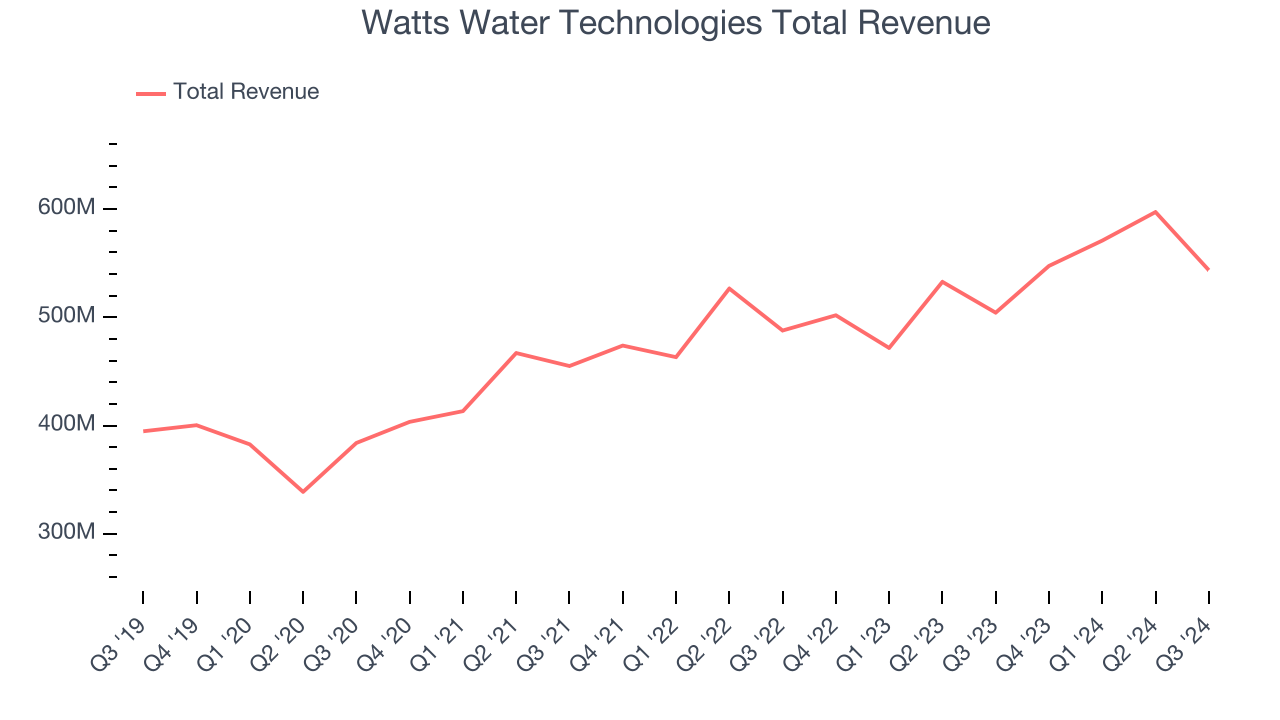

Water management manufacturer Watts Water (NYSE:WTS) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 7.8% year on year to $543.6 million. Its non-GAAP profit of $2.03 per share was 2.2% above analysts’ consensus estimates.

Is now the time to buy Watts Water Technologies? Find out by accessing our full research report, it’s free.

Watts Water Technologies (WTS) Q3 CY2024 Highlights:

- Revenue: $543.6 million vs analyst estimates of $541.5 million (in line)

- Adjusted EPS: $2.03 vs analyst estimates of $1.99 (2.2% beat)

