Post-Shutdown Jitters: Markets Reel as Government Reopens

By:

MarketMinute

November 13, 2025 at 14:37 PM EST

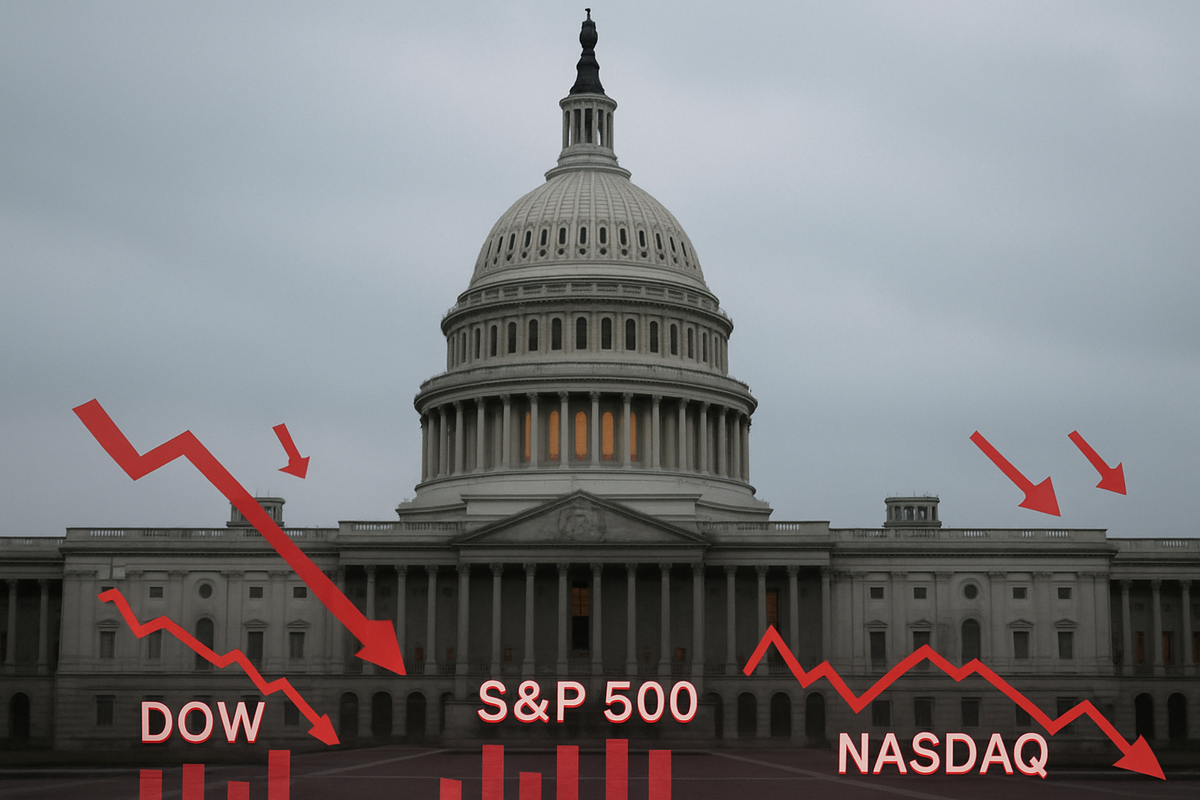

The United States government, after an unprecedented 43-day shutdown, officially reopened on Thursday, November 13, 2025, as President Donald Trump signed a funding bill into law. While the resolution brought an end to the longest federal government impasse in modern American history, the immediate reaction from financial markets was surprisingly negative, with major indices experiencing significant declines. This "sell the news" event, coupled with a looming "data deluge" and shifting expectations for Federal Reserve monetary policy, has left investors bracing for continued volatility and uncertainty. The negative market response signals that while the immediate political gridlock has been resolved, deeper anxieties about the economy's health, the impact of prolonged federal inactivity, and the future path of interest rates are weighing heavily on investor sentiment. The coming weeks are expected to be marked by "market chop" as delayed economic data finally trickles out, forcing a re-evaluation of the economic landscape and potential shifts in investment strategies. The Longest Impasse Concludes: A Timeline of Disruption and ResolutionThe recent government shutdown, which commenced on October 1, 2025, and extended for an extraordinary 43 days, concluded late Wednesday, November 12, 2025, when President Donald Trump signed a funding bill. This resolution followed swift approvals in both the House and Senate, bringing an end to a protracted standoff primarily centered on federal spending and policy disagreements. The agreement secured funding for the federal government until January 30, 2026, and crucially ensured that furloughed federal employees would receive back pay, reversing any firings that occurred during the shutdown. A key demand from Democrats regarding the extension of expiring tax credits for Affordable Care Act plans was not immediately addressed but was promised a vote by mid-December. The immediate aftermath on Thursday, November 13, 2025, saw a pronounced negative market reaction. The tech-heavy Nasdaq Composite (NASDAQ: COMP) experienced the sharpest decline, sinking 2.2%. The S&P 500 (NYSEARCA: SPY) followed, declining 1.4%, while the Dow Jones Industrial Average (NYSEARCA: DIA) fell 1.3%. This downturn wiped out much of the November advance and reflected a "sell the news" phenomenon, where the market had already priced in the optimism of a resolution. Technology shares, including prominent names like Tesla (NASDAQ: TSLA), Palantir Technologies (NYSE: PLTR), Nvidia (NASDAQ: NVDA), and Broadcom (NASDAQ: AVGO), were significant contributors to this market slide, with many seeing drops between 4% and 7.5%. The yield on the 10-year Treasury note also rose to 4.11%, indicating a decrease in bond prices, as money markets began projecting about even odds for a December rate cut by the Federal Reserve, a significant shift from earlier expectations. Corporate Crossroads: Winners and Losers in the Post-Shutdown LandscapeThe ending of the government shutdown, especially with a negative market reaction, creates a complex environment for public companies, with some poised for recovery and others facing continued headwinds. Potential "Winners" (or those likely to rebound/recover lost ground):

Potential "Losers" (or those facing continued challenges/amplified losses):

