SANTIAGO, Chile, May 22, 2014 /PRNewswire/ -- GeoPark Limited (GeoPark) (NYSE: GPRK), the Latin American oil and gas explorer, operator and consolidator with operations and producing properties in Chile, Colombia, Brazil and Argentina, today reported results for 1Q2014.

All figures are expressed in US dollars. All growth comparisons refer to the same period of the prior year, except when specified. Proforma figures in this release refer to the incorporation in both periods of the acquired interest in the Manati Field (Brazil), which was closed on March 31, 2014.

FIRST QUARTER 2014 HIGHLIGHTS

Operations:

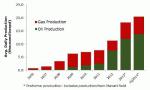

- Oil and gas production up 25% to 16,743 boepd compared to 1Q2013. Proforma, average production reached 20,410 boepd

- 15 new wells drilled during 1Q2014, seven exploration wells and eight development and appraisal wells

- New oil field discovery (Aruco 1 on the Llanos 34 Block) in Colombia

- Two new oil field discoveries in Chile (Loij 1 in the Fell Block and Tenca 1 in the Flamenco Block). Four exploratory wells drilled in 1Q2014 will be completed and tested in 2Q2014

- Start-up of commercial production in the Tierra del Fuego blocks in Chile, with a gross average of 374 boepd in 1Q2014, and a gross average of 1,084 boepd in March 2014 (542 boepd net to GeoPark)

- Signed service contracts to acquire 3D seismic in the blocks awarded in Round 11 in Brazil

Finance:

- Profit for the period up 9% to $10.3 million

- Net Revenues down 6% to $84.7 million and Adjusted EBITDA down 3% to $48.4 million, both impacted by oil delivery delays (please see note below)

- Cash position of $131.9 million at the close of 1Q2014

Strategic / New Business:

- Transitioned from the London AIM Market (AIM) to the New York Stock Exchange (NYSE) in February 2014, raising approximately $100 million of gross proceeds in the Initial Public Offering (IPO)

- Completed acquisition of 10% interest in the Manati gas field in Brazil, funded with existing cash and new debt amounting to $70 million

- Signed the license agreement with the ANP (Agencia Nacional do Petroleo, Brazil's National Agency of Petroleum) for the Sergipe Alagoas Block in Brazil awarded during Round 12

Note: The significant increase in GeoPark's Colombian oil production of 88% in 1Q2014 was not entirely reflected in net revenues or Adjusted EBITDA for the period, mainly due to some delays in oil deliveries and increased oil inventory. During the first quarter of 2014, Ecopetrol allocated larger volumes of its own oil production to exports because of an oil refinery shut down, temporarily affecting the volumes received from GeoPark and other Colombian oil producers at the port of Covenas. This situation has normalized in May 2014, and is not expected to generate any impact on the Company's 2014 results.

James F. Park, GeoPark Chief Executive Officer, said, "In February 2014, GeoPark made an important transition from the London AIM to the NYSE, where we look forward to reaching a wider audience of investors to share our story of performance, growth and opportunity. We also successfully raised additional funds from the IPO to support our new business expansion. Our on-the-ground operations and drilling activity in Colombia and Chile during the first quarter, as part of our active full year $220 million to $250 million work program, has already seen improved results and growth, with proforma production for the quarter in excess of 20,000 boepd. With these advances we continue to build on GeoPark's longstanding track record of production, reserves, and cash flow growth."

FIRST QUARTER 2014

The table below sets forth GeoPark's production figures for 1Q2014 compared with 1Q2013.

In addition, it includes proforma information for Brazil.

