One of the most recognizable and prominent backers of the AI trade on Wall Street is the global head of technology research at the broking firm Wedbush, Dan Ives. Often seen drawing comparisons of the current AI megatrend to the second or third inning of a nine-inning game or a party that is at 10 PM that goes on until 4 AM, Ives's bullish references are as colorful as his jackets.

However, Ives's recommendations are serious ones, a number of them having been proven right over the years. Now, with the recent selloff in tech stocks, the analyst is betting big on these three stocks as his preferred AI plays. Let's take a look at them.

Dan Ives' Top 3 Stocks: Nvidia (NVDA)

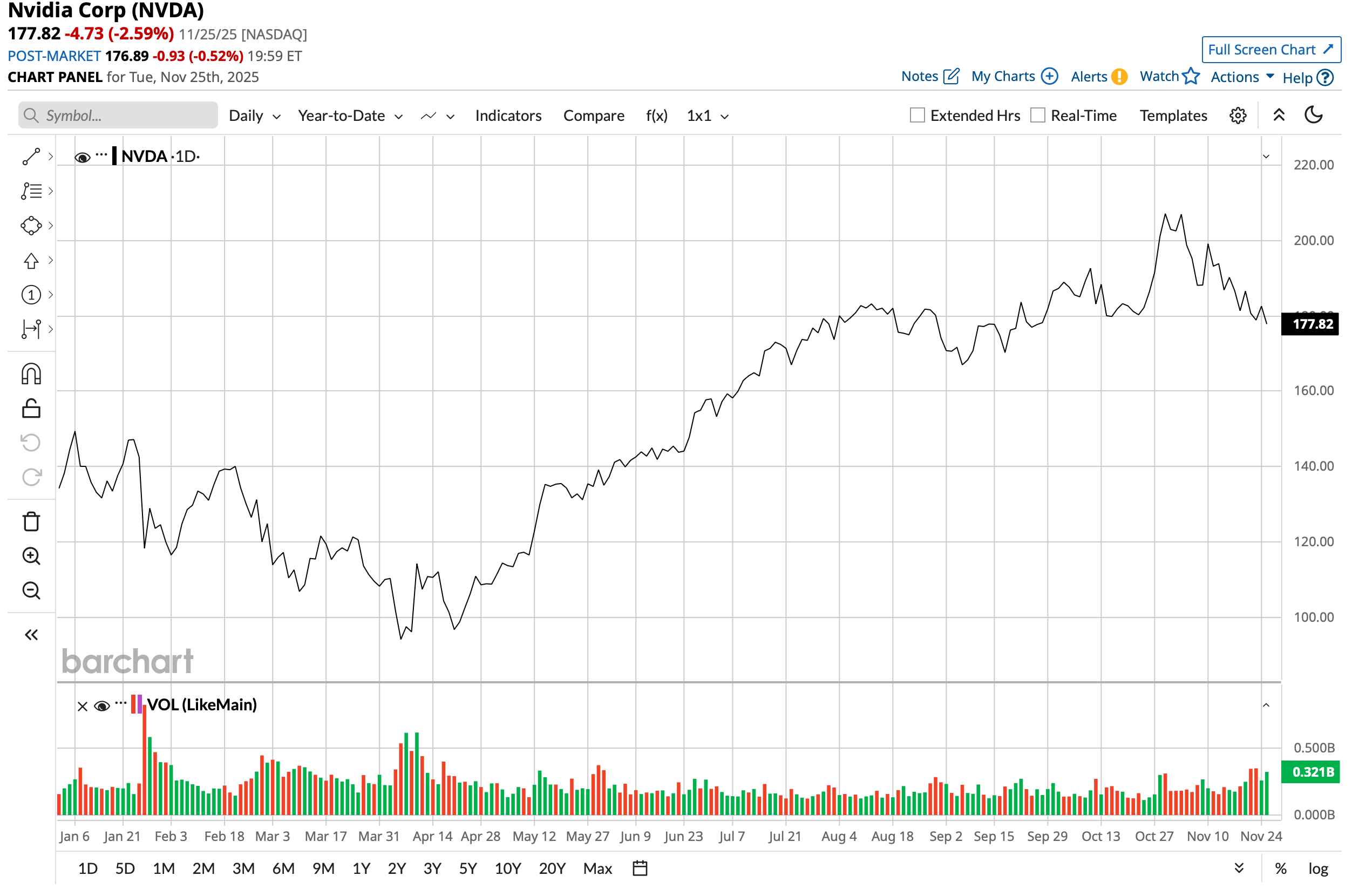

Chief among Ives's picks is the world's most valuable company and semiconductor giant, Nvidia (NVDA). Founded in 1993 with current CEO Jensen Huang (whom Ives refers to as the Godfather of AI) as one of its co-founders, Nvidia invented the GPU (graphics processing unit), which revolutionized computer graphics and enabled high-performance gaming and graphics-heavy applications. Over time, GPUs (and related hardware) became foundational for AI work like model training, inference, and data center workloads. Nvidia now sells data center-scale hardware/software, AI acceleration, networking, etc.

