Headquartered in Toronto, Canada, Li-Cycle Holdings Corp. (LICY) is engaged in the lithium-ion battery resource recovery and lithium-ion battery recycling business in North America. The company offers a mix of cathode and anode battery materials, including lithium, nickel, cobalt, graphite, copper, aluminum, and copper and aluminum metals. It also provides lithium carbonate, cobalt sulfate, nickel sulfate, and manganese carbonate. On May 5, 2022, LICY and Glencore PLC entered a global feedstock supply agreement, under which Glencore will supply all types of manufacturing scrap and end-of-life lithium-ion batteries to LICY. The companies will also enter into agreements for the black mass supply and off-take, Hub End-Products and By-Products Off-take, and Key Reagent Supply.

The growing demand for electric vehicles, mobile phones, laptops, power tools, and others is driving the demand for lithium-ion batteries. With government policies backing the adoption of EVs and cleaner power sources, the demand for lithium-ion batteries is expected to surge in the long term. The lithium-ion battery recyclers are expected to benefit from the rising demand for lithium-ion batteries. Furthermore, strict government regulations on recycling vital materials of old batteries will help promote environmental sustainability and mitigate material scarcity. According to a Fortune Business Insights report, the lithium-ion battery recycling market is expected to grow at an 18.5% CAGR to $6.55 billion by 2028.