First Quarter 2014 | First Quarter 2013 | |||||

Total (boepd) | Oil (bopd) | Gas (mcfpd) | Total (boepd) | % Chg. | ||

Chile | 7,407 | 4,475 | 17,588 | 8,436 | -12% | |

Colombia | 9,265 | 9,232 | 196 | 4,938 | 88% | |

Argentina | 71 | 57 | 84 | 52 | 38% | |

Total | 16,743 | 13,765 | 17,868 | 13,426 | 25% | |

Plus: | ||||||

Brazil | 3,667 | 57 | 21,661 | 4,140 | -11% | |

Total Proforma | 20,410 | 13,821 | 39,529 | 17,566 | 16% | |

The table below sets forth some key indicators of performance for 1Q2014 compared with 1Q2013. These figures do not include proforma information for the interest in the Manati field in Brazil, which GeoPark will begin consolidating in its financial statements starting in 2Q2014. The Company agreed to the acquisition and started accumulating related cash as of May 2013, and received upon closing in March 2014.

Key Indicators | 1Q 2014 | 1Q 2013 | % Chg. | |

Oil production (bopd) | 13,765 | 10,481 | 31% | |

Gas production (mcfpd) | 17,868 | 17,671 | 1% | |

Average net production (boepd) | 16,743 | 13,426 | 25% | |

Average realized sales price | ||||

⁻ Oil ($ per bbl) | 85.6 | 90.2 | -5% | |

⁻ Gas ($ per mcf) | 6.5 | 4.4 | 48% | |

Net Revenues ($ million) | 84.7 | 89.8 | -6% | |

Adjusted EBITDA ($ million) | 48.4 | 49.7 | -3% | |

Profit for the period ($ million) | 10.3 | 9.4 | 9% | |

CONSOLIDATED OPERATING PERFORMANCE

Production: Consolidated production increased by 25% in 1Q2014 to 16,743 boepd. This growth was led by a 31% increase in consolidated oil production, primarily from higher oil production in the Colombian operations. On a proforma basis, average production grew 16% in 1Q2014. In addition, gas production increased by 1% to reach 17,868 mcfpd in 1Q2014.

Net Revenues: Consolidated net revenues decreased by 6% to $84.7 million in 1Q2014 compared to $89.8 million in 1Q2013, mainly impacted by the delays in oil deliveries in Colombia and which have normalized in May 2014.

Consolidated Oil Revenues: Consolidated oil revenues represented 89% of total net revenues in 1Q2014 compared to 93% in 1Q2013, down 10% to $75.2 million in 1Q2014, mostly as a result of delayed deliveries in Colombia and a decrease in oil production in Chile. This was also impacted by a lower realized oil price in Colombia, which resulted in a 5% decrease in the consolidated average realized oil price to $85.6 per barrel.

Consolidated Gas Revenues: Consolidated gas revenues increased by 57% to $9.5 million in 1Q2014 mainly due to higher average realized sales prices of 48%, reaching $6.5 per mcf in 1Q2014 compared to $4.4 per mcf in 1Q2013.

Gas revenues represented 11% of total net revenues in 1Q2014 compared to 7% in 1Q2013.

Costs: Consolidated production costs decreased by 2% to $37.7 million in 1Q2014, as a result of lower production costs in the Colombian operations, and partially offset by increased production costs in the Chilean operations.

Consolidated exploration costs decreased to $6.8 million in 1Q2014 from $7.3 million in 1Q2013, primarily as a result of lower write‑offs in Chile, where one well was written-off in 1Q2014 compared to two wells in 1Q2013, and in Colombia where no exploratory wells were written-off in 1Q2014 compared to one well in 1Q2013.

Consolidated administrative costs increased by 16% to $11.1 million in 1Q2014, mostly due to increased staff costs at the corporate level related to transition to the New York Stock Exchange, higher costs related to the start-up of the Brazilian operations, and new business expenses.

Consolidated selling expenses decreased by 20% to $6.3 million in 1Q2014, driven by reductions in Colombia.

Adjusted EBITDA: Consolidated Adjusted EBITDA decreased by 3% to $48.4 million in 1Q2014 compared to $49.7 million in 1Q2013. The decline was mainly driven by a decrease in the Adjusted EBITDA from the Colombian operations (from the delayed oil deliveries), and was partially offset by higher Adjusted EBITDA of the Chilean operations.