Valued at a market cap of $4.4 trillion, the NVDA stock is a bona fide multibagger, having rallied by a mammoth 1,211% over the past five years. On a year-to-date (YTD) basis, the stock is up 35%.

Notwithstanding its leadership position in the GPU market, Nvidia is a financial powerhouse as well, with its revenue and earnings clocking CAGRs of 44.06% and 66.66%, respectively. Along with that, the company has a strong track record of consecutive quarterly earnings beats over the past several years.

The trend continued in the most recent quarter as well. In Q3 FY26, Nvidia reported revenues of $57 billion, up 62% from the previous year, as the core data center revenue went up by 66% in the same period to $51.2 billion. Earnings went up by an even sharper 67% yearly to $1.30, coming in ahead of the consensus estimate of $1.26.

Net cash from operating activities for the quarter came in at $23.8 billion, higher than the prior year's figure of $17.6 billion. Overall, Nvidia closed the quarter with a cash balance of $60.6 billion, dwarfing its short-term debt levels of $999 million.

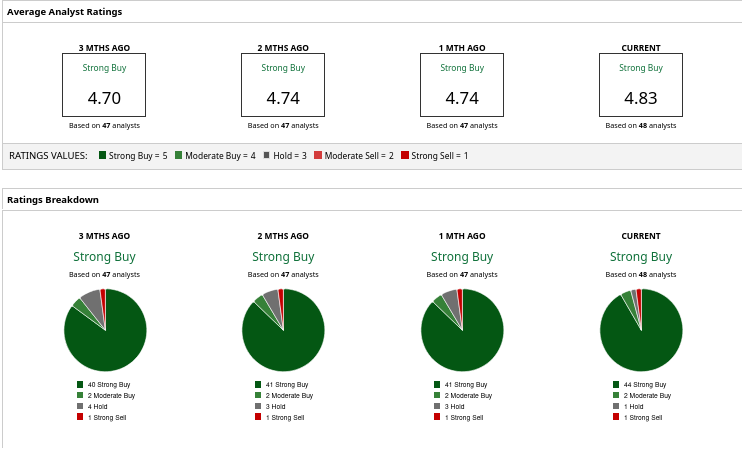

Thus, analysts have deemed the NVDA stock a consensus “Strong Buy,” with a mean target price of $252.33, which denotes an upside potential of about 42% from current levels. Out of 48 analysts covering the stock, 44 have a “Strong Buy” rating, two have a “Moderate Buy” rating, one has a “Hold” rating, and one more has a “Strong Sell” rating.

Dan Ives' Top 3 Stocks: AMD (AMD)

Next up on Ives's list is Advanced Micro Devices, or AMD (AMD). Occupying the runner-up position in the market that Nvidia leads, AMD was founded much earlier, in 1969. Currently, AMD is a diversified semiconductor company supplying hardware (and some associated software) across many sectors. Major business areas include GPUs, CPUs, embedded systems, semi-custom chips, and specialized hardware.

The company's current market cap stands at $350.1 billion, with AMD stock rocketing 76% and 119% on a YTD and five-year basis, respectively.

Meanwhile, the Lisa Su-led company may not have as storied a track record of earnings beats as its much bigger rival above, but AMD's fundamentals remain solid.

AMD has demonstrated solid financial momentum, with revenue and earnings advancing 29.94% and 28.93%, respectively, on a compound basis over the past five years. This trajectory carried into the latest reporting period, where the company once again surpassed analyst projections across key metrics.

For the third quarter of 2025, total revenue registered $9.25 billion, reflecting a robust 36% increase from the year-earlier figure. The data center division contributed $4.3 billion to that total, up 22% year-over-year (YoY), while the client and gaming unit delivered a standout 73% surge to $4 billion.

On the profitability side, earnings per share climbed 30% to $1.20, clearing the consensus forecast of $1.17. This performance extends AMD's streak of consecutive quarterly earnings beats to four.

