The economic data has been mixed for the last year but remains sufficient to sustain solid GDP growth, indicating growing activity, which is good news for business services companies. Business services companies provide value to other businesses with products and services that reduce time and costs, helping to sustain margins in critical industries. The critical detail for investors is that these businesses are supported by economic tailwinds in 2025, produce ample cash flow, and pay investors to own them. The tailwinds in place are driving the market action in 2024 and have them set up for double-digit gains in 2025, not counting the dividend payments.

Cintas: Helping America’s Workforce Look Good

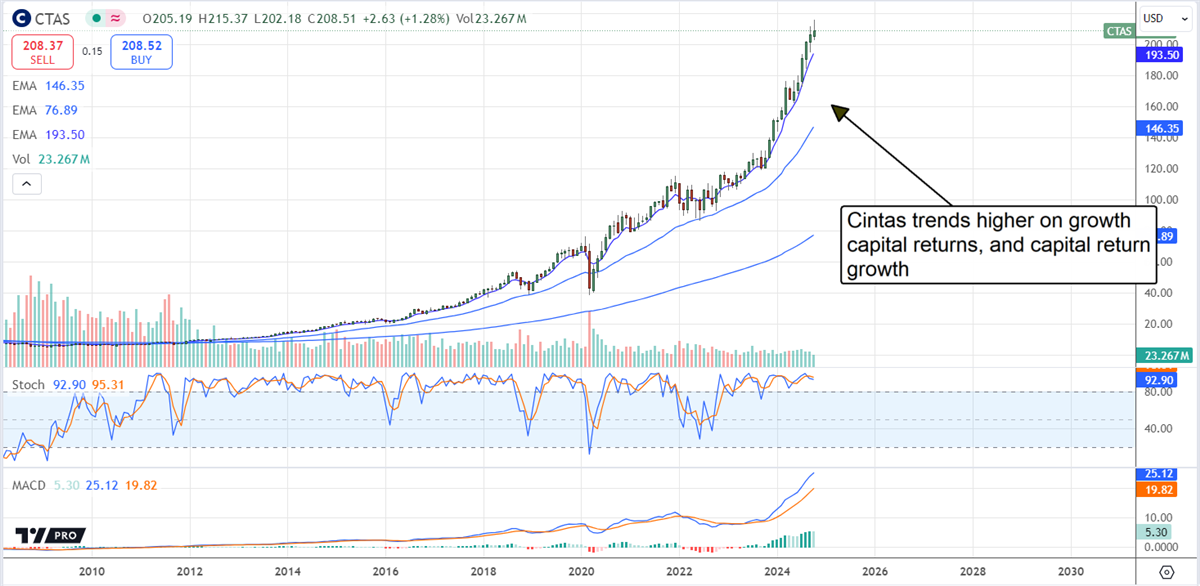

Cintas (NASDAQ: CTAS) is the leading player in uniform and facility services, providing services to various industries. The company has been growing steadily for decades due to its acquisitional and organic strategy, consolidating a fractured market while deepening penetration in existing territories. The two operational segments are Uniforms and Other, including facility services such as mats, rugs, bathroom supplies, first aid & safety, fire protection, PPE, and compliance.

Highlights from 2024 include sustained high-single-digit growth, widening margin, and outperformance that is sustained in the first fiscal quarter of 2025. The guidance for the year forecasts sequential revenue acceleration from Q1’s 6.5% pace, resulting in an 11.4% gain for the year and a slight increase in the margin at the mid-point range. Cash flow is the critical detail, allowing the company flexibility to pay an annually increasing distribution and repurchase shares.

Cintas is a Dividend Aristocrat of the highest caliber, able to sustain distribution increases indefinitely, given the growth outlook and balance sheet. The payout is worth $1.56 per share after the recent stock split, about 0.75% in yield, and is expected to grow at a solid double-digit pace in 2025. Balance sheet highlights at the end of FQ1 2025 include reduced shareholder equity, but the loss is more than offset by increased treasury shares. The repurchase program reduced the count by 1%, providing a tailwind for the market expected to blow in 2025.

The analyst's trends provide another tailwind for this market. The consensus target implies fair value near $205 but has risen by 50% in the last year, with revisions leading to new all-time highs. The high-end range is near $245, a 20% increase from the consensus target.

Fastenal Manages Inventory for Manufacturing Industries

Fastenal (NASDAQ: FAST) is a leader in fasteners ranging from common nails to OEM-specific automotive, aerospace, and industrial applications. It is also a leader in inventory management and cost control, providing many on-site, near-site, and remote services. Services include maintaining inventories of business-related supplies, including but not limited to fasteners. On-site supplies range from tiny to moderately sized and can be stored and labeled with RFID or other tracking tools or delivered in vending applications. An employee that needs a box of screws, a can of glue, or a package of rubber gloves can walk up, quickly find what they need, and receive it without trouble while inventory is closely managed, a win-win for Fastenal clients.

Fastenal's 2024 results include sustained growth and an acceleration in Q3 attributed to the diversified model. The company’s core fastener business faces headwinds due to macroeconomic conditions but is offset by the safety and maintenance segment. The outlook for 2025 is for the business to accelerate as macroeconomic headwinds, i.e., FOMC interest rate policy, ease. Analysts forecast a 7.5% increase in revenue and 8% in earnings for 2025.

Fastenal’s capital return is entirely dividends. The company pays $1.56 in 2024, worth about 2%, with shares near $77, and can sustain distribution growth if at a slower pace than recently. The payout ratio is nearly 75% but is not a significant hurdle due to the health of the balance sheet. Highlights from Q3 2024 include increased cash, inventory, and assets and decreased debt. Leverage is down, with long-term debt less than 0.5X cash, and equity is rising, up by 7.5%.

Analysts rate Fastenal as a Hold and view it as fairly valued trading near the all-time high, but revisions suggest new all-time highs will come soon. The revisions trend has increased the consensus by nearly 30% in the last year and 10% following the Q3 results, with the freshest targets 15% above the critical resistance target.