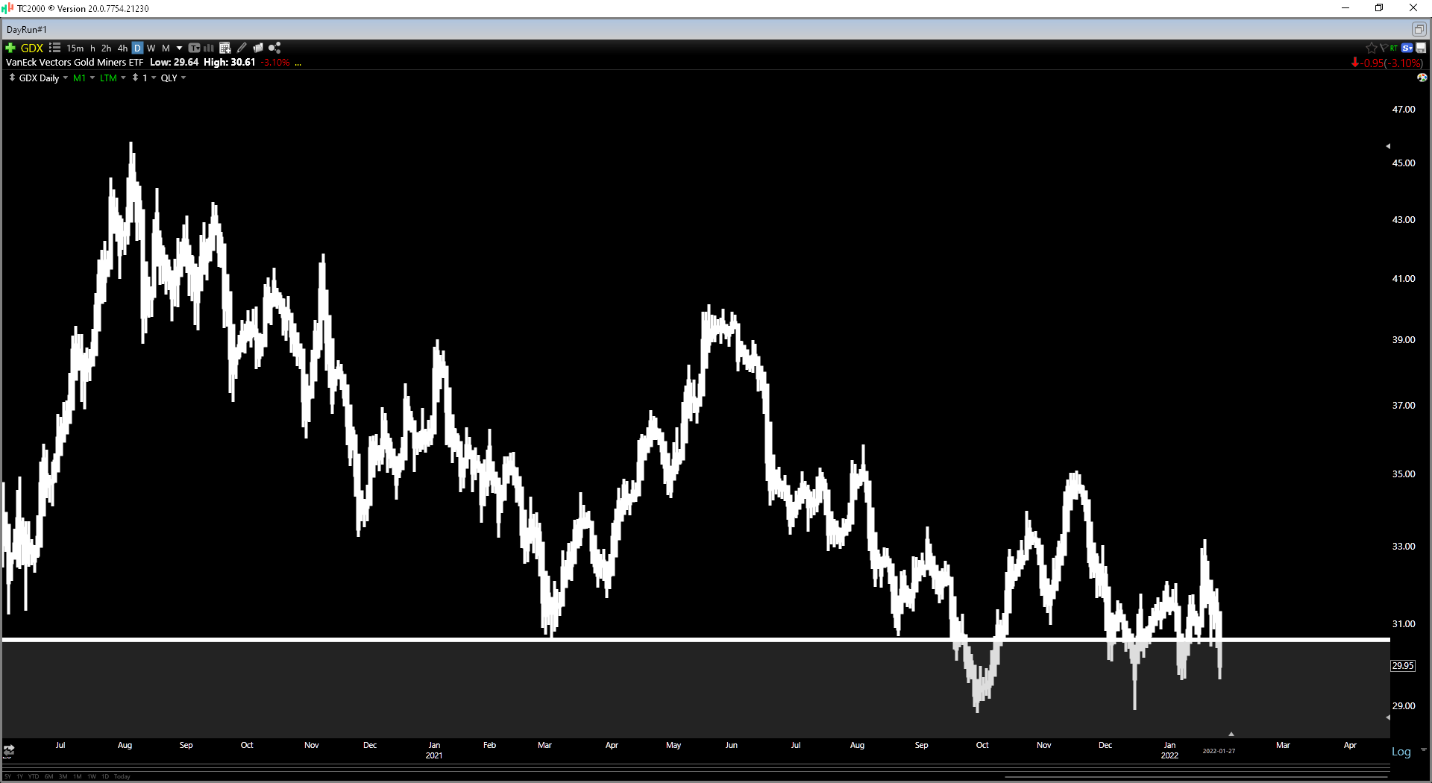

It's been a tough 18-month stretch for the Gold Miners Index (GDX), with the ETF sliding more than 30% from its highs. While some of this weakness is related to the gold (GLD) price, the other culprit is inflationary pressures, which have taken a bite out of margins for some miners. However, not all miners are created equal, and some have been thrown out with the bathwater. In this update, we'll look at three that make excellent buy-the-dip candidates.