Liquidity metrics remained a bright spot as well, with operating cash flow nearly tripling to $1.8 billion from $628 million in the prior-year quarter. The company wrapped up the period holding $4.81 billion in cash, a figure that comfortably exceeds its short-term borrowings of $873 million and long-term debt of $2.35 billion.

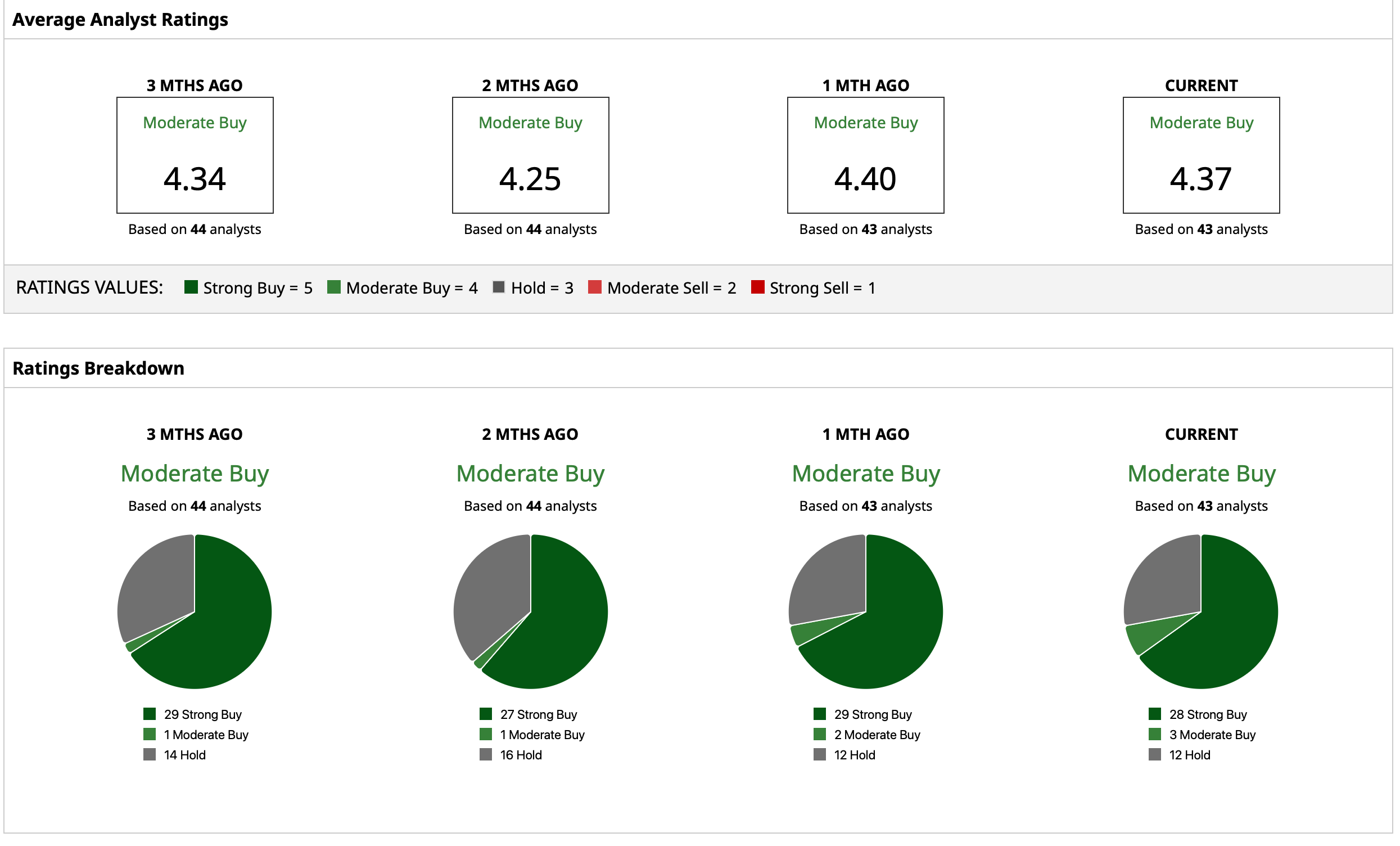

Considering this, analysts have earmarked an overall rating of “Moderate Buy” for the stock. The mean target price of $291.29 indicates an upside potential of about 41% from current levels. Out of 43 analysts covering the stock, 28 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and 12 have a “Hold” rating.

