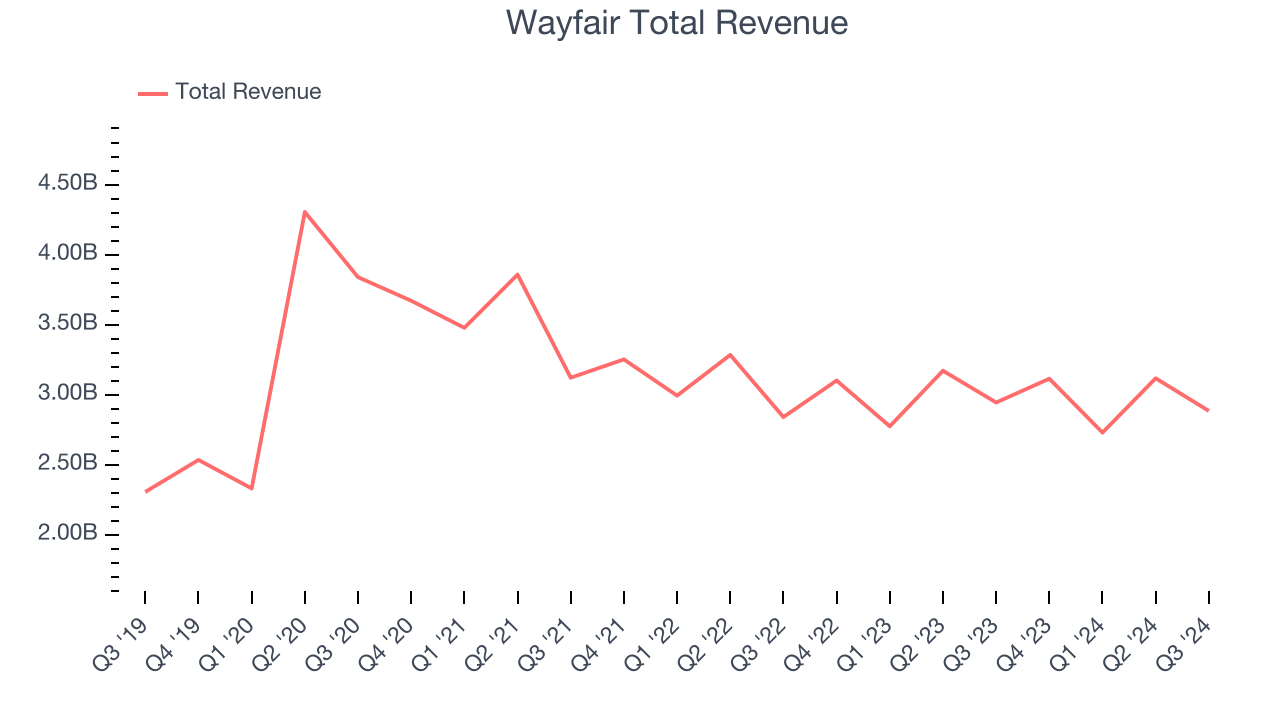

Online home goods retailer Wayfair (NYSE: W) met Wall Street’s revenue expectations in Q3 CY2024, but sales fell 2% year on year to $2.88 billion. Its non-GAAP profit of $0.22 per share was 72.5% above analysts’ consensus estimates.

Is now the time to buy Wayfair? Find out by accessing our full research report, it’s free.

Wayfair (W) Q3 CY2024 Highlights:

- Revenue: $2.88 billion vs analyst estimates of $2.88 billion (in line)

- Adjusted EPS: $0.22 vs analyst estimates of $0.13 ($0.09 beat)

- EBITDA: $119 million vs analyst estimates of $120.1 million (small miss)