- Gross Margin (GAAP): 47.3%, in line with the same quarter last year

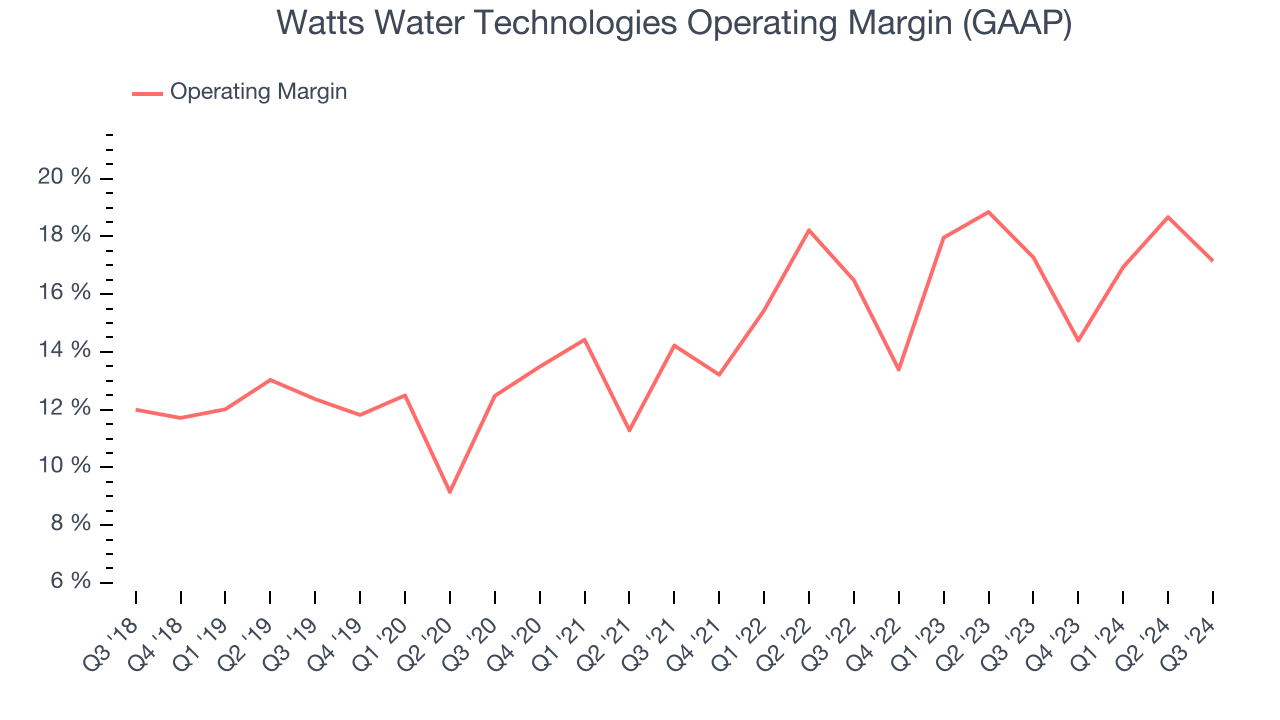

- Operating Margin: 17.1%, in line with the same quarter last year

- Free Cash Flow Margin: 15.5%, down from 18.4% in the same quarter last year

- Market Capitalization: $6.60 billion

Chief Executive Officer and President Robert J. Pagano Jr. commented, “We are pleased with our third quarter results that exceeded our expectations. I want to express my gratitude to the entire Watts team for their dedication to providing exceptional customer service. Given our strong performance through the third quarter and our fourth quarter expectations, we are increasing the midpoint of our full-year 2024 operating margin outlook.”

Company Overview

Founded in 1874, Watts Water (NYSE:WTS) specializes in manufacturing water products and systems for residential, commercial, and industrial applications globally.

Water Infrastructure

Trends towards conservation and reducing groundwater depletion are putting water infrastructure and treatment products front and center. Companies that can innovate and create solutions–especially automated or connected solutions–to address these thematic trends will create incremental demand and speed up replacement cycles. On the other hand, water infrastructure and treatment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

