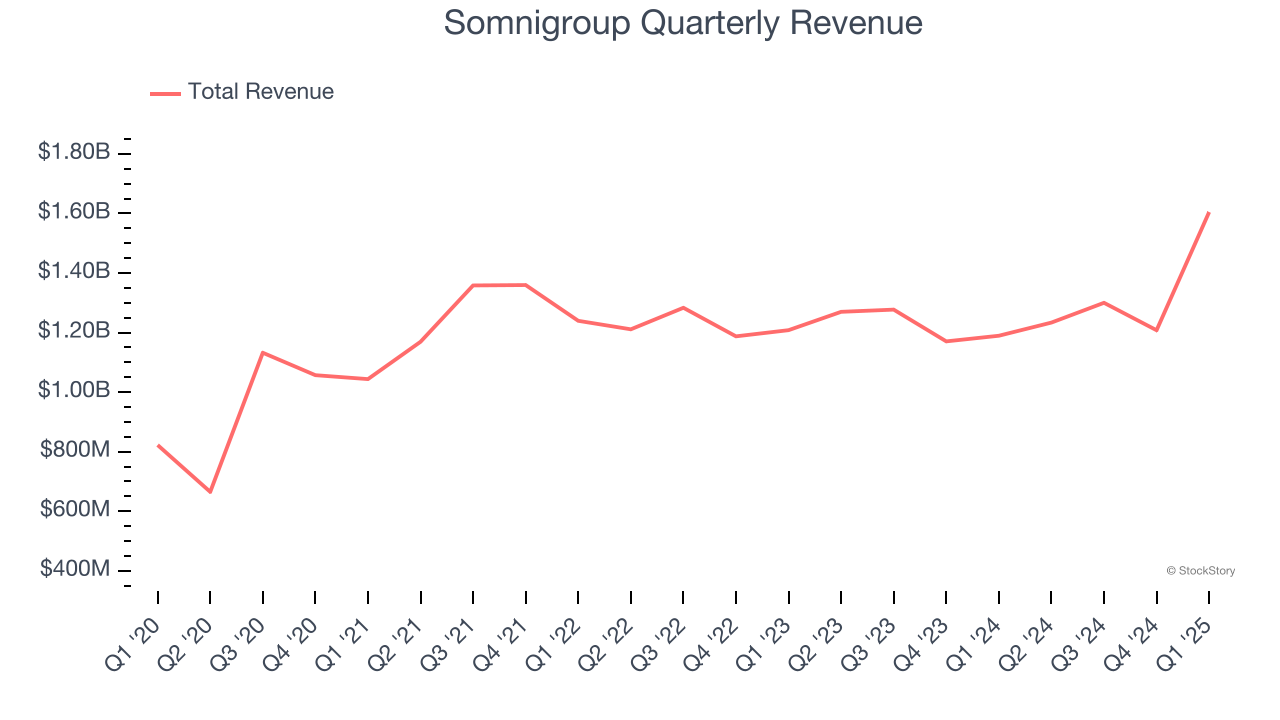

Bedding manufacturer Somnigroup (NYSE: SGI) missed Wall Street’s revenue expectations in Q1 CY2025, but sales rose 34.9% year on year to $1.60 billion. Its non-GAAP profit of $0.49 per share was 5.1% above analysts’ consensus estimates.

Is now the time to buy Somnigroup? Find out by accessing our full research report, it’s free.