(Source: TC2000.com)

The preferred way to get exposure to the gold price is through GLD or GDX, with the latter offering more leverage. This is because producers can see a significant increase in their margins when the gold price moves higher. However, while the GDX does offer diversification with 50+ holdings, this diversification is its Achilles' heel. This is because 70% of miners are not worth owning, which leads to the worst producers with declining margins dragging down the index.

The way to achieve superior returns is to own the best producers/royalty companies in the sector and buy them at the right price. There are several available at the right price when it comes to high-quality names, but three stand out as having superior fundamentals, attractive dividend yields, and strong growth. These three names are Agnico Eagle Mines (AEM), Wheaton Precious Metals (WPM), and Alamos Gold (AGI). Let's take a closer look at the three companies below:

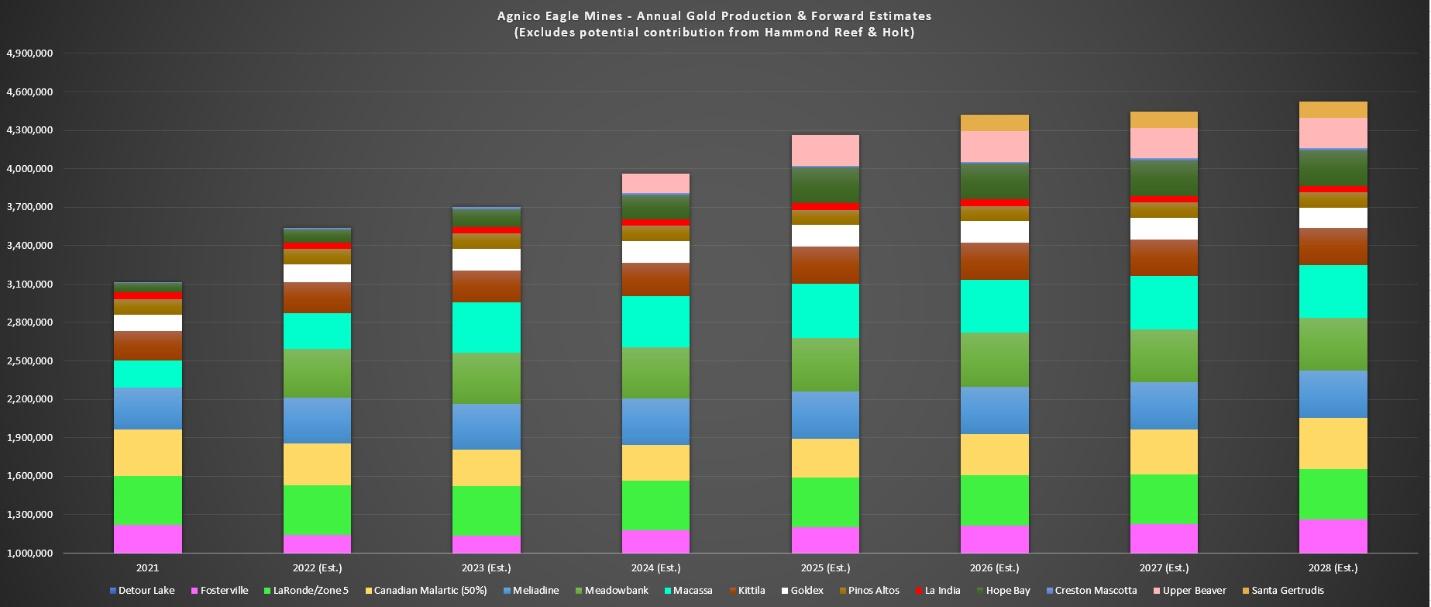

Beginning with Agnico Eagle Mines, the company is set to complete its merger with Kirkland Lake Gold (KL) in the next couple of weeks, making it one of the world's largest gold producers. The combined entity is expected to produce roughly ~3.4 million ounces of gold in FY2022 on a conservative basis and could grow to become a ~4.5-million-ounce producer by FY2028. This represents 33% growth from current levels, which is well above the production growth rate of its peer group, with companies like Barrick expecting minimal production growth over the next several years.