ANALYSIS BY BUSINESS SEGMENT

Operations in Chile

In Chile, GeoPark is the first and the largest non-state controlled oil and gas producer. Operations began in 2006 in the Fell Block and have evolved from having a non-operated, non-producing interest to a fully-operated and producing asset with 45.1 mmboe of 2P PRMS reserves certified by DeGolyer and McNaughton ("D&M") as of December 31, 2013. Average production in Fell Block amounted to 7,033 boepd during 1Q2014, representing 95% of GeoPark's Chilean production. In addition, the Company operates five other hydrocarbon blocks in Chile with significant prospective resources.

Key Indicators | 1Q2014 | 1Q2013 | % Chg. | |

Oil production (bopd) | 4,475 | 5,507 | -19% | |

Gas production (mcfpd) | 17,588 | 17,573 | 0% | |

Average net production (boepd) | 7,407 | 8,436 | -12% | |

Net Revenues ($ million) | 47.2 | 45.5 | 4% | |

Adjusted EBITDA ($ million) | 30.7 | 29.2 | 5% | |

Adjusted EBITDA per boe ($) | 48.5 | 38.4 | 26% |

Production: Production in Chile decreased by 12% to 7,407 boepd in 1Q2014 compared to 8,436 boepd in 1Q2013. GeoPark's production in 1Q2014 represented a 10% increase compared to 4Q2013, mainly due to new wells drilled, as well as some work-overs and the installation of electrical submersible pumps in certain existing Tobifera wells. GeoPark expects to replicate this artificial lift system (first time used in the basin) in 7-10 new wells on the Fell Block during 2014 to enhance production levels.

Net Revenues: Net revenues in Chile increased by 4% to $47.2 million for 1Q2014, representing 56% of consolidated net revenues, compared to $45.5 million or 51% of consolidated net revenues in 1Q2013.

Oil revenues decreased by 4% to $37.7 million in 1Q2014, due to lower production, which was partially offset by a higher average realized oil price per barrel.

The average realized oil price increased by 9% to $90.7 per barrel in 1Q2014, primarily driven by an increase of approximately 4% in the average reference price and lower quality discounts, resulting from renegotiated commercial terms with ENAP, the crude buyer.

Oil revenues represented 80% of total net revenues in Chile in 1Q2014 compared to 87% in 1Q2013.

Gas revenues increased by 57% to $9.5 million in 1Q2014, mainly due to an increase of 48% in the average realized gas price resulting from higher world methanol prices and an improved agreement with the Company's gas purchaser, Methanex. Gas revenues represented 20% of total net revenues in Chile in 1Q2014 compared to 13% in 1Q2013.

Costs: Production costs in Chile in 1Q2014 increased by 8% to $19.5 million, resulting in a 29% increase in production cost per boe to $30.8. This was mostly due to higher depreciation charges per boe, the impact on fixed costs from lower production, and, to a lesser extent, higher costs resulting from the operation of electrical submersible pumps and chemical treatments to improve oil quality.

Exploration expenses in Chile remained relatively stable and amounted to $5.5 million in 1Q2014 compared to $5.3 million in 1Q2013. Exploration expenses in 1Q2014 included the write-off of one well in the Fell Block drilled in 4Q2013 compared to the write-off of two wells in 1Q2013, one in Fell Block and one in Tranquilo Block.

Administrative costs in Chile in 1Q2014 decreased to $4.0 million from $4.6 million in 1Q2013. Selling expenses in Chile decreased from $1.2 million in 1Q2013 to $0.7 million in 1Q2014.

Operating costs increased by 2% to $7.8 million in 1Q2014 from $7.9 million in 1Q2013.

Adjusted EBITDA: Adjusted EBITDA in Chile increased by 5% to $30.7 million in 1Q2014, compared to $29.2 million in 1Q2013, mainly driven by revenue growth and lower administrative and selling expenses, which were partially offset by higher operating costs.