Somnigroup (SGI) Q1 CY2025 Highlights:

- Revenue: $1.60 billion vs analyst estimates of $1.63 billion (34.9% year-on-year growth, 1.8% miss)

- Adjusted EPS: $0.49 vs analyst estimates of $0.47 (5.1% beat)

- Adjusted EBITDA: $247.9 million vs analyst estimates of $255.6 million (15.4% margin, 3% miss)

- Management lowered its full-year Adjusted EPS guidance to $2.47 at the midpoint, a 11.6% decrease

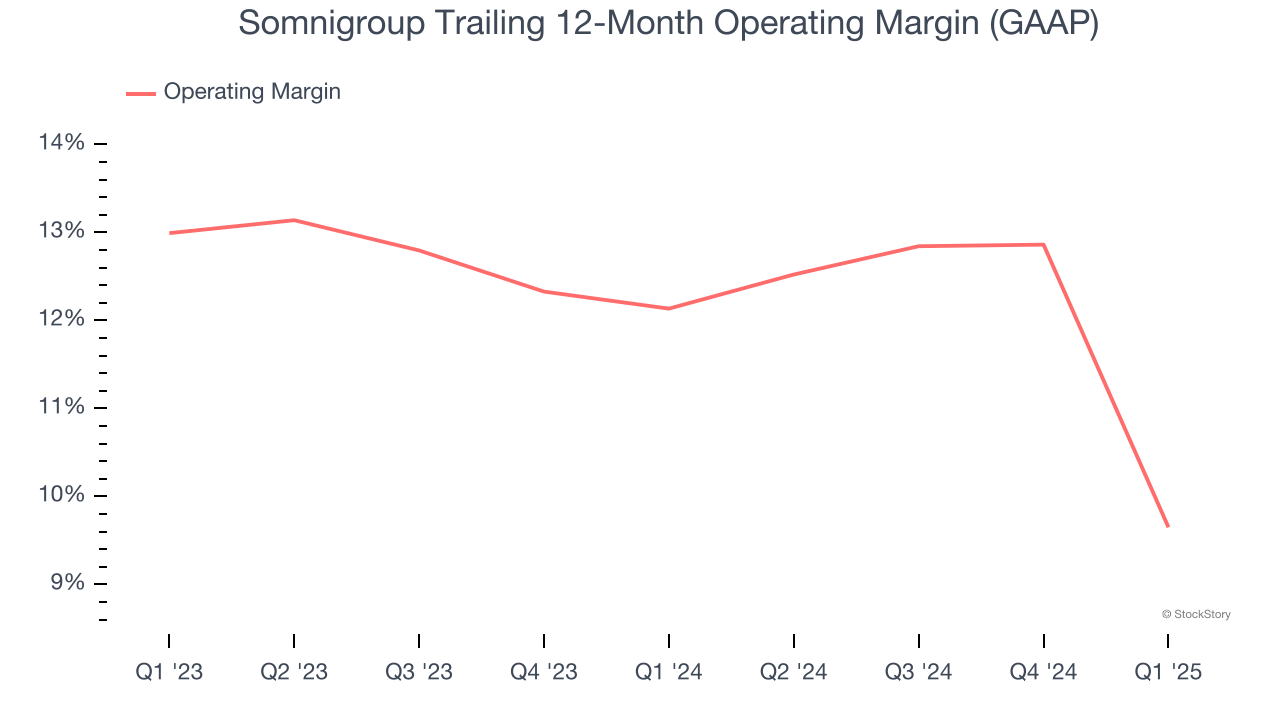

- Operating Margin: 0.8%, down from 11.1% in the same quarter last year

- Free Cash Flow Margin: 5.1%, down from 8.3% in the same quarter last year

- Market Capitalization: $12.64 billion

Company Chairman and CEO Scott Thompson commented, "Our results this quarter both reflect the transformational acquisition of Mattress Firm and highlight our ability to navigate a weak global market. All of our business units, domestically and internationally, successfully made progress on their growth opportunities as we leverage the core strengths of our business, including scale, operational flexibility and manufacturing capabilities. I continue to be impressed by our people, all around the world, as they focus on execution and taking care of our customers to deliver share gains and efficient cost management across the Somnigroup enterprise. Everyone in the organization has stepped up to quickly advance our near and longer term initiatives to continue delivering value to shareholders."