(Source: Company Filings, Author's Chart & Estimates)

The source of this sharp increase in total production comes from organic growth at current mines and the expectation that new projects will come online, with these including Upper Beaver and Santa Gertrudis, two advanced-stage projects in Canada and Mexico. Within the portfolio, Detour Lake is expected to steadily ramp up to more than 850,000 ounces per annum (2021 production: 712,000 ounces), while Macassa's annual production is projected to grow to 400,000+ ounces (FY2021: production ~210,000 ounces).

The exciting part about this growth is that not only is the company expected to see a meaningful increase in production, but incremental growth is expected to come from higher-margin assets. This includes Upper Beaver, which should produce at below $850/oz with by-product credits, Santa Gertrudis, which should have costs below $850/oz as well, and Detour Lake, which is expected to see costs dip below $775/oz at a higher production profile.

Finally, Macassa is likely to see costs dip below $650/oz once production heads above 400,000 ounces per annum. Hence, Agnico's growth should be accompanied by higher margins, with a potential increase in the gold price benefiting margins even further. Based on Agnico's current operating/development projects portfolio, the company's combined NPV (5%) on mining assets comes in above $23BB, which is well above its current market cap of $21BB.

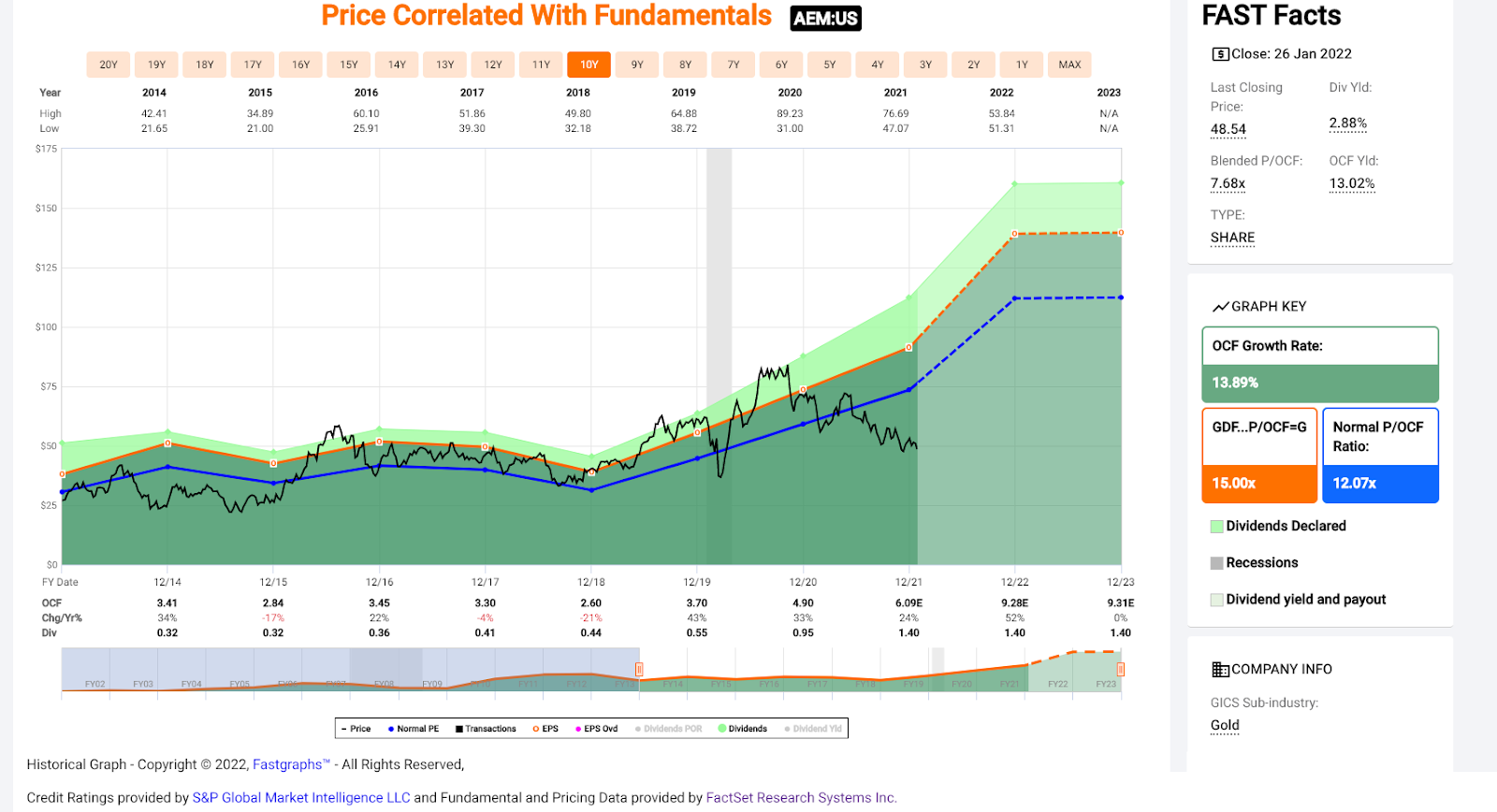

(Source: FASTGraphs.com)

With AEM typically commanding a large premium to net asset value, I see an upside to more than $70.00 per share. The bonus is that AEM has one of the most attractive dividend yields sector-wide, currently paying an annualized dividend yield near ~3.00%. Finally, the company should be nearly debt-free by Q2 2022, providing ample room to supplement dividends with share buybacks to return capital to shareholders. So, at a share price of $47.00, I see significant upside from current levels, and I plan to continue to accumulate on weakness.