- Gross Margin (GAAP): 30.3%, in line with the same quarter last year

- Operating Margin: -2.6%, up from -5.2% in the same quarter last year

- EBITDA Margin: 4.1%, in line with the same quarter last year

- Free Cash Flow was -$9 million, down from $183 million in the previous quarter

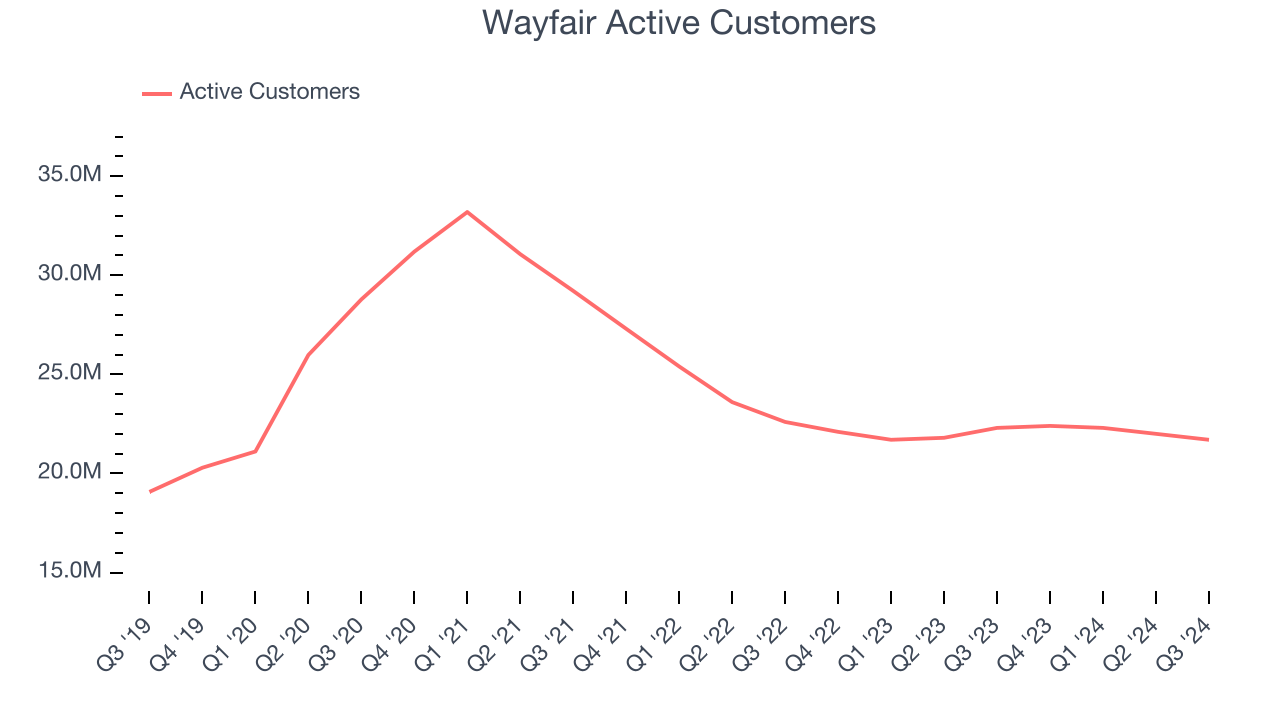

- Active Customers: 21.7 million, down 600,000 year on year

- Market Capitalization: $5.29 billion

"Q3 marked another proofpoint of resilience for Wayfair with further market share capture in the face of sustained challenges in the category. Once again, we navigated a dynamic consumer environment while driving further discipline on costs to achieve a mid-single-digit Adjusted EBITDA margin for the second quarter in a row. As I've mentioned before, our north star is driving Adjusted EBITDA dollars in excess of equity-based compensation and capital expenditures, and we're pleased to be making noteworthy improvements across each of these fronts," said Niraj Shah, CEO, co-founder and co-chairman, Wayfair.

Company Overview

Launched in 2002 by founder Niraj Shah, Wayfair (NYSE: W) is a leading online retailer for mass market home goods in the US, UK, Canada, and Germany.

Online Retail

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last three years, Wayfair’s revenue declined by 5.7% per year. This shows demand was weak, a rough starting point for our analysis.

This quarter, Wayfair reported a rather uninspiring 2% year-on-year revenue decline to $2.88 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.6% over the next 12 months, an acceleration versus the last three years. While this projection shows the market believes its newer products and services will catalyze better performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Active Customers

Buyer Growth

As an online retailer, Wayfair generates revenue growth by expanding its number of buyers and the average order size in dollars.

Wayfair struggled to engage its active customers over the last two years as they have declined by 5% annually to 21.7 million in the latest quarter. This performance isn't ideal because internet usage is secular. If Wayfair wants to accelerate growth, it must enhance the appeal of its current offerings or innovate with new products.