Dan Ives' Top 3 Stocks: Palantir (PLTR)

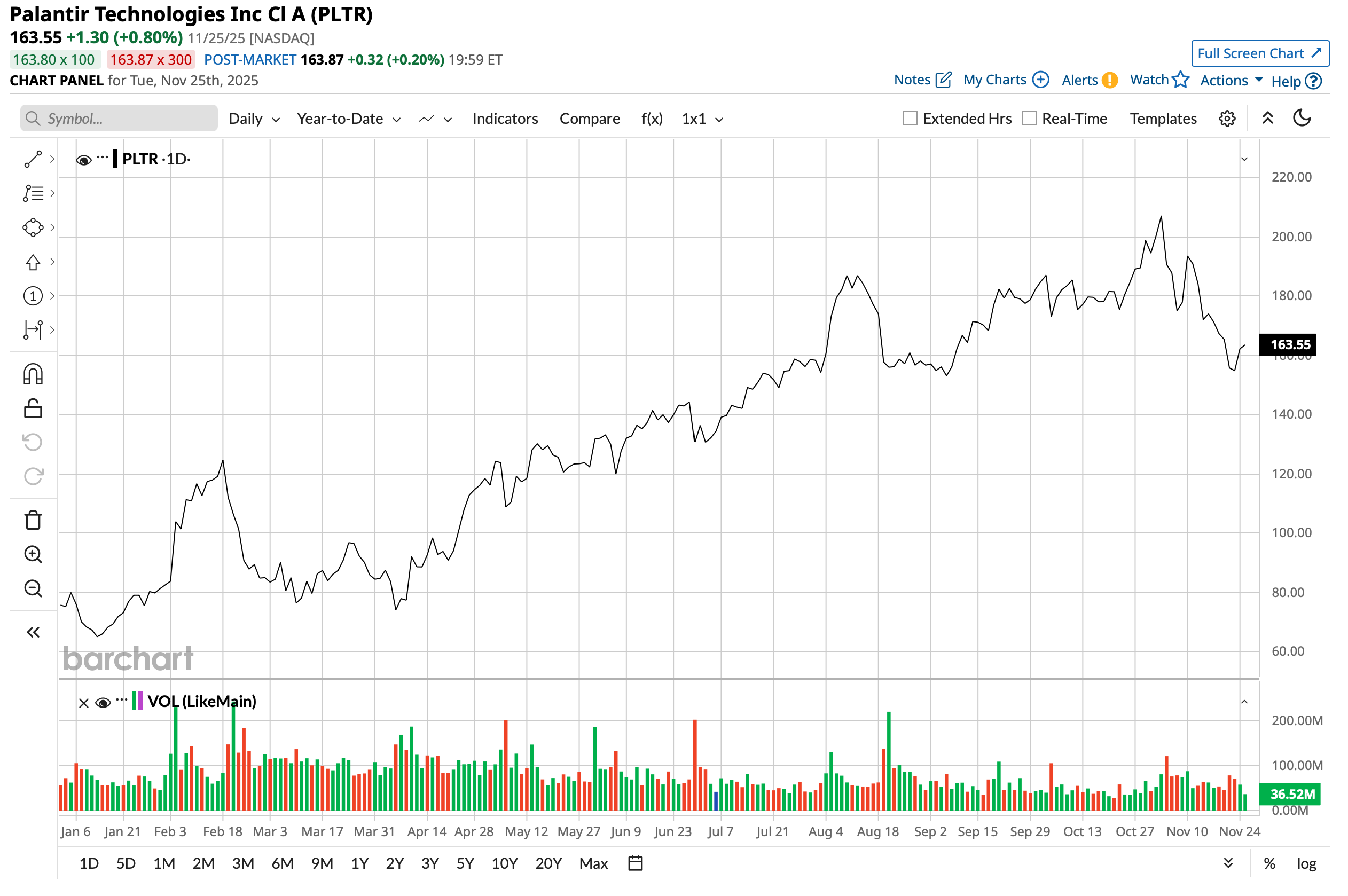

We conclude our list with the company that Ives has given the moniker of “Messi of AI,” Palantir (PLTR). Helmed by the outspoken Alex Karp and backed by Peter Thiel, Palantir is a software company specializing in big data analytics, data integration, and AI-enabled decision-making platforms. Its products serve both government (defense, intelligence, and law enforcement) and commercial customers across many industries.

With a current market cap of $386.7 billion, PLTR has more than doubled so far this year, rising 120% on a YTD basis and 586% on a five-year basis.

Meanwhile, the share price rally has been a consequence of its robust financial showing, as the company's quarterly earnings have surpassed expectations over the past two years consecutively.

The story remained the same in Q3 2025 as well. Revenue for the quarter came in at $1.2 billion, up 62.8% from the previous year. Further, earnings went up by a staggering 110% in the same period to $0.21 per share, higher than the consensus estimate of $0.17.