The second name on the list worth paying attention to is Wheaton Precious Metals (WPM). This streaming company helps to fund producers/developers with an up-front payment in exchange for the delivery of a portion of production over their mine life. The company has a market cap of $17.5BB, has an attributable production profile of more than 740,000 ounces, and expects to see production average of 825,000+ gold-equivalent ounces per annum over the next five years.

(Source: Company Filings, Author's Chart)

Given its extremely high margins due to its streaming model (capex-light model), the company is not impacted by inflationary pressures and has much lower risk than its peers. However, the company does benefit immensely from new discoveries and expansions on its partner projects, which boosts the company's total attributable production and its long-term revenue (longer mine life). So, WPM is one of the best ways to play the sector for investors who want exposure to the sector at the lowest risk

(Source: FASTGraphs.com)

If we look at WPM's valuation above, we can see that the stock has historically traded at 35x earnings yet currently trades at just 27x FY2023 earnings estimates. This is a very reasonable valuation, especially considering that the gold price is sitting at much higher levels than it averaged over the past seven years when WPM commanded an earnings multiple of 35. Based on what I believe to be a fair earnings multiple closer to 36, given that WPM enjoys 75% plus margins, I see a fair value for the stock closer to $52.00 per share. So, at $38.00, this looks like a low-risk entry point into the stock.