Adjusted EBITDA per boe increased by 26% to $48.5 per boe in 1Q2014 compared to $38.4 per boe in 1Q2013, as a result of higher average realized sales prices, which were partially offset by higher operating costs per boe.

Operational Performance:

During the first quarter of 2014, the Company advanced its exploration and development work program with the drilling of the Konawentru Oeste 1, Loij 1 and Konawentru 12 wells in the Fell Block (GeoPark operated with a 100% WI), and the drilling of the Tenca 1 well in the Flamenco Block (GeoPark operated with a 50% WI). Furthermore, an additional 350 sqkm of new 3D seismic were acquired on the Isla Norte Block (GeoPark operated with a 60% WI) to complete a total of 1,541 sqkm on the Tierra del Fuego blocks and fully completing the 3D seismic commitment.

Further details are provided in the recent Operations Update release of May 13, 2014.

Operations in Colombia

In Colombia, following the acquisitions of three companies (Winchester, Luna and Cuerva) in early 2012, GeoPark has working interests in 10 hydrocarbon blocks with 2P PRMS reserves of 16.5 mmboe, certified by D&M as of December 31, 2013. Average production for 1Q2014 reached 9,265 boepd.

Key Indicators | 1Q2014 | 1Q2013 | % Chg. | |

Oil production (bopd) | 9,232 | 4,932 | 88% | |

Gas production (mcfpd) | 196 | 34 | 476% | |

Average net production (boepd) | 9,265 | 4,938 | 88% | |

Net Revenues ($ million) | 37.2 | 43.8 | -15% | |

Adjusted EBITDA ($ million) | 20.7 | 22.0 | -6% | |

Adjusted EBITDA per boe ($) | 41.2 | 49.6 | -17% |

Production: Colombian oil production increased by 88% to 9,232 bopd in 1Q2014, resulting from successful exploration and development efforts, most notably the new discoveries in the Tigana 1 and Tigana Sur 1 wells in 4Q2013 and the development and appraisal of the Max, Tua and Tarotaro fields in the Llanos 34 Block.

Net Revenues: The Colombian operations represented 44% of the total consolidated net revenues compared to 49% of the total consolidated net revenues in 1Q2013. The significant increase in GeoPark's Colombian oil production of 88% in 1Q2014 was not entirely reflected in net revenues, due to the delay in deliveries. Net revenues, which decreased by 15% to $37.2 million in 1Q2014, were also negatively impacted by a decrease in the average realized price per barrel of crude oil and an increase in earn-out expenses.

The average realized price decreased by 20% to $82 per barrel in 1Q2014. During 2013, the Company started selling part of its oil production at the well-head with higher commercial discounts (and thus lower net prices), as opposed to transporting it to different delivery points. This led to lower selling expenses that partially offset the lower selling prices and had no impact in the overall Adjusted EBITDA.

Earn-out expenses increased to $3.7 million in 1Q2014 compared to $1.4 million in 1Q2013 due to higher production, mainly in the Llanos 34 Block, as provided for in the Winchester stock purchase agreement.

Costs: Production costs in Colombia decreased by 13% to $18.0 million in 1Q2014, primarily due to improved fixed cost absorption that led to a decrease in the production cost per barrel of 23% to $35.9 per barrel.

Exploration expenses in Colombia amounted to $0.4 million in 1Q2014 compared to $1.4 million in 1Q2013, mainly due to the write-off of one well in 1Q2013. There were no write-offs in 1Q2014.

Administrative costs in Colombia in 1Q2014 increased to $2.6 million compared to $2.4 million in 1Q2013.

Selling expenses in Colombia in 1Q2014 decreased by 16% to $5.5 million compared to $6.6 million in 1Q2013, as explained above.

Operating costs for the quarter decreased by 22% to $8.3 million compared to $10.8 million in 1Q2013.

Adjusted EBITDA: Adjusted EBITDA in Colombia decreased by 6% to $20.7 million in 1Q2014 compared to $22.0 million in 1Q2013, mainly as a result of the delayed oil deliveries.

