MSC Industrial currently trades at $86.39 per share and has shown little upside over the past six months, posting a middling return of 0.9%. The stock also fell short of the S&P 500’s 14% gain during that period.

Is now the time to buy MSC Industrial, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.We're sitting this one out for now. Here are three reasons why you should be careful with MSM and a stock we'd rather own.

Why Do We Think MSC Industrial Will Underperform?

Founded in NYC’s Little Italy, MSC Industrial Direct (NYSE:MSM) provides industrial supplies and equipment, offering vast and reliable selection for customers such as contractors

1. Long-Term Revenue Growth Disappoints

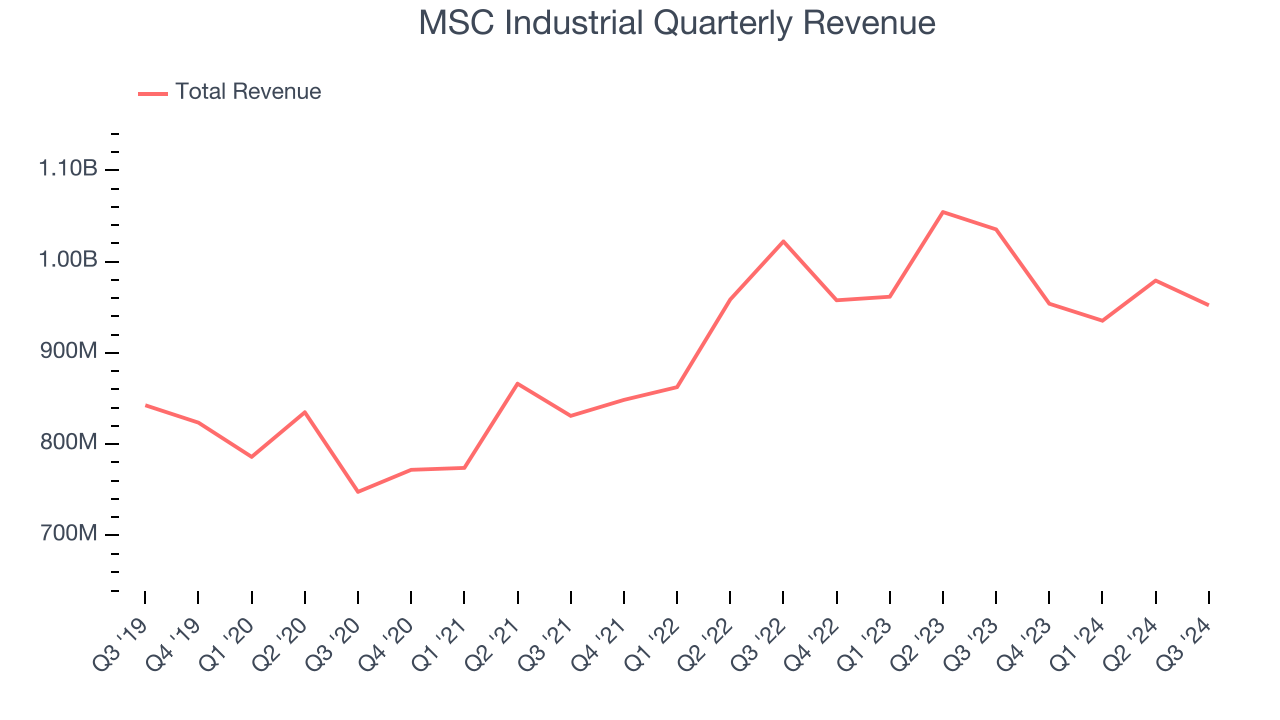

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, MSC Industrial’s 2.6% annualized revenue growth over the last five years was sluggish. This fell short of our benchmarks.

