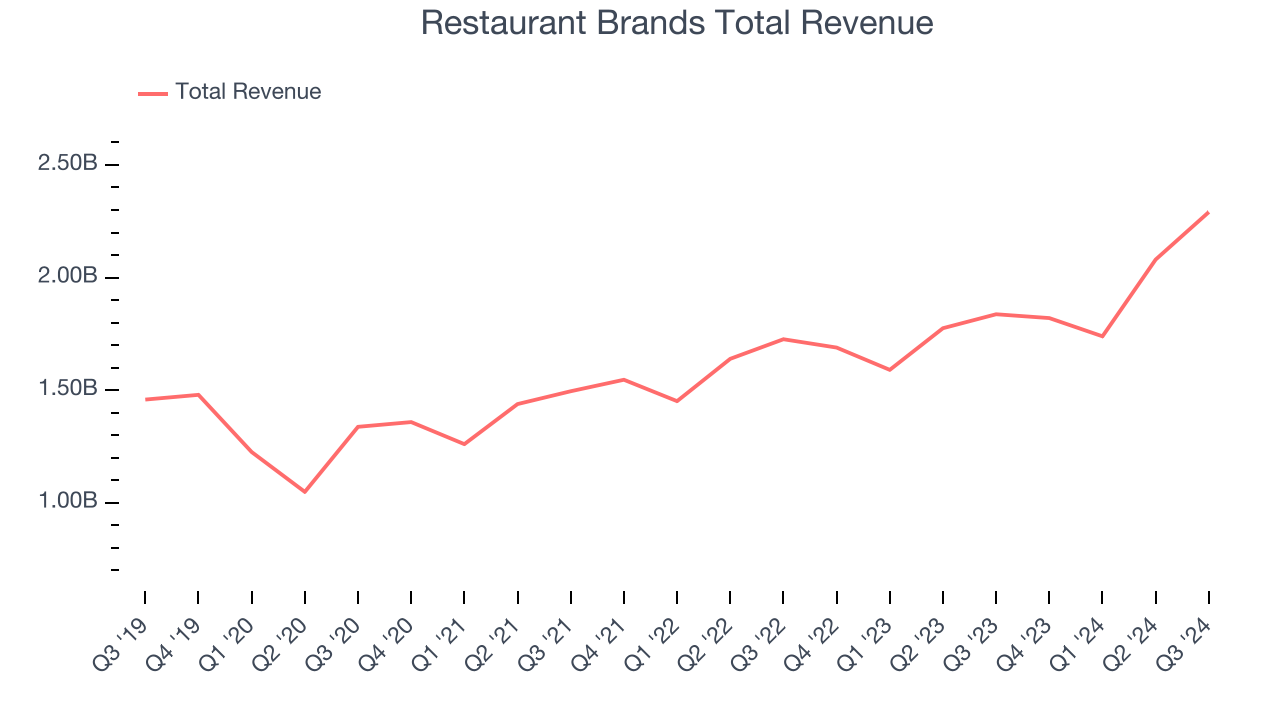

Fast-food company Restaurant Brands International (NYSE:QSR) fell short of the market’s revenue expectations in Q3 CY2024, but sales rose 24.7% year on year to $2.29 billion. Its non-GAAP profit of $0.93 per share was also 2.4% below analysts’ consensus estimates.

Is now the time to buy Restaurant Brands? Find out by accessing our full research report, it’s free.

Restaurant Brands (QSR) Q3 CY2024 Highlights:

- Revenue: $2.29 billion vs analyst estimates of $2.35 billion (2.7% miss)

- Adjusted EPS: $0.93 vs analyst expectations of $0.95 (2.4% miss)

- EBITDA: $748 million vs analyst estimates of $755.6 million (small miss)