Company Overview

Established through the merger of Tempur-Pedic and Sealy in 2012, Somnigroup (NYSE: SGI) is a bedding manufacturer known for its innovative memory foam mattresses and sleep products

Sales Growth

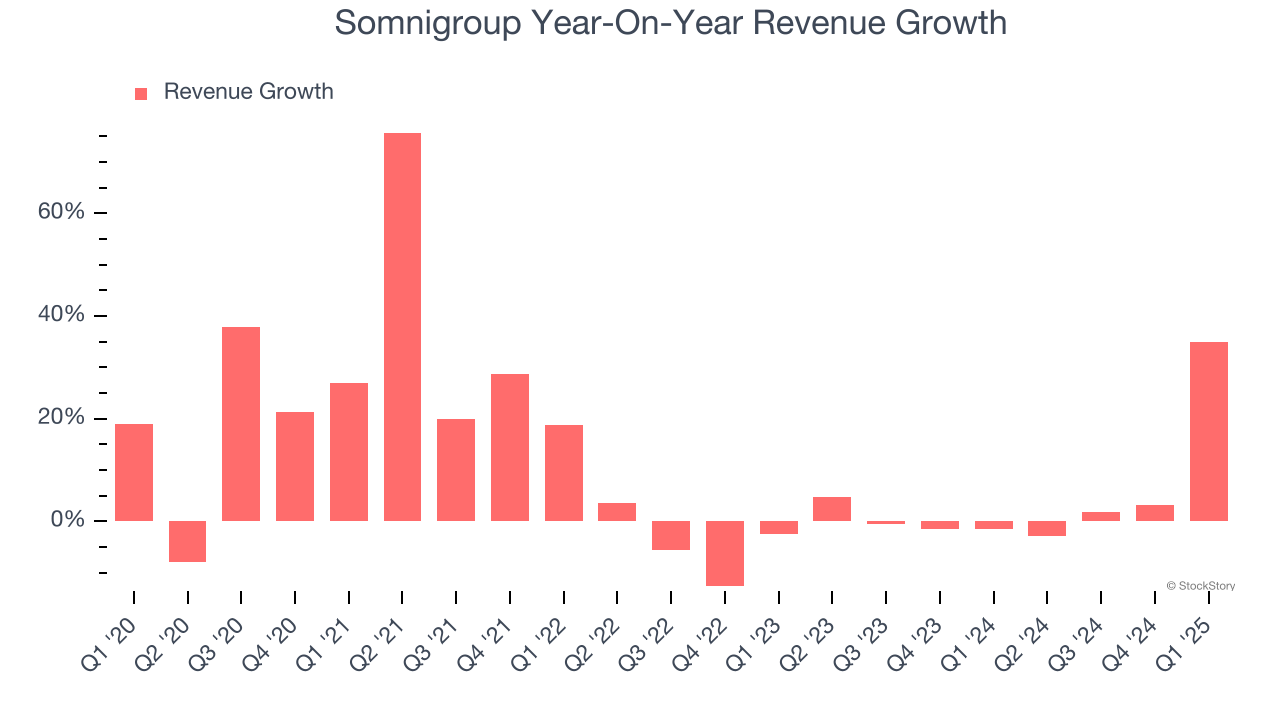

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Somnigroup grew its sales at a 10.6% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Somnigroup’s recent performance shows its demand has slowed as its annualized revenue growth of 4.6% over the last two years was below its five-year trend.

We can better understand the company’s revenue dynamics by analyzing its most important segments, Wholesale and Direct, which are 43.5% and 56.5% of revenue. Over the last two years, Somnigroup’s Wholesale revenue (sales to retailers) averaged 3.4% year-on-year declines. On the other hand, its Direct revenue (sales made directly to consumers) averaged 29.2% growth.

This quarter, Somnigroup pulled off a wonderful 34.9% year-on-year revenue growth rate, but its $1.60 billion of revenue fell short of Wall Street’s rosy estimates.