2. Core Business Falling Behind as Demand Plateaus

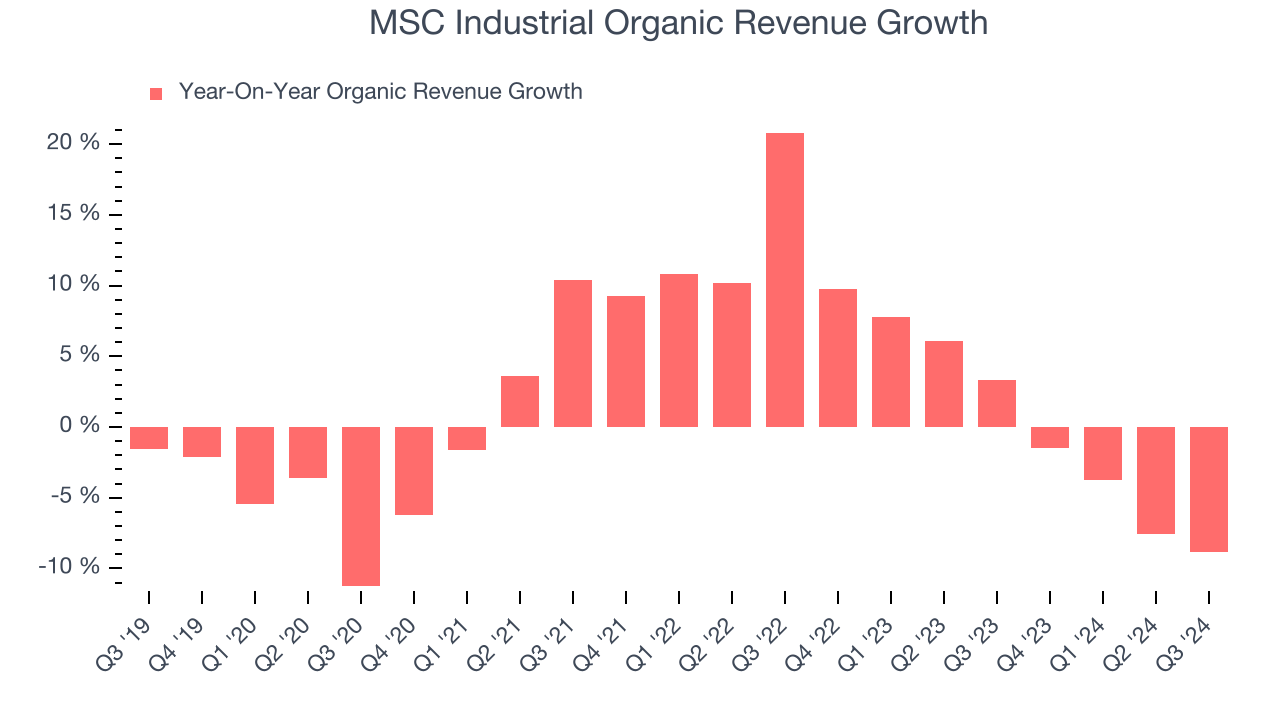

We can better understand Maintenance and Repair Distributors companies by analyzing their organic revenue. This metric gives visibility into MSC Industrial’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, MSC Industrial failed to grow its organic revenue. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests MSC Industrial might have to lean into acquisitions to accelerate growth, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

3. EPS Trending Down

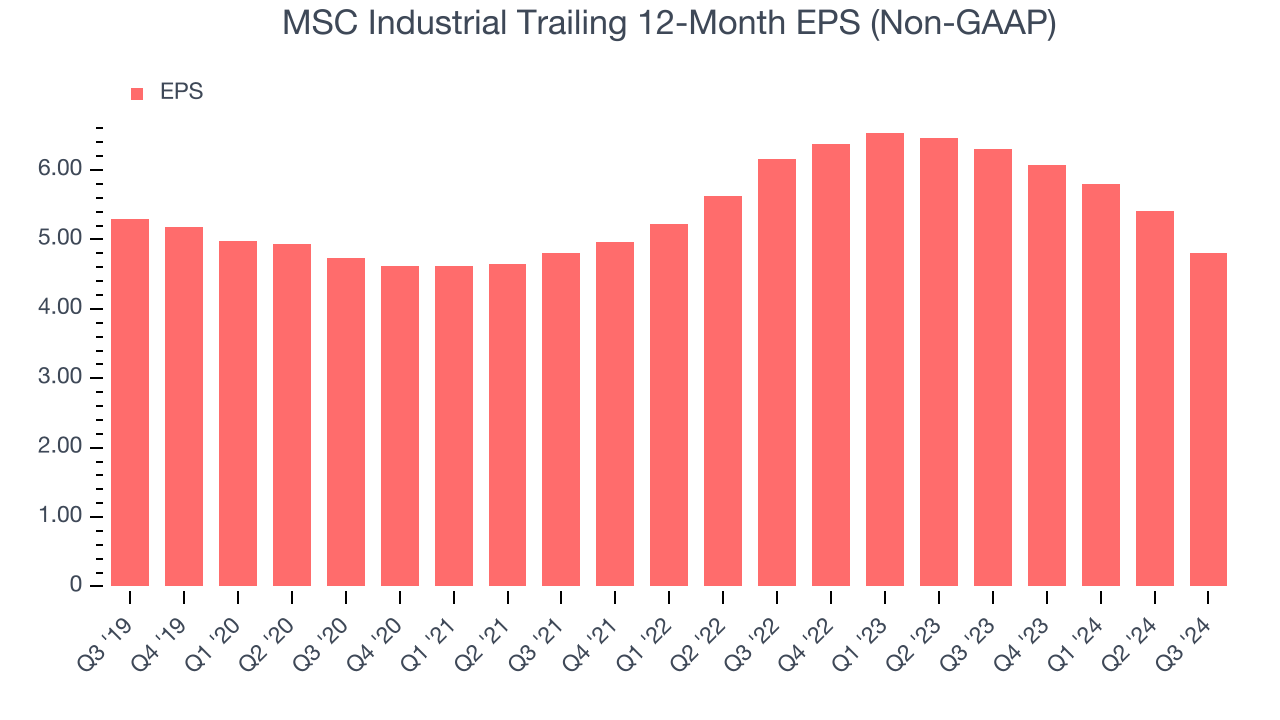

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for MSC Industrial, its EPS declined by 2% annually over the last five years while its revenue grew by 2.6%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

We see the value of companies helping their customers, but in the case of MSC Industrial, we’re out. With its shares trailing the market in recent months, the stock trades at 18x forward price-to-earnings (or $86.39 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better stocks to buy right now. We’d suggest looking at Chipotle, which surprisingly still has a long runway for growth.

Stocks We Would Buy Instead of MSC Industrial

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.