Over the last six months, ON Semiconductor’s shares have sunk to $66.97, producing a disappointing 9.5% loss - a stark contrast to the S&P 500’s 12.4% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in ON Semiconductor, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why you should be careful with ON and a stock we'd rather own.

Why Is ON Semiconductor Not Exciting?

Spun out of Motorola in 1999 and built through a series of acquisitions, ON Semiconductor (NASDAQ: ON) is a global provider of analog chips specializing in autos, industrial applications, and power management in cloud data centers.

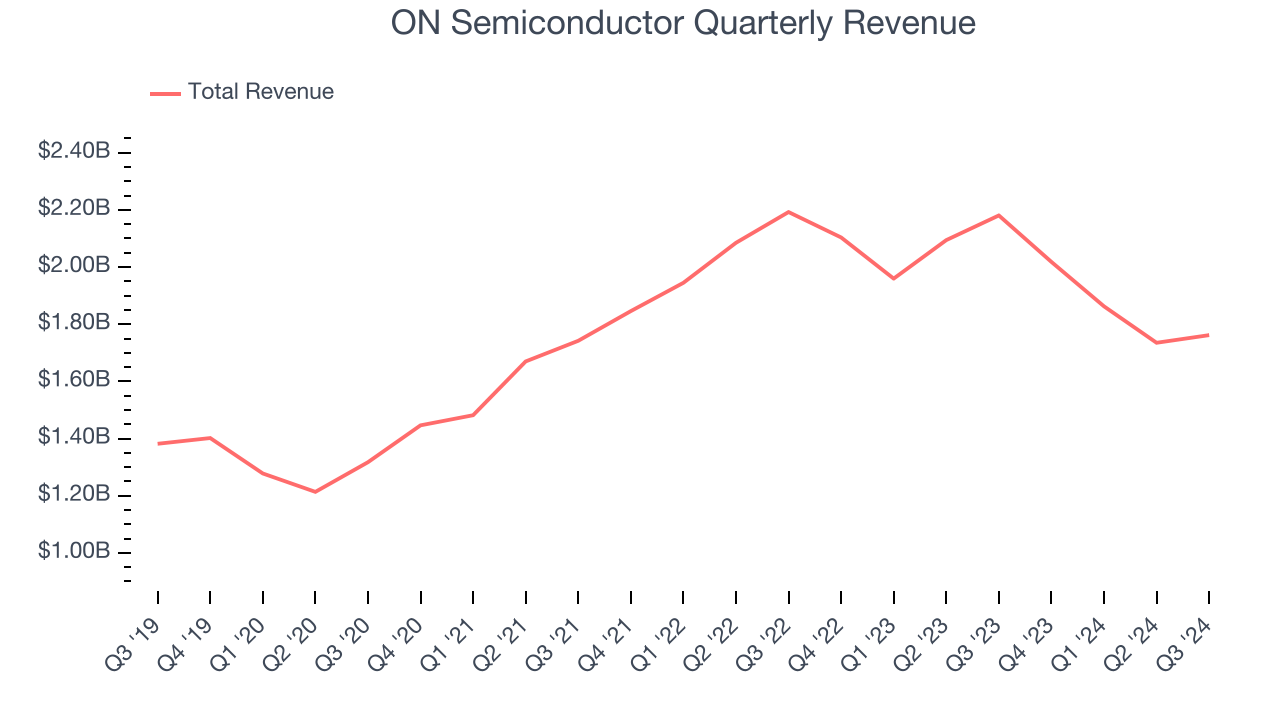

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, ON Semiconductor’s 5.6% annualized revenue growth over the last five years was tepid. This fell short of our benchmark for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

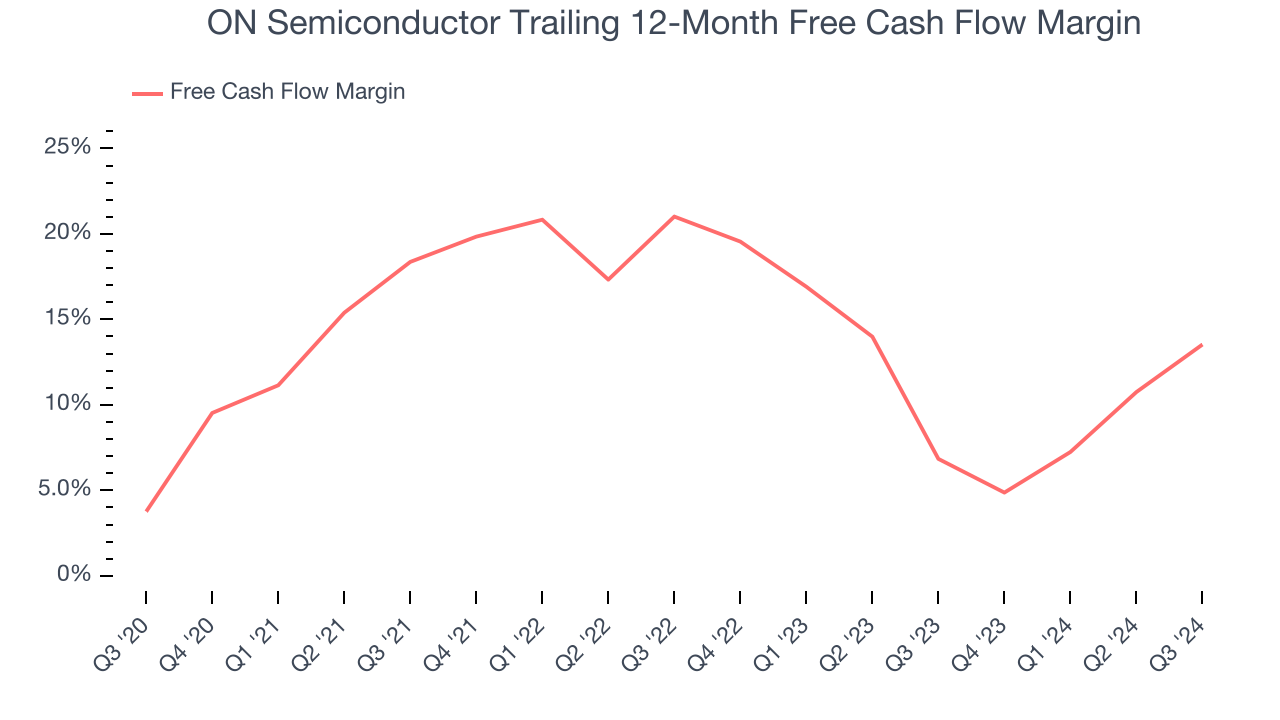

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

ON Semiconductor has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 10%, subpar for a semiconductor business. The divergence from its good operating margin stems from its capital-intensive business model, which requires ON Semiconductor to make large cash investments in working capital and capital expenditures.

3. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect ON Semiconductor’s revenue to stall. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

Final Judgment

ON Semiconductor isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 15.1× forward price-to-earnings (or $66.97 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d suggest looking at KLA Corporation, a picks and shovels play for semiconductor manufacturing.

Stocks We Would Buy Instead of ON Semiconductor

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.