Looking ahead, sell-side analysts expect revenue to grow 48.8% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Somnigroup’s operating margin has shrunk over the last 12 months, but it still averaged 10.8% over the last two years, decent for a consumer discretionary business. This shows it generally does a decent job managing its expenses.

This quarter, Somnigroup’s breakeven margin was down 10.2 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

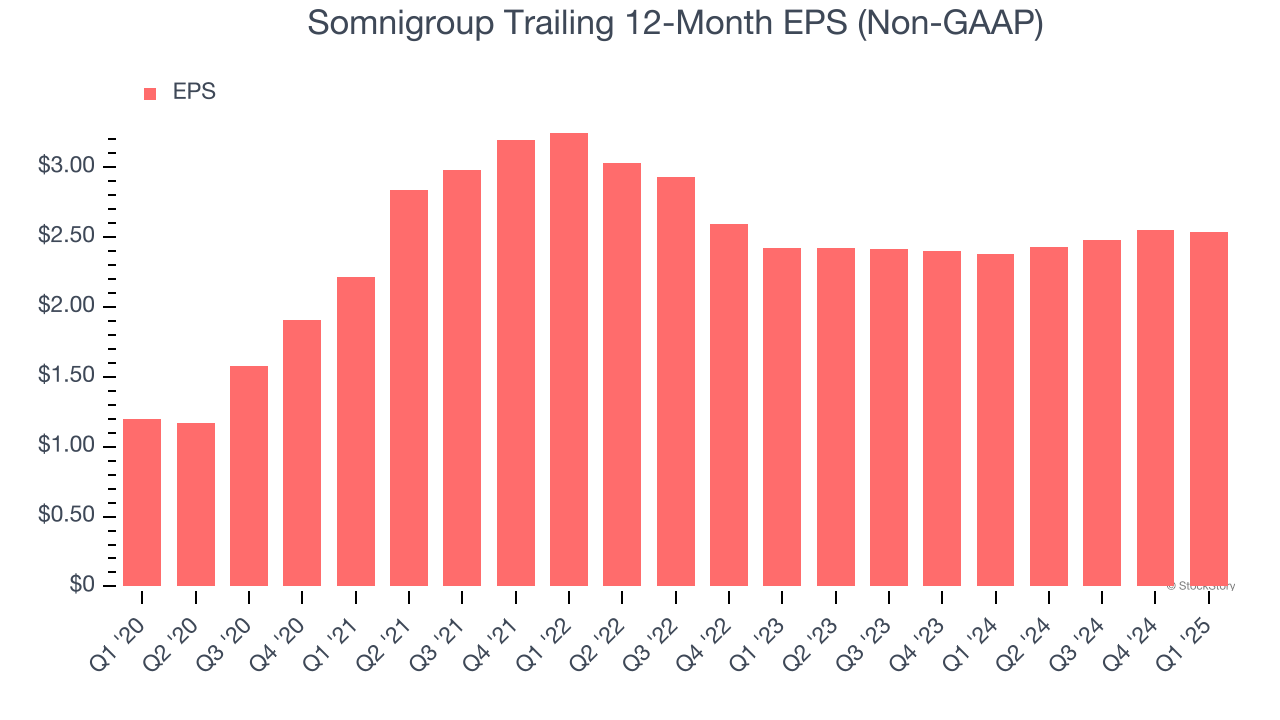

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Somnigroup’s EPS grew at a remarkable 16.2% compounded annual growth rate over the last five years, higher than its 10.6% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t expand.

In Q1, Somnigroup reported EPS at $0.49, down from $0.50 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 5.1%. Over the next 12 months, Wall Street expects Somnigroup’s full-year EPS of $2.54 to grow 13%.

Key Takeaways from Somnigroup’s Q1 Results

It was encouraging to see Somnigroup beat analysts’ EPS expectations this quarter. On the other hand, its full-year EPS guidance missed significantly and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 5.9% to $57.03 immediately following the results.

The latest quarter from Somnigroup’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.