- Gross Margin (GAAP): 34.8%, down from 41.5% in the same quarter last year

- Operating Margin: 25.2%, down from 32.7% in the same quarter last year

- EBITDA Margin: 32.6%, down from 38% in the same quarter last year

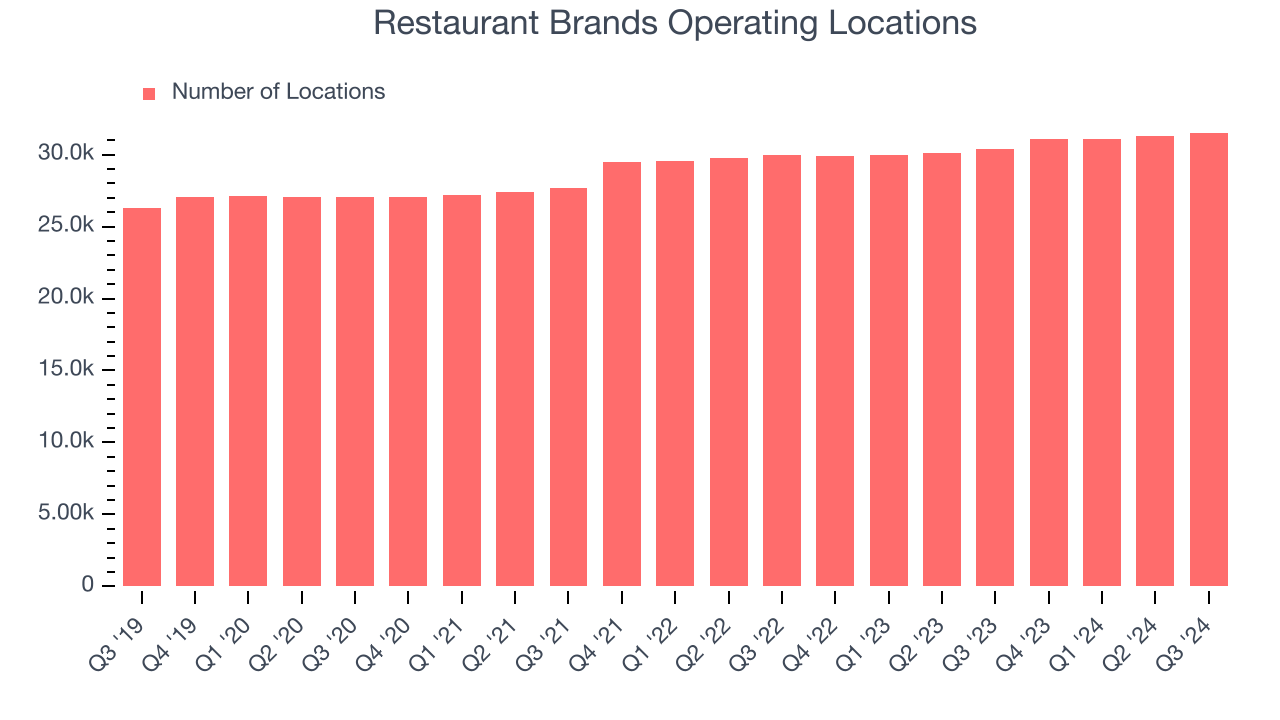

- Locations: 31,525 at quarter end, up from 30,375 in the same quarter last year

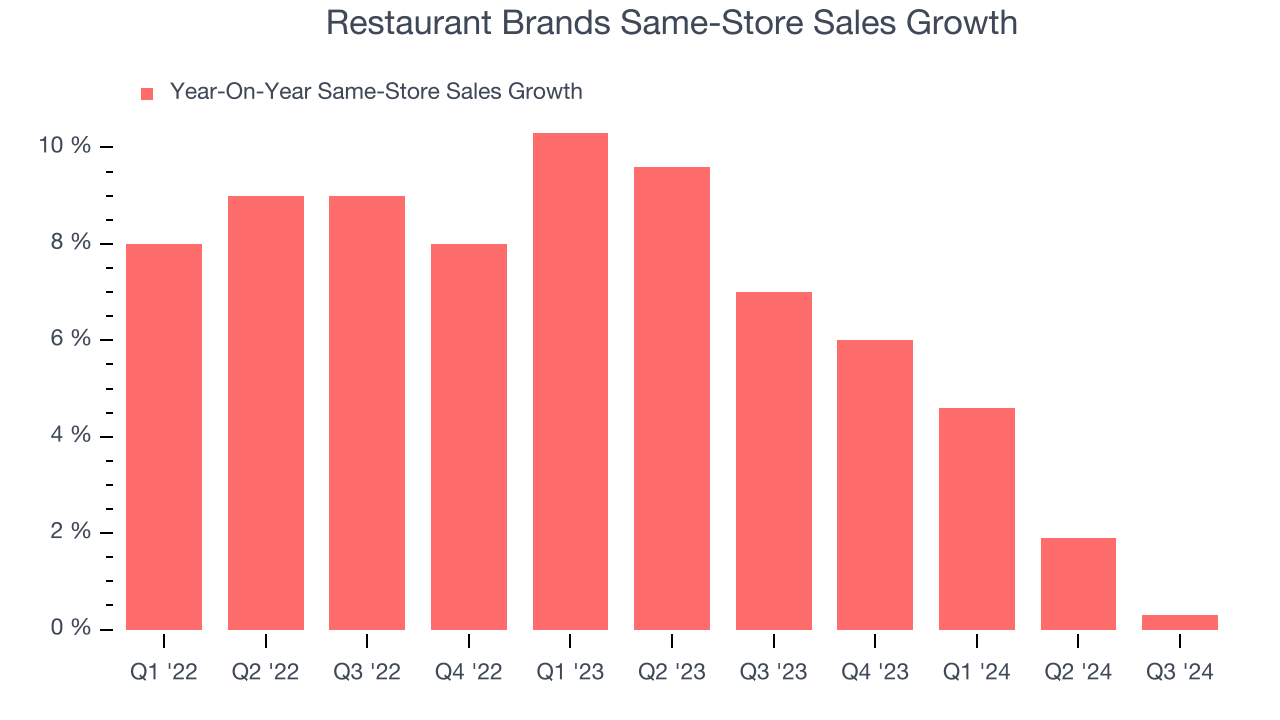

- Same-Store Sales were flat year on year (7% in the same quarter last year)

- Market Capitalization: $22.67 billion

Company Overview

Formed through a strategic merger, Restaurant Brands International (NYSE:QSR) is a multinational corporation that owns three iconic fast-food chains: Burger King, Tim Hortons, and Popeyes.

Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years.

Restaurant Brands is larger than most restaurant chains and benefits from economies of scale, enabling it to gain more leverage on fixed costs than its smaller competitors.

As you can see below, Restaurant Brands grew its sales at a decent 7.6% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, Restaurant Brands generated an excellent 24.7% year-on-year revenue growth rate, but its $2.29 billion of revenue fell short of Wall Street’s high expectations.

Looking ahead, sell-side analysts expect revenue to grow 17.8% over the next 12 months, an acceleration versus the last five years. This projection is healthy and indicates the market believes its newer offerings will spur faster growth.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Restaurant Performance

Number of Restaurants

Restaurant Brands sported 31,525 locations in the latest quarter. Over the last two years, it has opened new restaurants quickly, averaging 2.6% annual growth. This was faster than the broader restaurant sector. Additionally, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while Restaurant Brands provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where the concept has few or no locations.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth for restaurants open for at least a year.

Restaurant Brands has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 6%. This performance suggests its rollout of new restaurants is beneficial for shareholders. We like this backdrop because it gives Restaurant Brands multiple ways to win: revenue growth can come from new restaurants or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Restaurant Brands’s year on year same-store sales were flat. By the company’s standards, this growth was a meaningful deceleration from the 7% year-on-year increase it posted 12 months ago. We’ll be watching Restaurant Brands closely to see if it can reaccelerate growth.

Key Takeaways from Restaurant Brands’s Q3 Results

We struggled to find many strong positives in these results. Its revenue missed analysts’ expectations and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.7% to $66.76 immediately following the results.

Restaurant Brands may have had a tough quarter, but does that actually create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.