Last week will be remembered as the week AI proved it was more than just a blip in the radar for the market. NVIDIA’s (NASDAQ: NVDA) earnings and guidance cemented that the demand for AI is real, the adoption of the new technology is real, and it’s only just beginning.

Last week will be remembered as the week AI proved it was more than just a blip in the radar for the market. NVIDIA’s (NASDAQ: NVDA) earnings and guidance cemented that the demand for AI is real, the adoption of the new technology is real, and it’s only just beginning.

While most of the attention and applause was on NVDA’s blowout earnings and guidance, many other semiconductor heavyweights experienced an enormous inflow of volume and share price appreciation.

Taiwan Semiconductor Manufacturing Company Limited (NYSE: TSM) was one of the largest beneficiaries of NVDA’s earnings. In the two days that followed the earnings report, shares of TSM rallied over 14% and ended the week up 11.48%. The company gained about 66 billion in market capitalization in the two days following the report.

TSMC is well situated to benefit from the AI Boom

TSMC was founded as and remains to this day the world’s leading pure-play semiconductor foundry. TSMC manufactures semiconductors for other companies at their own specification. Some of TSMC’s clients include Advanced Micro Devices (NASDAQ: AMD), Apple (NASDAQ: AAPL), and NVIDIA. Even the third largest chip manufacturer in the world, Intel (NASDAQ: INTC) outsources some of its manufacturing to TSMC.

This unique business model ensures that TSMC will remain relevant to the industry while never competing with its customers.

As of 2022, TSMC had seven operational foundries throughout Taiwan. The company plans to open an additional plant in Arizona in 2024 and another Japan.

TSM First Quarter Earnings and Outlook

For the first quarter, TSMC reported revenues of $16.72 billion, a (4.8%) change YoY. EPS decreased to $1.31 compared to $1.40 for the same period. Analysts forecast a further dip in EPS of $1.08 for the second quarter. However, analysts estimate EPS of $1.48 and $1.61 for the third and fourth quarters.

This has been a steady cyclical trend with the company, as Q1 and Q2 are slower periods, with the second half of the year being its strongest. While the company faced some macroeconomic and geopolitical headwinds, it still managed to post impressive margins. For the first quarter, TSMC posted a net income margin of 40.7%.

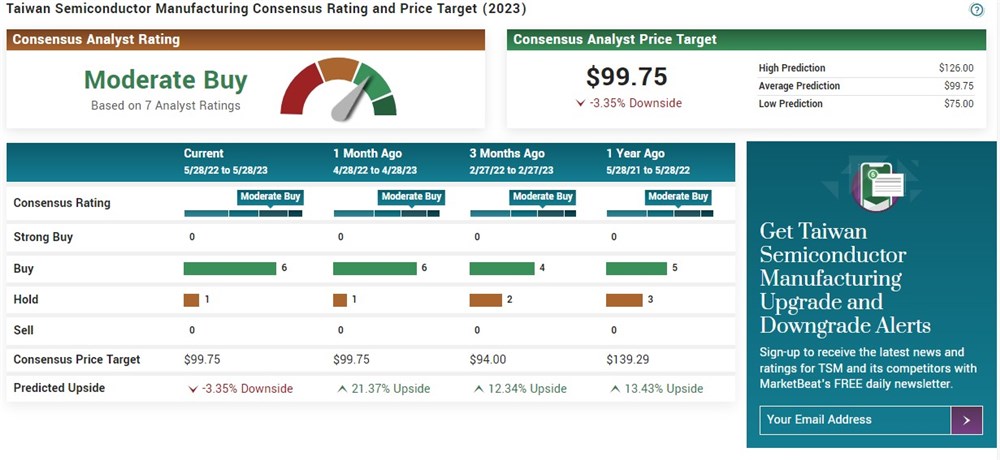

The current consensus analyst price target is $99.75, implying a 3.35% downside for the stock. TSMC currently has a consensus rating of Moderate Buy, with six of the seven analysts having a Buy rating.

The current consensus analyst price target is $99.75, implying a 3.35% downside for the stock. TSMC currently has a consensus rating of Moderate Buy, with six of the seven analysts having a Buy rating.

Tensions Between China and Taiwan

TSMC investors have been increasingly hesitant over the growing tensions between Taiwan and China. It was recently reported that Buffett’s Berkshire sold its shares in TSMC. This came after Buffett cited concerns about the geopolitical tensions when discussing the company at Berkshire’s annual meeting.

Several geopolitical scenarios and risks face the company’s business, which could directly impact its ability to deliver a return to shareholders. As trade tensions and deteriorating relations between the U.S. and China persist, there is a possibility that TSMC’s operations and supply chains could be impacted, affecting their growth prospects.

Should You Invest in TSMC

TSMC plays a crucial role in the global chip industry. With its advanced manufacturing capabilities and partnerships with major technology companies, TSMC is well-positioned to capitalize on the growing demand for chips driven by the expanding applications of artificial intelligence. That alone makes it a solid contender in the market.

TSMC’s unique and favorable business model makes it an appealing portfolio addition. However, investors must be mindful of the potential risks of geopolitical tensions.