Adjusted EBITDA per boe decreased by 17% to $41.2 per boe in 1Q2014, mainly due to lower average price and higher earn-out payments, which were partially offset by lower production costs per boe from increased efficiency.

Operational Performance:

During the 1Q2014, in the Llanos 34 Block, the Aruco 1 well was successfully drilled and tested and put in production, while the Tigana Norte 1 well was drilled and will be tested in 2Q2014 (GeoPark operated with a 45% WI). GeoPark continues to advance and is on track with its 2014 work program.

Further details are provided in the recent Operations Update release of May 13, 2014.

Operations in Brazil

During 1Q2014, GeoPark signed service contracts to acquire 3D seismic in the Blocks awarded in Round 11 in the Reconcavo and Potiguar basins. Seismic registration of those blocks is expected to start in 3Q2014.

On March 28, 2014, GeoPark announced the approval by the ANP in relation to the acquisition of a 10% interest in the Manati Field in Brazil. The agreed purchase price was $140 million, which was adjusted by the net cash proceeds from all production, attributable to Rio das Contas since May 1, 2013, to $115.2 million net of cash acquired. The transaction closed on March 31, 2014 and GeoPark will begin consolidating results in its financial statements as of 2Q2014.

Operations in Argentina

Operations in Argentina represented less than 1% of consolidated net revenues and Adjusted EBITDA in 1Q2014 and 1Q2013.

In March 2014, GeoPark informed the Mendoza Province Secretary of Infrastructure and Energy of its decision to relinquish 100% of the Cerro Dona Juana and Loma Cortaderal Blocks to the Mendoza Province, which cover an area of 47.9 thousand acres. Neither the Cerro Dona Juana nor the Loma Cortaderal Blocks are currently in production or have any associated reserves.

CONSOLIDATED NON-OPERATING RESULTS AND PROFIT FOR THE PERIOD

Net Financial Expenses: Net financial expenses decreased to $7.6 million in 1Q2014 from $12.6 million in 1Q2013, due to one-time expenses incurred as part of the prepayment of the 2015 Reg S Bond in February 2013, which were partially offset by higher interest expenses due to higher average indebtedness as a result of the 2020 Bond amounting to $300 million issued in 1Q2013, and which allowed the Company to reduce its average cost of funding and extend maturities.

Income Tax: Income tax amounted to $5.5 million in 1Q2014 compared to $4.4 million in 1Q2013, in line with the increase in profits before income taxes in 1Q2014.

Profit: Profit for the period increased 9% and amounted to $10.3 million in 1Q2014 compared to $9.4 million in 1Q2013, mainly due to lower net financial expenses, which were partially compensated by the decrease in operating results.

BALANCE SHEET

Cash and cash equivalents as of March 31, 2014, totaled $131.9 million, while at year-end 2013 cash and cash equivalents amounted to $121.1 million. The increase is primarily due to cash generation from operations during the period of $37.5 million, along with $132.6 million of funds generated from financing activities, and are explained by (i) $70 million credit facility to acquire an interest in the Manati gas field and (ii) $90.9 million net proceeds resulting from the NYSE IPO, which were partially offset by $28 million related to debt and interest payments. In addition, $159.3 million of net cash was used for the Company's investment activities, including the Company's capital expenditures program as well as the acquisition of an interest in the Manati gas field.

Total assets as of March 31, 2014, amounted to $1,046.0 million. Additionally, total investments for the period included (i) $45.8 million invested in Chile, where the Company drilled nine wells and acquired 350 sqkm of 3D seismic surveys and (ii) $28.9 million invested in Colombia that included the drilling of six wells. In addition, investing activities in 1Q2014 included $115.2 million related to the acquisition of an interest in the Manati gas field (net of cash acquired) that was completed on March 31, 2014.

At the end of 1Q2014, GeoPark's total financial debt amounted to $364.7 million, which included $294.5 million related to the 2020 Bond issued in February 2013 and $70.0 million related to a 5-year credit facility for the acquisition of an interest in the Manati Field.