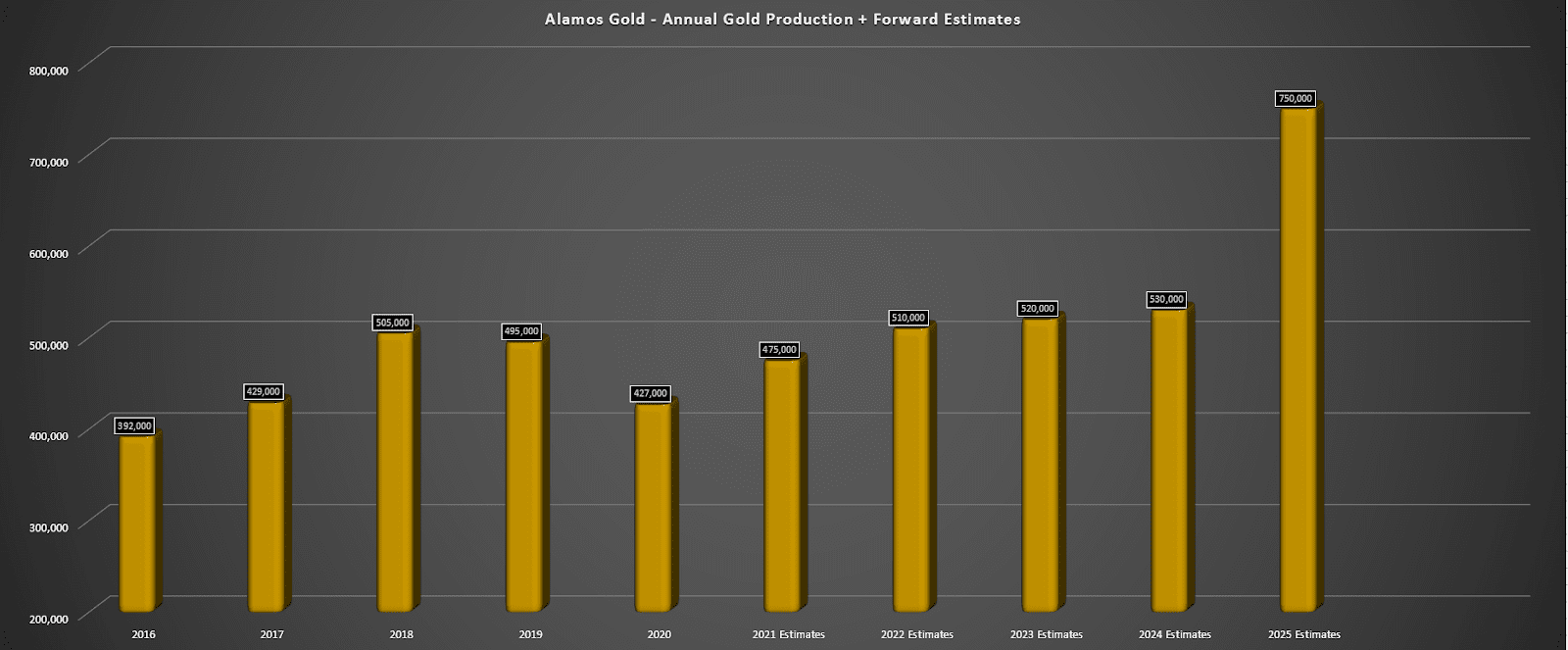

The final name on the list is Alamos Gold (AGI), a mid-tier gold producer with three mines, two located in Canada and one in Mexico. The stock has seen a sharp sell-off over the past 18 months due to the lower gold price and higher costs from its Mulatos Project in Mexico. However, the company is set to transform over the next few years, growing from a 480,000-ounce producer with costs of $1,150/oz to a 750,000-ounce producer with costs below $850/oz.

(Source: Company Filings, Author's Chart)

This makes Alamos one of the best growth stories sector-wide, and it will help the company to become one of the highest-margin producers sector-wide in 2025, which should translate to a higher multiple for the stock. For those unfamiliar with the story, this growth is expected to come from a major expansion at its high-grade Island Gold Mine in Ontario and a new mine, Lynn Lake, in Manitoba.

Based on 396MM shares outstanding, AGI currently trades at a market cap of $2.62BB, which pales in comparison to its estimated NPV (5%) of $3.9BB. With a current share buyback program in place that should reduce the share count further and help provide support at current levels and a 1.0%+ dividend yield, I see this as a low-risk entry point into the stock. Based on a multiple of 1.1x P/NAV, I see a fair value of $11.00 for the stock, or more than 60% upside to its 18-month target price.

In more than a decade trading the gold sector, I do not recall the last time the sector was this hated, except for near the lows of the secular bear market in 2015. The difference this time around is that the average mine is generating significant free cash flow is much more disciplined with capital allocation, and has a strong balance sheet, which makes this a very low-risk entry point into the sector to diversify one's portfolio. Based on AEM, WPM, and AGI being high-quality businesses at a reasonable price, I see this as a buying opportunity for all three.

Disclosure: I am long GLD, AEM, AGI

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.

WPM shares were trading at $38.67 per share on Friday afternoon, down $0.34 (-0.87%). Year-to-date, WPM has declined -9.92%, versus a -8.11% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 High-Quality Gold & Silver Miners Trading at Attractive Valuations appeared first on StockNews.com