Net cash from operating activities for the nine months ended Sept. 30 surged to $1.36 billion from $693.54 million in the year-ago period as the company closed the quarter with a cash balance of $1.62 billion. This was much higher than its short-term debt levels of $46.3 million.

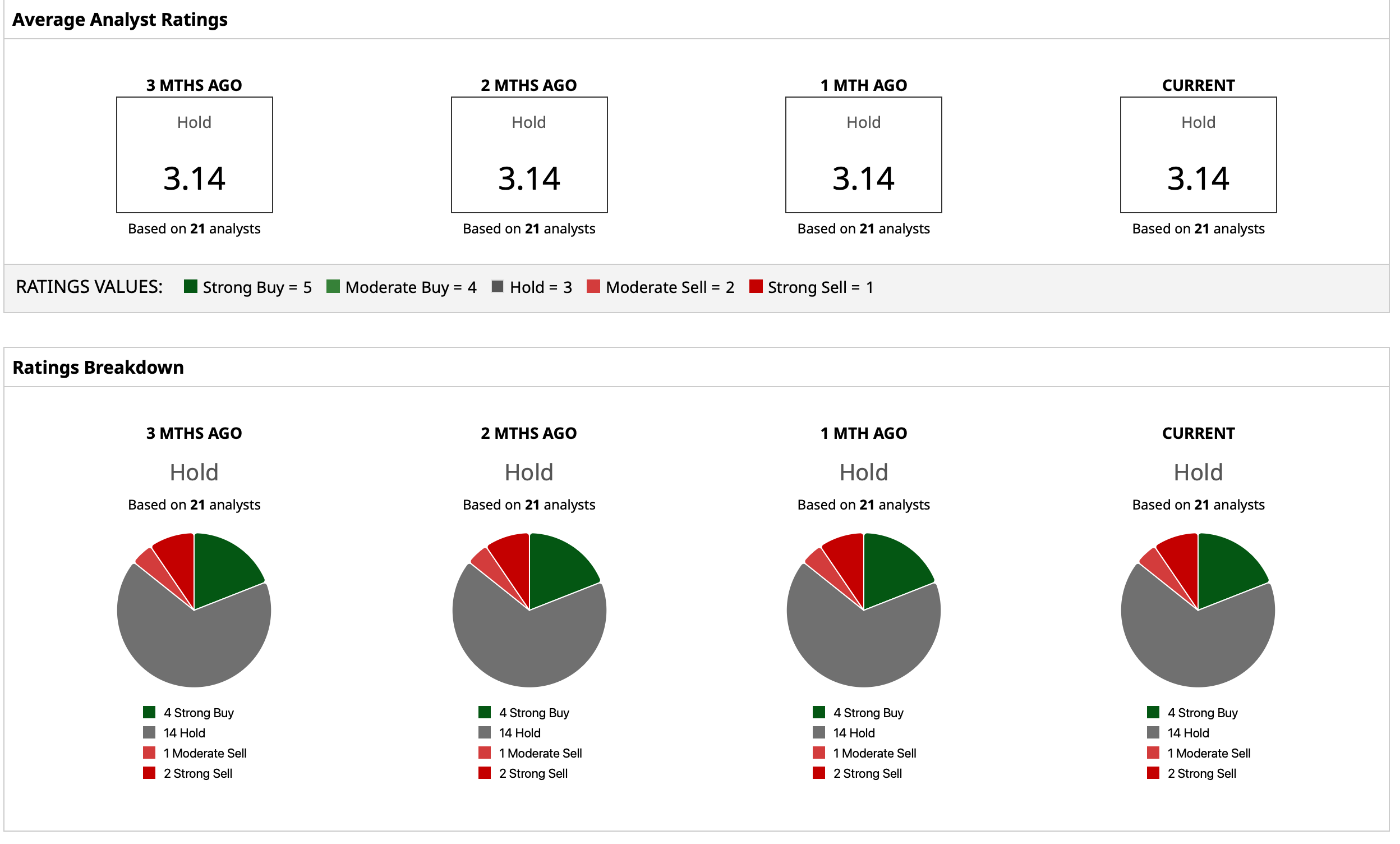

Taking this into account, analysts have attributed a rating of “Hold” for the PLTR stock, primarily due to its hefty valuations after the searing rally. The mean target price of $192.67 indicates an upside potential of roughly 18% from current levels. Out of 21 analysts covering the stock, four have a “Strong Buy” rating, 14 have a “Hold” rating, one has a “Moderate Sell” rating, and two have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart