All eyes were locked in on the many employment reports this week. That’s because the state of jobs holds the key for the economy...as well as what is likely to happen with future Fed rate decisions.

Honestly, you could not have more divergent information especially as we compare the rip-roaring ADP report on Thursday versus the subdued Government version on Friday.

So, we have much to discuss today on the labor front as to what it tells us about future Fed actions and the stock market (SPY) outlook.

Market Commentary

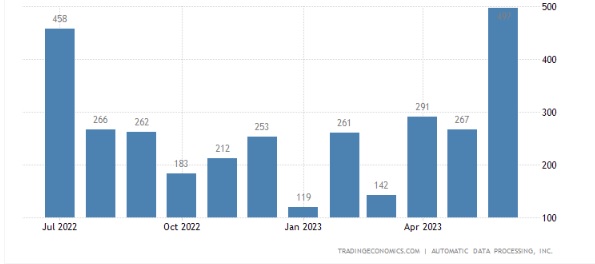

On Thursday investors could not believe their eyes as the ADP Employment Change report showed a whopping 497,000 added. That was more than 2X the expected result.

This gave investors a reason to hit the sell button as this result was considered “too good”. That’s because it sends a message to the Fed that the economy is too hot leading to more rate hikes on the way.

Another interesting part of this ADP report was seeing the +6.4% annual wage increase which is a sticky form of inflation that the Fed is not going to like the sound of. With that the odds for a rate hike on 7/26 jumped another notch to 95% showing that it is extremely likely. Further the odds for a second hike by end of the year just increased to 50% from nearly 0% chance a month ago.

Hmmm...maybe investors should start taking the Fed at their word about future rate hike intentions instead of creating conspiracy theories like they are bluffing.

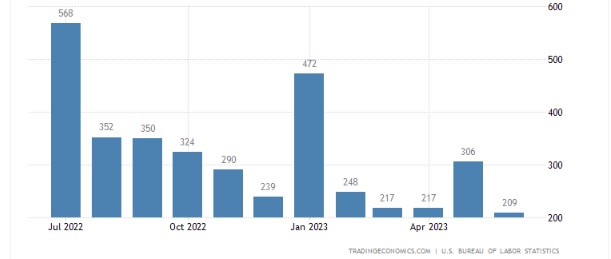

Now let’s flip the page to Friday morning where we get the tale of 2 jobs reports. That is because the Government Employment situation report was actually under expectations at just 209,000 jobs added.

There is no world in which both of these reports can be true. One is right and one is wrong about the employment trends.

Historically I have found the ADP report to be more consistently reliable about the state of employment whereas the Government version is often subject to serious revision after the fact. Yet as you explore the month by month charts for each report below, the only logical conclusion is that ADP is wrong and Government is right.

ADP Employment Change Monthly Past Year

Government Employment Situation Monthly Past Year

The trend of the Government Report is much more consistent with job adds basically slowing all year long. This makes much more logical sense in a world where the Fed keeps raising rates to slow down the economy to tamp down inflation.

The one aspect that these reports agree upon is that wage increases are still too hot which is something that Powell has repeatedly focused on at his press conferences. Again, there is NO DOUBT that another rate increase is in the cards for their meeting on 7/26.

Now let me add one more ingredient to the economy gumbo before we discuss what it all means for the market outlook and our trading plans.

That is a discussion of ISM Services which did not follow the path of ISM Manufacturing falling into deep contraction territory. In fact, it rallied from 50.3 to 53.9 in June. Even better was the New Orders component at 55.5 pointing to potentially more upside in future readings.

Add this all up, with clues from the Fed minutes, and you have an economy that is amazingly resilient. Especially on the employment side. Whereas this is normally good news...that is not the case in this situation given that the Fed’s current mission is to lower demand to win a battle versus inflation.

This recent news clearly shows that more rate hikes are on the way. And that increases the odds of future recession, but does not guarantee that outcome.

This all explains why stocks are pausing at current levels. Not a serious correction. Just not chugging ahead oblivious to the storm clouds off in the distance.

What many bulls are counting on is that a recession may never truly come together because of all the folks who chosen early retirement during Covid. This is why the labor market is so strong because there are literally 2-3 million less people looking for jobs leading to historically low unemployment rate and creating ample pressure on employers to give raises.

This is an interesting juxtaposition versus the Fed who wants to stamp out inflation with wage increases being one of the stickier elements. This is why so many market commentators, like Steve Liesman at CNBC, is talking about the Fed on purpose hiking rates “until something breaks”.

Clearly the key thing that needs to break is employment to produce less income in the economy which begets lower spending. This action would tame the most persistent form of inflation in wages.

So who is going to win this battle: Market Bulls vs. the Fed?

For me the fundamental logic still points to future recession (like in the next 12 months) with return of the bear market. BUT it is not a forgone conclusion. Nor should we discount the clearly bullish price action.

The solution is to take on a balanced investment approach closer to 50% long the stock market. Then adjust more bullish or bearish as new facts roll in.

Very few facts will matter this month outside of the 7/26 Fed meeting followed by the early August set of reports like ISM Manufacturing, ISM Services and Government Employment. Even the 7/12 CPI and 7/13 PPI inflation reports will barely move the needle as it is already assumed that inflation is too high forcing the Fed to raise rates once again.

The best assumption is that the market will consolidate around recent highs with a chance of modest pullback creating a new trading range. This pause will end as investors digest the next round of information that helps better determine the odds of future recession...and thus direction of the market.

I will do my best to share timely insights on that information as it comes in along with appropriate changes to our trading strategy. Again, I do lean bearish given the facts in hand...but more than happy to get bullish if that is what logic dictates.

What To Do Next?

Discover my full market outlook and trading plan for the rest of 2023. It’s all available in my latest presentation:

2nd Half of 2023 Stock Market Outlook >

Just in case you are curious, let me pull back the curtain a little wider on the main contents:

- Review of...How Did We Get Here?

- Bear Case

- Bull Case

- And the Winner Is??? (Spoiler: Bear case more likely)

- Trading Plan with Specific Trades Like...

- Top 10 Small Cap Stocks

- 4 Inverse ETFs

- And Much More!

If these ideas appeal to you, then please click below to access this vital presentation now:

2nd Half of 2023 Stock Market Outlook >

Wishing you a world of investment success!

Steve Reitmeister…but everyone calls me Reity (pronounced “Righty”)

CEO, StockNews.com and Editor, Reitmeister Total Return

SPY shares rose $0.24 (+0.05%) in after-hours trading Friday. Year-to-date, SPY has gained 15.54%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Steve Reitmeister

Steve is better known to the StockNews audience as “Reity”. Not only is he the CEO of the firm, but he also shares his 40 years of investment experience in the Reitmeister Total Return portfolio. Learn more about Reity’s background, along with links to his most recent articles and stock picks.

The post Jobs Market vs. Stock Market? appeared first on StockNews.com