In Q3, Wayfair’s active customers once again decreased by 600,000, a 2.7% drop since last year. On the bright side, the quarterly print was higher than its two-year result and suggests its new initiatives are accelerating buyer growth.

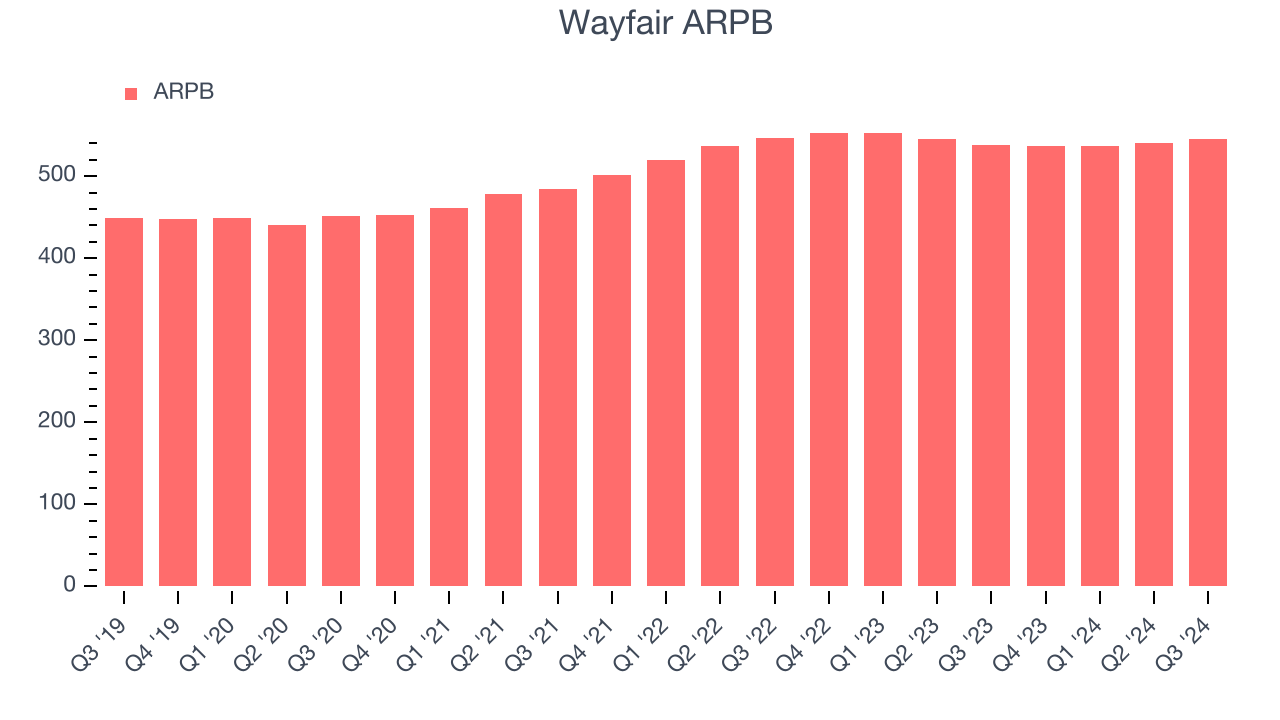

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track for consumer internet businesses like Wayfair because it measures how much customers spend per order.

Wayfair’s ARPB growth has been subpar over the last two years, averaging 1.4%. This raises questions about its platform’s health when paired with its declining active customers. If Wayfair wants to grow its buyers, it must either develop new features or lower its monetization of existing ones.

This quarter, Wayfair’s ARPB clocked in at $545. It grew 1.3% year on year, faster than its active customers.

Key Takeaways from Wayfair’s Q3 Results

Although buyers missed, revenue was in line and adjusted EPS beat. The company described driving Adjusted EBITDA dollars in excess of equity-based compensation and capital expenditures as their "north star" and there was progress on this front. Guidance will be given on the call. Judging by the move in shares, expectations were perhaps low going into the quarter. The stock traded up 10.8% to $47.47 immediately after reporting.

So should you invest in Wayfair right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.