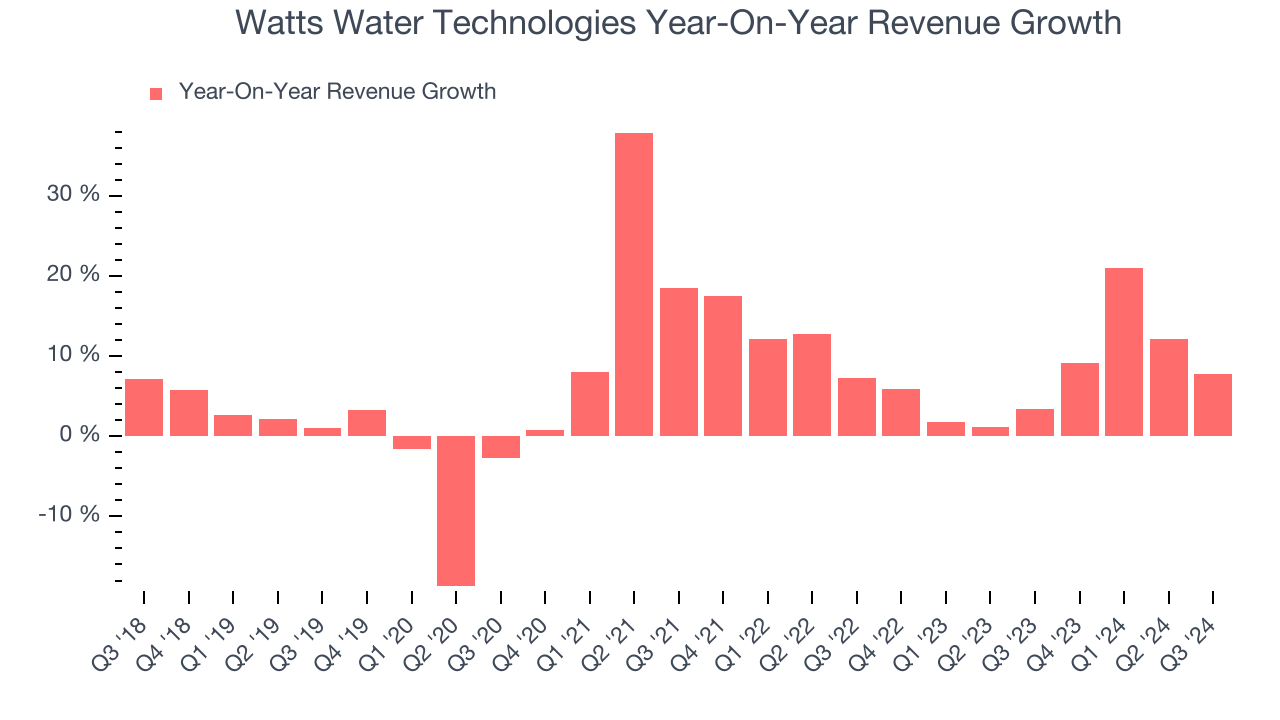

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Watts Water Technologies grew its sales at a mediocre 7.3% compounded annual growth rate. This shows it couldn’t expand in any major way, a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Watts Water Technologies’s annualized revenue growth of 7.6% over the last two years aligns with its five-year trend, suggesting its demand was stable.

This quarter, Watts Water Technologies grew its revenue by 7.8% year on year, and its $543.6 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and illustrates the market believes its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling them, and, most importantly, keeping them relevant through research and development.

Watts Water Technologies has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 15.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Watts Water Technologies’s annual operating margin rose by 5.3 percentage points over the last five years, showing its efficiency has meaningfully improved.

This quarter, Watts Water Technologies generated an operating profit margin of 17.1%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