Shareholders' Equity reached $470.6 million and included minority interests of $98.7 million related to LG International's participation in the Chilean and Colombian operations (LG International and GeoPark have a strategic alliance to build a portfolio of upstream assets across Latin America.) Shareholders' Equity as of March 31, 2014 also includes net proceeds of $90.9 million resulting from the NYSE IPO.

FINANCIAL RATIOS (*)

Amounts in $ million | ||||||

Year / Period | Financial debt | Cash position | Gross debt / | Interest coverage | ||

1Q2013 | 299.4 | 176.0 | 2.2x | 5.3x | ||

2Q2013 | 301.8 | 149.4 | 2.2x | 4.4x | ||

3Q2013 | 296.2 | 104.8 | 2.2x | 5.9x | ||

2013 | 317.1 | 121.1 | 1.9x | 4.3x | ||

1Q2014(**) | 364.7 | 131.9 | 2.2x | 4.9x | ||

(*) Based on trailing 12 month financial results for 1Q2013, 2Q2013, 3Q2013 and 1Q2014

(**) Does not consider Adjusted EBITDA generated by the acquired interest in the Manati Field in Brazil

GeoPark's consolidated incurrence financial covenants agreed to under the 2020 Bond indenture provide for:

- Leverage Ratio, defined as gross debt to Adjusted EBITDA, lower than 2.75x for the year 2014 and lower than 2.5x from 2015 onwards;

- Interest Coverage Ratio, defined as Adjusted EBITDA divided by Interest Expenses, above 3.5x.

OTHER NEWS/RECENT EVENTS

Initial Public Offering and NYSE Listing

The Company began trading on the NYSE under the ticker symbol GPRK on February 7, 2014. In its move to the NYSE, GeoPark issued 13,999,700 shares at a price of $7.00 per share, including the over-allotment option granted to and exercised by the underwriters and resulting in 57,863,615 shares outstanding as of March 31, 2014. Gross proceeds from the offering totaled approximately $100 million, which will primarily be used to support the Company's expansion. Through its NYSE listing, the Company intends to reach a wider investor audience and strengthen liquidity for all its shareholders.

Brazil Round 12 Bidding Process

Parnaiba Basin: In December, 2013, the Brazilian Federal Court issued an injunction, preventing the ANP from advancing with the bidding process of Block PN-T-597 in the Parnaiba Basin (Round 12), until studies are carried out by ANP regarding the possible environmental impact of drilling unconventional resources. On April 16, 2014, the ANP suspended proceedings related to the award of Block PN-T-597 to GeoPark.

Sergipe Alagoas Basin: In May 2014, GeoPark obtained final approval and signed the concession contract with the ANP for the Exploratory Block SEAL-T-268, located in the Sergipe Alagoas Basin in Brazil (Round 12)

GeoPark can be visited online at www.geo-park.com

For further information please contact: | |

Pablo Ducci – Director Capital Markets | |

Sofia Chellew – Investor Relations | |

Santiago, Chile | |

T: +562-2242-9600 |

CONSOLIDATED STATEMENT OF INCOME

(Unaudited)