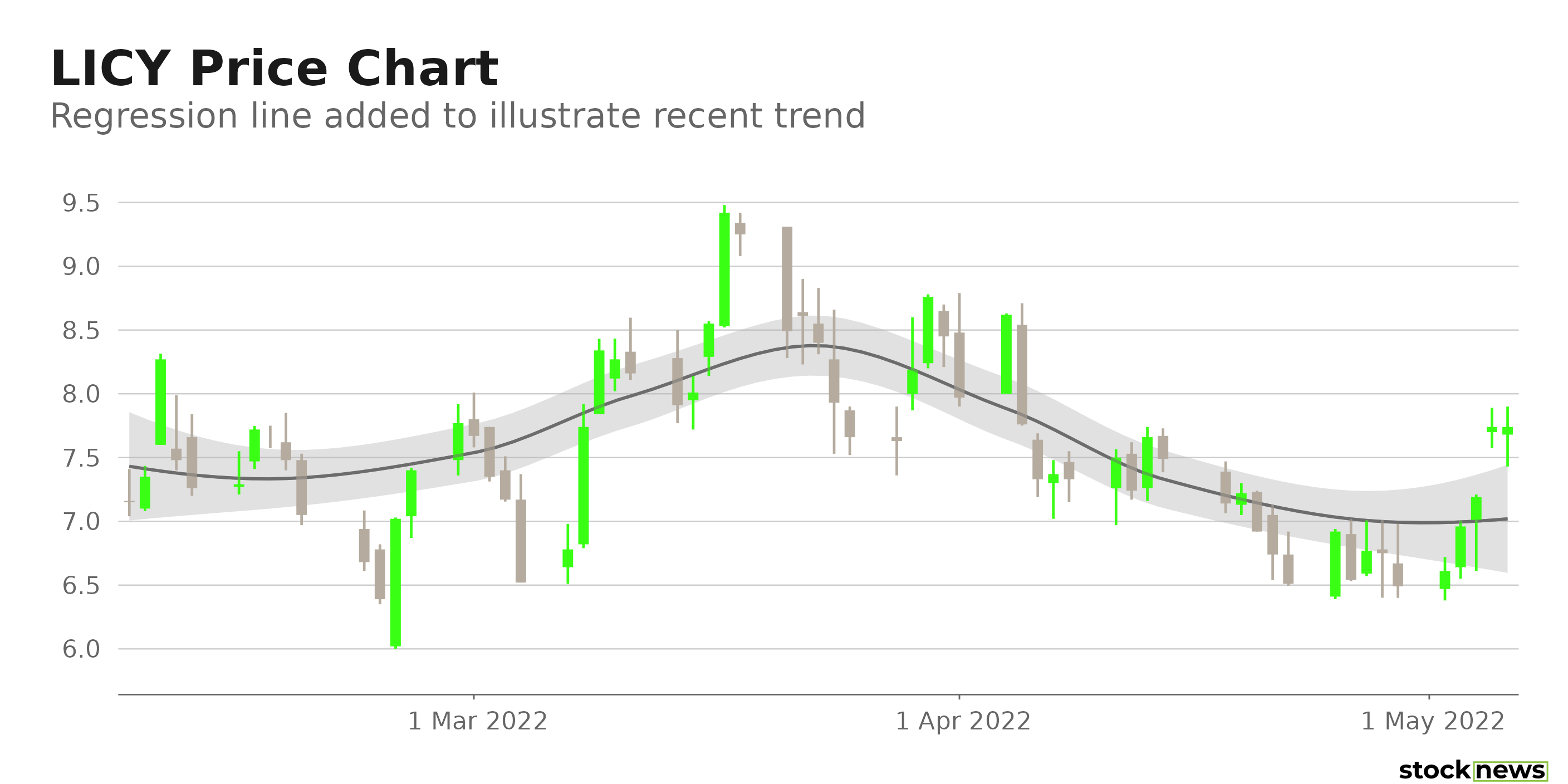

However, LICY does not look well-positioned to capitalize on the industry trends. The stock has declined 38.3% in price over the past six months and 26.3% over the past year to close the last trading session at $7.74. It is currently trading 45.8% below its 52-week high of $14.28, which it hit on November 16, 2021.

Here is what could influence LICY’s performance in the upcoming months:

Disappointing Financials

LICY’s adjusted EBITDA loss widened 359.6% year-over-year to $16.89 million for the first quarter, ended Jan. 31, 2022. The company’s current assets declined 5% to $581.22 million, compared to its current assets of $611.74 million for its fiscal year ended Oct. 31, 2021. Also, its loss from operations widened 201.9% year-over-year to $18.73 million.

Class Action Lawsuit

The Law Offices of Vincent Wong recently announced that a class action lawsuit has commenced against LICY. The allegations include misleading statements made by the company. This could tarnish LICY’s reputation and lead to penalties.

Low Profitability

LICY’s 0.03% trailing-12-month asset turnover ratio is 96.2% lower than the 0.79% industry average. Also, its trailing-12-month ROCE, ROC, and ROA are negative compared to the 14.31%, 7.08%, and 5.30% industry averages.

Stretched Valuation

In terms of forward EV/S and P/S, LICY’s 21.43x and 35.79x are higher than the 1.64x and 1.31x industry average, respectively. Also, its 96.91x trailing-12-month P/S is 6,784.2% higher than the 1.41x industry average.

POWR Ratings Reflect Bleak Prospects

LICY has an overall F rating, which equates to a Strong Sell in our POWR Ratings system. The POWR Ratings are calculated by considering 118 distinct factors, with each factor weighted to an optimal degree.

Our proprietary rating system also evaluates each stock based on eight distinct categories. LICY has a D grade for Value, which is in sync with its 76.85x trailing-12-month EV/S, which is significantly higher than the 1.84x industry average.

Furthermore, the stock has a D grade for Quality, which is in sync with its negative trailing-12-month return on total assets compared to the 5.30% industry average.

LICY is ranked last among 16 stocks in the Waste Disposal industry. Click here to access LICY’s growth, Momentum, Stability, and sentiment ratings.

Bottom Line

Given the growing use of lithium-ion batteries, battery recyclers are expected to witness solid growth in the long term. Despite the bright prospects of the battery recycling industry, LICY is unlikely to perform well due to its weak fundamentals, lower-than-industry profitability, and stretched valuation. So, we think it could be wise to avoid the stock now.

How Does Li-Cycle Holdings Corp. (LICY) Stack Up Against Its Peers?

LICY has an overall POWR Rating of F, equating to a Strong Sell rating. Therefore, one might want to consider investing in other Waste Disposal stocks with an A (Strong Buy) or B (Buy) rating, such as Heritage-Crystal Clean, Inc (HCCI), Waste Management, Inc. (WM), and Waste Connections, Inc. (WCN).

LICY shares were trading at $7.72 per share on Friday morning, down $0.02 (-0.26%). Year-to-date, LICY has declined -22.49%, versus a -13.22% rise in the benchmark S&P 500 index during the same period.

About the Author: Dipanjan Banchur

Since he was in grade school, Dipanjan was interested in the stock market. This led to him obtaining a master’s degree in Finance and Accounting. Currently, as an investment analyst and financial journalist, Dipanjan has a strong interest in reading and analyzing emerging trends in financial markets.

The post Li-Cycle Holdings: Does This Battery Recycler Deserve a Place in Your Portfolio? appeared first on StockNews.com