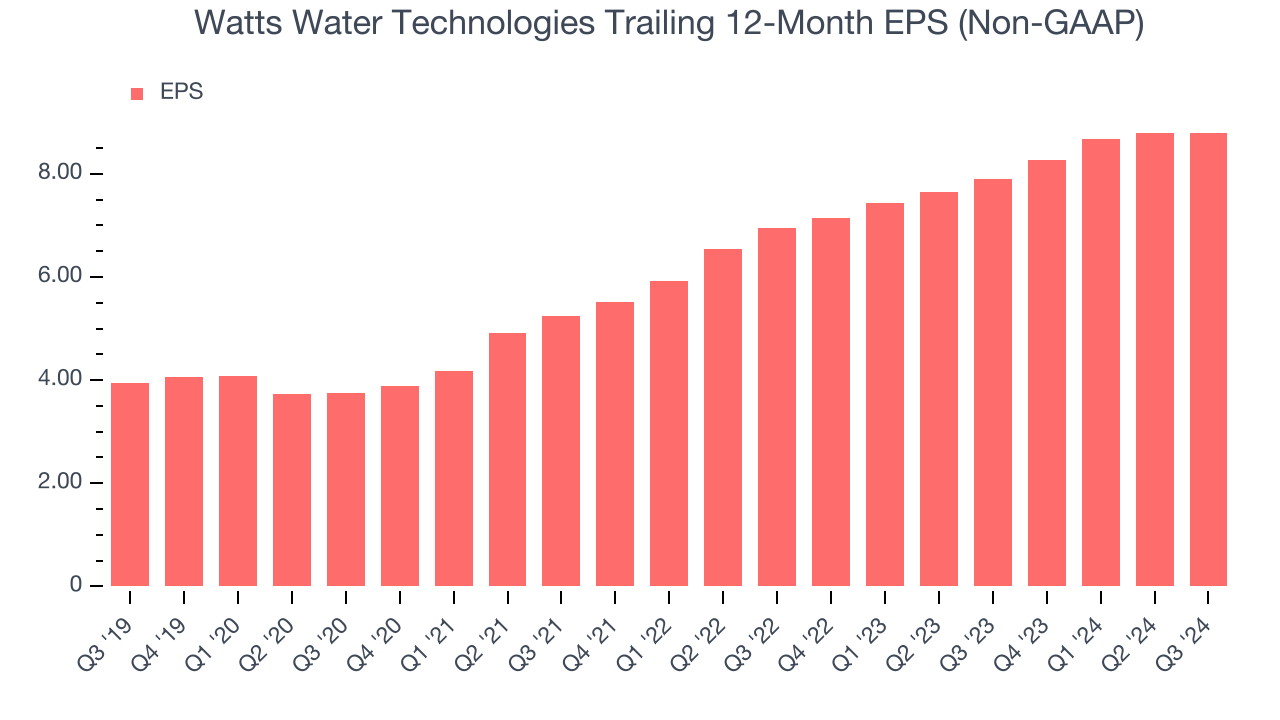

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Watts Water Technologies’s EPS grew at a spectacular 17.4% compounded annual growth rate over the last five years, higher than its 7.3% annualized revenue growth. This tells us the company became more profitable as it expanded.

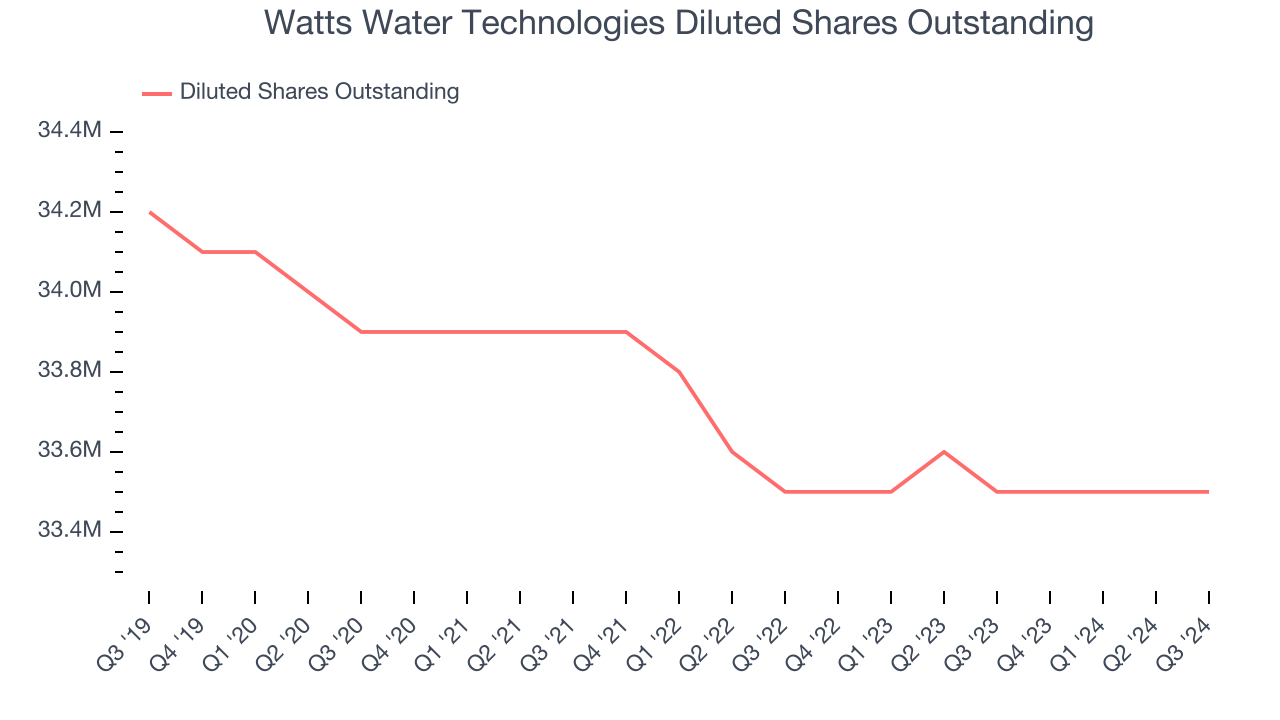

Diving into Watts Water Technologies’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Watts Water Technologies’s operating margin was flat this quarter but expanded by 5.3 percentage points over the last five years. On top of that, its share count shrank by 2%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Watts Water Technologies, its two-year annual EPS growth of 12.4% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.In Q3, Watts Water Technologies reported EPS at $2.03, down from $2.04 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2.2%. Over the next 12 months, Wall Street expects Watts Water Technologies’s full-year EPS of $8.79 to shrink by 2.9%.

Key Takeaways from Watts Water Technologies’s Q3 Results

It was good to see Watts Water Technologies beat analysts’ EPS expectations, and we think this was a decent quarter featuring some areas of strength. In other news, Chief Financial Officer Shashank Patel announced he would retire on March 15, 2025. The market didn't seem to care much as the stock traded up 1.1% to $199.65 immediately following the results.

Is Watts Water Technologies an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.