In millions of $, except for % | |||

1Q2014* | 1Q2013 | % | |

NET REVENUES | |||

Sale of crude oil | 75.2 | 83.7 | -10% |

Sale of gas | 9.5 | 6.1 | 57% |

TOTAL NET REVENUES | 84.7 | 89.8 | -6% |

Production costs | -37.7 | -38.3 | -2% |

GROSS PROFIT | 47.1 | 51.5 | -9% |

Exploration costs | -6.8 | -7.3 | -7% |

Administrative costs | -11.1 | -9.6 | 16% |

Selling expenses | -6.3 | -7.9 | -20% |

Other operating income | 0.6 | -0.2 | -497% |

OPERATING PROFIT | 23.4 | 26.5 | -12% |

Financial results, net | -7.6 | -12.6 | -40% |

PROFIT BEFORE INCOME TAX | 15.8 | 13.9 | 14% |

Income tax | -5.5 | -4.4 | 24% |

PROFIT FOR THE PERIOD | 10.3 | 9.4 | 9% |

Non‑controlling interest | 3.6 | 3.0 | 22% |

ATTRIBUTABLE TO OWNERS | 6.7 | 6.5 | 3% |

RECONCILIATION OF ADJUSTED EBITDA TO PROFIT BEFORE INCOME TAX AND ADJUSTED EBITDA PER BOE

In millions of $, except for % | |||

1Q2014 | 1Q2013 | % | |

Adjusted EBITDA | 48.4 | 49.7 | -3% |

Depreciation | -18.1 | -15.8 | 15% |

Accrual of Stock Awards | -3.0 | -1.8 | 64% |

Impairment and write-off | -4.1 | -5.9 | -31% |

Others | 0.2 | 0.3 | -41% |

OPERATING PROFIT | 23.4 | 26.5 | -12% |

Financial results, net | -7.6 | -12.6 | -40% |

PROFIT BEFORE INCOME TAX | 15.8 | 13.9 | 14% |

Adjusted EBITDA | 48.4 | 49.7 | -3% |

Total Boe (in millions of boe) | 1.14 | 1.21 | -5% |

Adjusted EBITDA per boe | 42.4 | 41.1 | 3% |

* The significant increase in GeoPark's Colombian oil production of 88% in 1Q2014 was not entirely reflected in net revenues or Adjusted EBITDA for the period, mainly due to some delayed oil deliveries and increased oil inventory. During the first quarter of 2014, Ecopetrol (who buys and exports a significant portion of the Company's oil), allocated larger volumes of its own oil production to exports because of an oil refinery shut down, temporarily affecting the volumes received from GeoPark and other Colombian oil producers. This situation was normalized during May 2014, and is not expected to generate any impact on the Company's 2014 results.

SELECTED HISTORICAL OPERATIONAL AND FINANCIAL DATA

Year ended December 31, | |||||

2013 | 2012 | 2011 | 2010 | 2009 | |

Oil Reserves (2P PRMS) - mmboe | 33.9 | 27.8 | 16.9 | 16.2 | 10.9 |

Gas Reserves (2P PRMS) - mmboe | 27.7 | 29.1 | 32.6 | 33.4 | 31.3 |

Combined Reserves (2P PRMS) - mmboe | 61.6 | 56.9 | 49.5 | 49.6 | 42.2 |

Oil Production (thousand boepd) | 11.1 | 7.5 | 2.5 | 1.9 | 1.2 |

Gas Production (thousand boepd) | 2.4 | 3.8 | 5.1 | 5.0 | 5.1 |

Production (thousand boepd) | 13.5 | 11.3 | 7.6 | 6.9 | 6.3 |

Oil Revenues ($ million ) | 315 | 222 | 74 | 48 | 22 |

Gas Revenues ($ million) | 23 | 29 | 38 | 31 | 23 |

Total Revenues ($ million) | 338 | 250 | 112 | 80 | 45 |

Adjusted EBITDA ($ million) | 167 | 121 | 63 | 41 | 18 |

GLOSSARY

Adjusted EBITDA | Profit for the period before net finance cost, income tax, depreciation, amortization, certain non-cash items such as impairments and write offs of unsuccessful efforts, accrual of stock options and stock awards and bargain purchase gain on acquisitions of subsidiaries |

Adjusted EBITDA per boe | Adjusted EBITDA divided by total boe production for the applicable period |

ANP | Agencia Nacional do Petroleo, Brazil's National Agency of Petroleum |

boe | Barrels of oil equivalent |

boepd | Barrels of oil equivalent per day |

bopd | Barrels of oil per day |

CEOP | Contrato Especial de Operacion Petrolera (Special Petroleum Operations Contract) |