Beyond the Immediate: Wider Significance and Lingering ConcernsThe negative market reaction to the ending of the longest government shutdown in U.S. history carries significant wider implications, suggesting that the resolution is perceived as insufficient or indicative of deeper, unresolved issues. This event fits into broader trends of political instability and can have substantial ripple effects both domestically and internationally. Firstly, it signals an increased political risk premium being factored into financial markets. The expectation of recurring political dysfunction, rather than isolated incidents, means investors are increasingly wary of U.S. governmental stability. This contributes to broader global market instability and can lead to higher risk premiums in asset valuations. Secondly, the data-driven vulnerability of the modern economy has been starkly highlighted. The shutdown's "data blackout" left investors and policymakers "flying blind," and the anticipated "data deluge" post-shutdown is expected to create significant volatility as new information is integrated, potentially challenging prior assumptions about economic health and Federal Reserve policy. Ripple effects will be felt by international partners and competitors. Allies may question the reliability of the U.S. economic and political system, potentially impacting foreign direct investment and prompting other nations to seek alternative partners and reduce their reliance on the U.S. market. Competitors may seize opportunities as U.S. economic credibility temporarily wanes. Domestically, government contractors and small businesses, which bore the brunt of payment delays and operational halts, face lingering challenges, impacting their long-term growth and competitiveness. In terms of regulatory and policy implications, federal agencies will grapple with significant backlogs in processing permits, applications, and investigations, delaying business operations and critical economic functions. The persistent political gridlock, a hallmark of this shutdown, also prevents progress on strategic initiatives like healthcare reform and infrastructure modernization, impacting long-term economic competitiveness. Historically, while markets often recover from shutdowns, a negative reaction upon resolution, as seen on November 13, 2025, is less common and points to deeper concerns like unresolved economic anxieties or shifts in monetary policy expectations, rather than a simple relief rally. The Road Ahead: Navigating Uncertainty and Adapting StrategiesThe immediate aftermath of the shutdown's conclusion, marked by negative market sentiment, ushers in a period requiring careful navigation from businesses and investors. In the short term, continued market volatility is highly probable as the "data deluge" of delayed economic reports (jobs, inflation, consumer spending) is released, forcing the Federal Reserve to make critical interest rate decisions with clearer, albeit belated, information. This could lead to further shifts in rate expectations and market apprehension. Economic activity, though expected to rebound from the shutdown's immediate drag, may still face headwinds from eroded consumer and business confidence. Long-term possibilities include a potential "soft patch" in economic data and a slower recovery if underlying economic stresses persist. Recurrent political dysfunction could further erode international trust in U.S. fiscal stability and potentially lead to credit rating downgrades. There's also the risk of a "K-shaped recovery," where structurally strong sectors like technology and defense continue to grow, while others, particularly consumer discretionary and small businesses, face prolonged weakness. Strategic pivots for businesses should include diversifying revenue streams away from government dependence, building robust cash reserves for future disruptions, strengthening supply chain resilience, and proactive scenario planning. For investors, maintaining