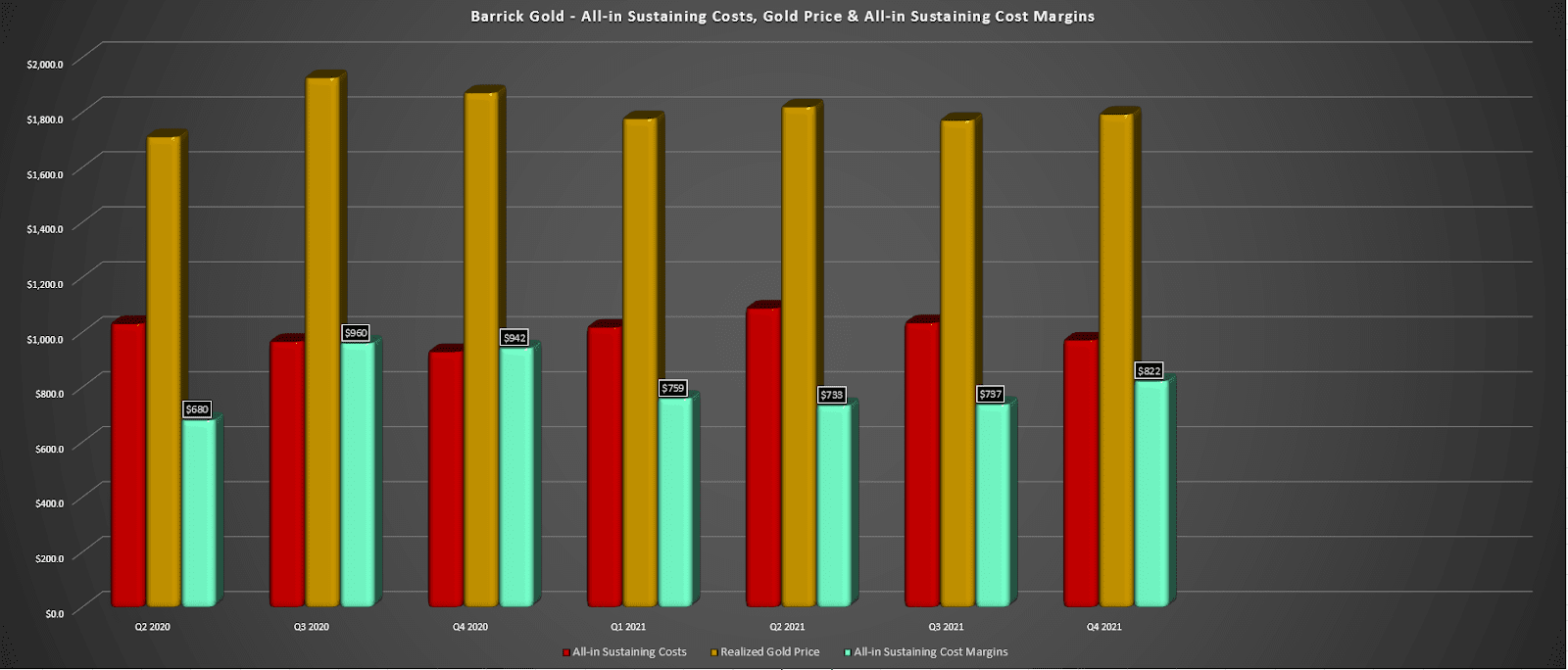

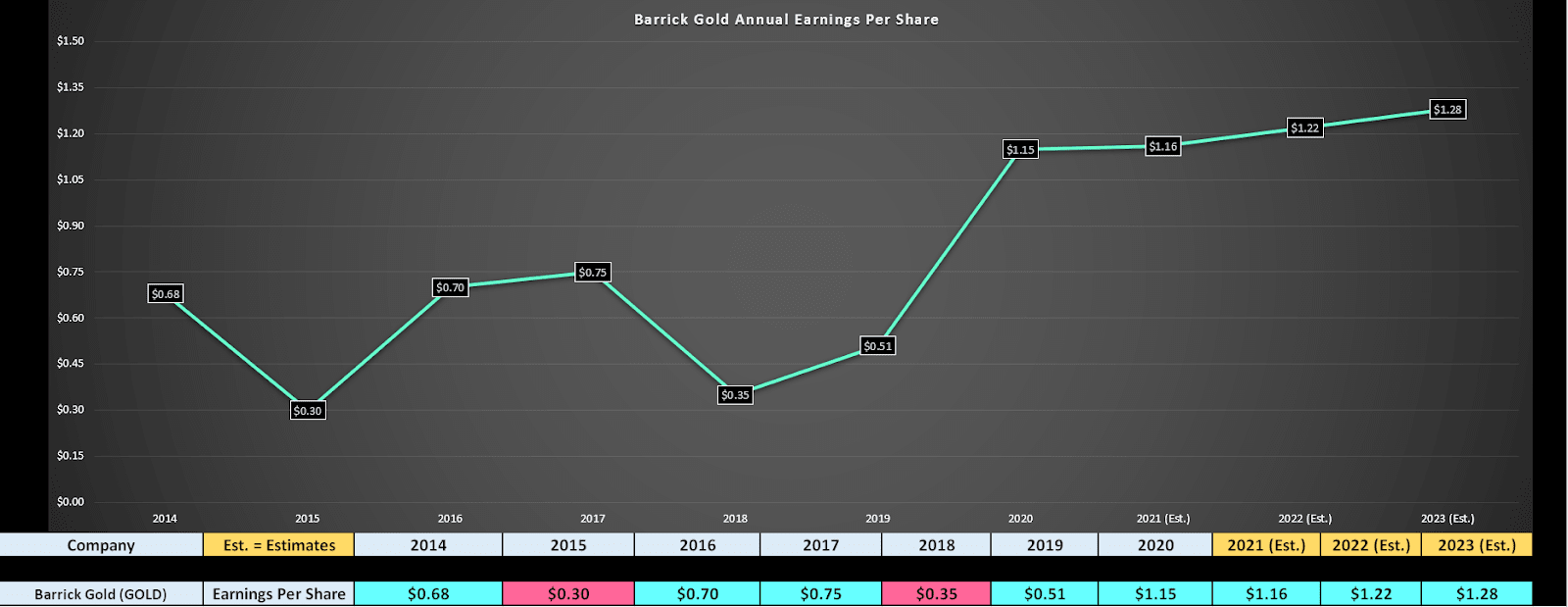

The final name on the list is Barrick, a company that needs little introduction given that it’s the 2nd largest gold producer globally. The company operates more than 10 mines across several continents, with the bulk of its production coming from the Carlin Trend in Nevada. Notably, the company also has meaningful copper exposure and saw a sharp increase in revenue last year with margins rising exponentially for its copper business.

Looking at its gold business below, we can see that margins came in at a respectable $822/oz in Q4 2021, or ~45% despite a much lower gold price ($1,800/oz). With the gold price increasing to $1,950/oz, Barrick’s margins should head north of 50%, while its copper business will remain strong, given that copper continues to find a floor at $4.25/lb. This is setting the company up for a massive year, and with a new dividend framework in place, investors could enjoy a 3% plus dividend yield, more than double that of the S&P-500.

(Source: Company Filings, Author’s Chart)

Despite this improving outlook, Barrick trades at barely 18x earnings at a current share price of $24.00, and less than 16x earnings if gold stays above $1,975/oz for most of the year. This is a very reasonable valuation for a diversified producer with copper exposure. Given the 30% rally in the stock recently, I am not a buyer at current levels. However, if GOLD were to dip below $20.00, I would view this as a low-risk buying opportunity.

(Source: YCharts.com, Author’s Chart)

With many precious metals miners to choose from and the gold price trying to break out, investors should keep a close eye on gold/silver miners, given the meaningful margin expansion. Among the group, I see SKE, SILV, and GOLD as three of the higher-quality producers, and I would expect any sharp pullbacks to provide buying opportunities.

Disclosure: I am long GLD, SKE

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.

GOLD shares were trading at $24.43 per share on Friday afternoon, down $0.06 (-0.24%). Year-to-date, GOLD has gained 29.15%, versus a -10.69% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Precious Metals Miners To Buy With Raging Inflation, Geopolitical Tensions appeared first on StockNews.com

Stock quotes supplied by Barchart

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the following

Privacy Policy and Terms and Conditions.