EPS | Earnings per share |

IPO | Initial Public Offering |

mbbl | Thousand barrels of oil |

mmboe | Million barrels of oil equivalent |

mcfpd | Thousand cubic feet per day |

mmcfpd | Million cubic feet per day |

Mm3/day | Thousand cubic meters per day |

PRMS | Petroleum Resources Management System |

SPE | Society of Petroleum Engineers |

WI | Working interest |

NPV10 | Present value of estimated future oil and gas revenues, net of estimated direct expenses, discounted at an annual rate of 10% |

Sqkm | Square kilometers |

NOTICE

Additional information about GeoPark can be found in the "Investor Support" section on the Web site at www.geo-park.com

Rounding amounts and percentages: Certain amounts and percentages included in this press release have been rounded for ease of presentation. Percentage figures included in this press release have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, certain percentage amounts in this press release may vary from those obtained by performing the same calculations using the figures in the financial statements. In addition, certain other amounts that appear in this press release may not sum due to rounding.

CAUTIONARY STATEMENTS RELEVANT TO FORWARD-LOOKING INFORMATION

This press release contains statements that constitute forward-looking statements. Many of the forward looking statements contained in this press release can be identified by the use of forward-looking words such as ''anticipate,'' ''believe,'' ''could,'' ''expect,'' ''should,'' ''plan,'' ''intend,'' ''will,'' ''estimate'' and ''potential,'' among others.

Forward-looking statements appear in a number of places in this press release and include, but are not limited to, statements regarding the intent, belief or current expectations, regarding various matters, including expected 2014 production growth and capital expenditures plan. Forward-looking statements are based on management's beliefs and assumptions and on information currently available to the management. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the forward-looking statements due to various factors.

Forward-looking statements speak only as of the date they are made, and the Company does not undertake any obligation to update them in light of new information or future developments or to release publicly any revisions to these statements in order to reflect later events or circumstances or to reflect the occurrence of unanticipated events. For a discussion the risks facing the Company which could affect whether these forward-looking are realized, see filings with the U.S. Securities and Exchange Commission.

Information about oil and gas reserves: The SEC permits oil and gas companies, in their filings with the SEC, to disclose only proved, probable and possible reserves that meet the SEC's definitions for such terms. GeoPark uses certain terms in this press release, such as "PRMS Reserves" that the SEC's guidelines do not permit GeoPark from including in filings with the SEC. As a result, the information in the Company's SEC filings with respect to reserves will differ significantly from the information in this press release. NPV10 for PRMS 1P, 2P and 3P reserves is not a substitute for the standardized measure of discounted future net cash flows for SEC proved reserves.

Adjusted EBITDA: The Company defines Adjusted EBITDA as profit for the period before net finance cost, income tax, depreciation, amortization and certain non-cash items such as impairments and write-offs of unsuccessful exploration and evaluation assets, accrual of stock options and stock awards and bargain purchase gain on acquisition of subsidiaries. Adjusted EBITDA is not a measure of profit or cash flows as determined by IFRS. The Company believes Adjusted EBITDA is useful because it allows us to more effectively evaluate our operating performance and compare the results of our operations from period to period without regard to our financing methods or capital structure. The Company excludes the items listed above from profit for the period in arriving at Adjusted EBITDA because these amounts can vary substantially from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. Adjusted EBITDA should not be considered as an alternative to, or more meaningful than, profit for the period or cash flows from operating activities as determined in accordance with IFRS or as an indicator of our operating performance or liquidity. Certain items excluded from Adjusted EBITDA are significant components in understanding and assessing a company's financial performance, such as a company's cost of capital and tax structure and significant and/or recurring write-offs, as well as the historic costs of depreciable assets, none of which are components of Adjusted EBITDA. The Company's computation of Adjusted EBITDA may not be comparable to other similarly titled measures of other companies. For a reconciliation of Adjusted EBITDA to the IFRS financial measure of profit for the year, see the accompanying financial tables.

Photo - http://photos.prnewswire.com/prnh/20140522/90315

Logo - http://photos.prnewswire.com/prnh/20130603/MX24008LOGO-b

SOURCE GeoPark Limited