a long-term, diversified strategy is crucial, alongside considering strategic portfolio rebalancing towards more defensive sectors (healthcare, utilities) and safe-haven assets like gold. Caution with overvalued assets, especially in growth sectors, is also advised. Market opportunities may emerge from undervalued assets during the downturn, and from defensive sectors that offer stability. Conversely, challenges include heightened volatility, reduced consumer spending, persistent regulatory backlogs, and the Federal Reserve's dilemma in making policy decisions with limited initial data. Potential scenarios range from a moderate recovery, where the market gradually rebounds after initial volatility, to a protracted slowdown/stagnation if underlying economic issues are severe, or a "K-shaped" economic divergence, where certain sectors thrive while others struggle. Wrap-Up: A Test of Resilience and a Call for VigilanceThe ending of the 2025 government shutdown, after an unprecedented 43 days, provides a degree of immediate relief but has simultaneously ushered in a period of significant market uncertainty. The negative reaction on November 13, 2025, serves as a stark reminder that while political impasses can be resolved, their lingering economic and psychological effects can be profound. Key takeaways include the substantial economic disruption, estimated at billions in permanently lost GDP and wages, the critical "data blackout" that hampered decision-making, and the erosion of public and investor trust due to persistent political gridlock. The market's immediate focus has shifted from the shutdown itself to the impending "data deluge" and its implications for the Federal Reserve's monetary policy, particularly the likelihood of a December interest rate cut. Moving forward, the market is expected to remain volatile, characterized by "chop" as new economic data is digested. While a rebound in Q1 2026 is a historical pattern after Q4 weakness, the extent and speed of this recovery will depend on the clarity provided by the belated data and the Fed's response. Investors should watch for continued sector rotations, potentially away from high-valuation tech stocks towards more defensive plays. The lasting impact of this shutdown could be significant, setting a precedent for future protracted funding battles and potentially leaving economic scars that subtly influence growth for months to come. The "flying blind" scenario faced by the Federal Reserve underscores the fragility of data-dependent policymaking in times of political dysfunction. What investors should watch for in the coming months is paramount. Foremost are the delayed economic data releases, particularly the jobs report and CPI, which will offer crucial clarity. Federal Reserve communication will be vital for signals on interest rate policy. Corporate earnings and guidance for Q4 will reveal how businesses are weathering the environment. Finally, political developments regarding future budget agreements and consumer sentiment and spending will be key indicators of broader economic resilience. This event is a test of resilience for the U.S. economy and its financial markets, demanding vigilance and adaptability from all stakeholders. This content is intended for informational purposes only and is not financial advice More NewsView More

Power On: Applied Digital’s First AI Data Center Goes Live ↗

Today 16:11 EST

Alphabet: The AI Leader Best Positioned to Dominate 2026 ↗

Today 15:07 EST

2 Reasons to Load Up on Fiserv, 1 to Stay Away ↗

Today 10:41 EST

Via MarketBeat

Tickers

FISV

3 Stocks to Buy for the Evolution of AI Infrastructure ↗

Today 8:39 EST

How Semtech’s Data Center Chips Are Powering the AI Boom ↗

Today 7:25 EST

Recent QuotesView More

Stock Quote API & Stock News API supplied by www.cloudquote.io

Quotes delayed at least 20 minutes. By accessing this page, you agree to the Privacy Policy and Terms Of Service.

© 2025 FinancialContent. All rights reserved.

|