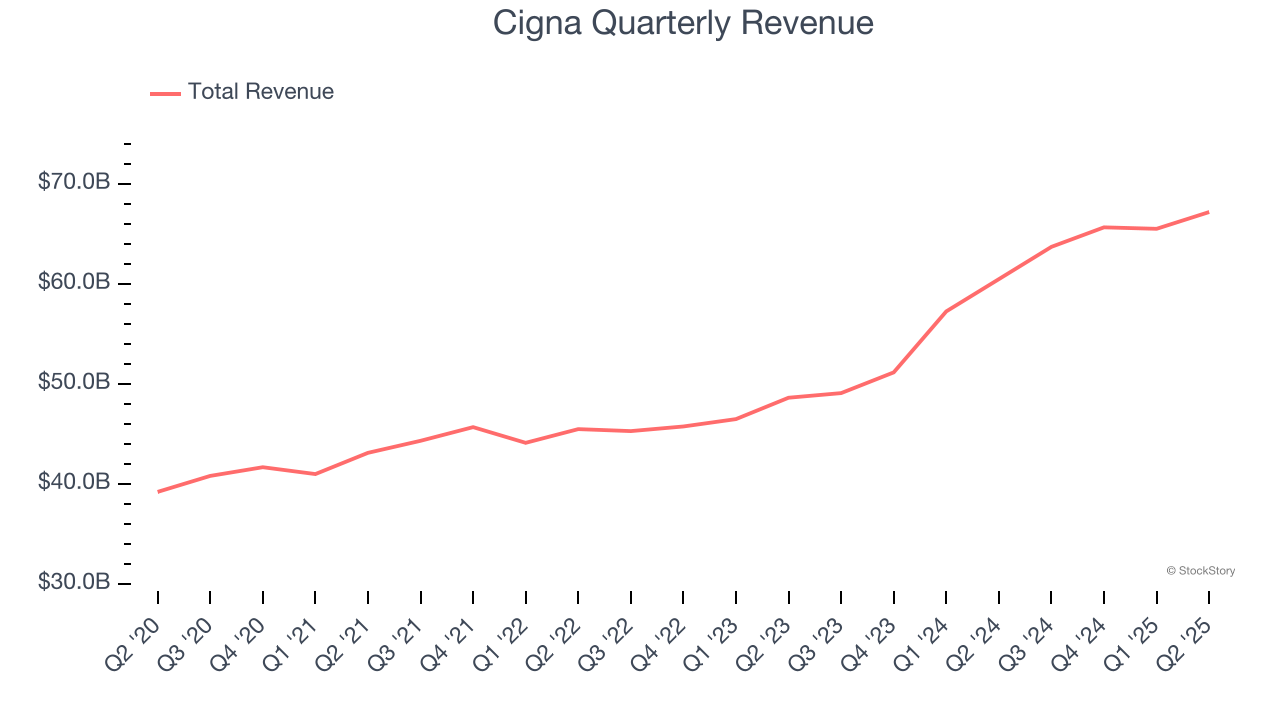

Health insurance company Cigna (NYSE: CI) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 11.1% year on year to $67.18 billion. Its non-GAAP profit of $7.20 per share was 0.6% above analysts’ consensus estimates.

Is now the time to buy Cigna? Find out by accessing our full research report, it’s free.

Cigna (CI) Q2 CY2025 Highlights:

- Revenue: $67.18 billion vs analyst estimates of $62.21 billion (11.1% year-on-year growth, 8% beat)

- Adjusted EPS: $7.20 vs analyst estimates of $7.15 (0.6% beat)

- Full-year guidance: maintained adjusted EPS guidance of at least $29.60 per share

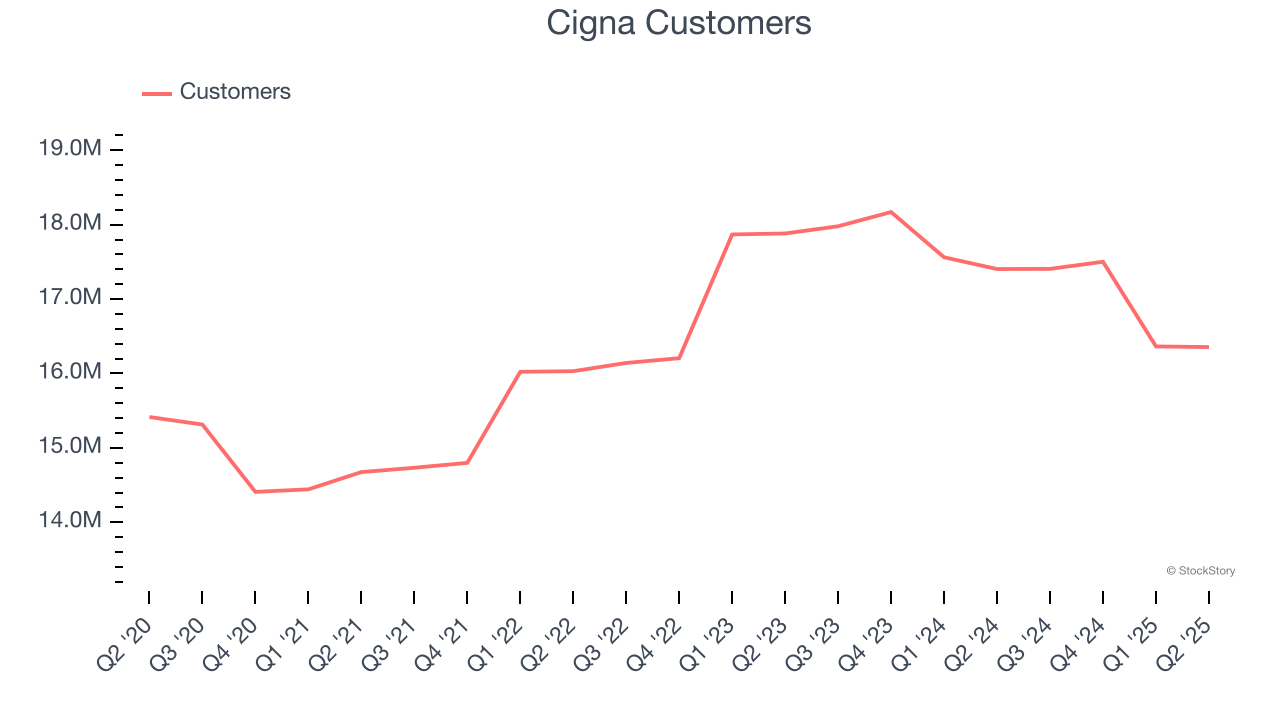

- Customers: 16.36 million, down from 16.36 million in the previous quarter

- Market Capitalization: $79.57 billion

Company Overview

With roots dating back to 1792 and serving millions of customers across the globe, The Cigna Group (NYSE: CI) provides healthcare services through its Evernorth Health Services and Cigna Healthcare segments, offering pharmacy benefits, specialty care, and medical plans.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Cigna grew its sales at a decent 11.8% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

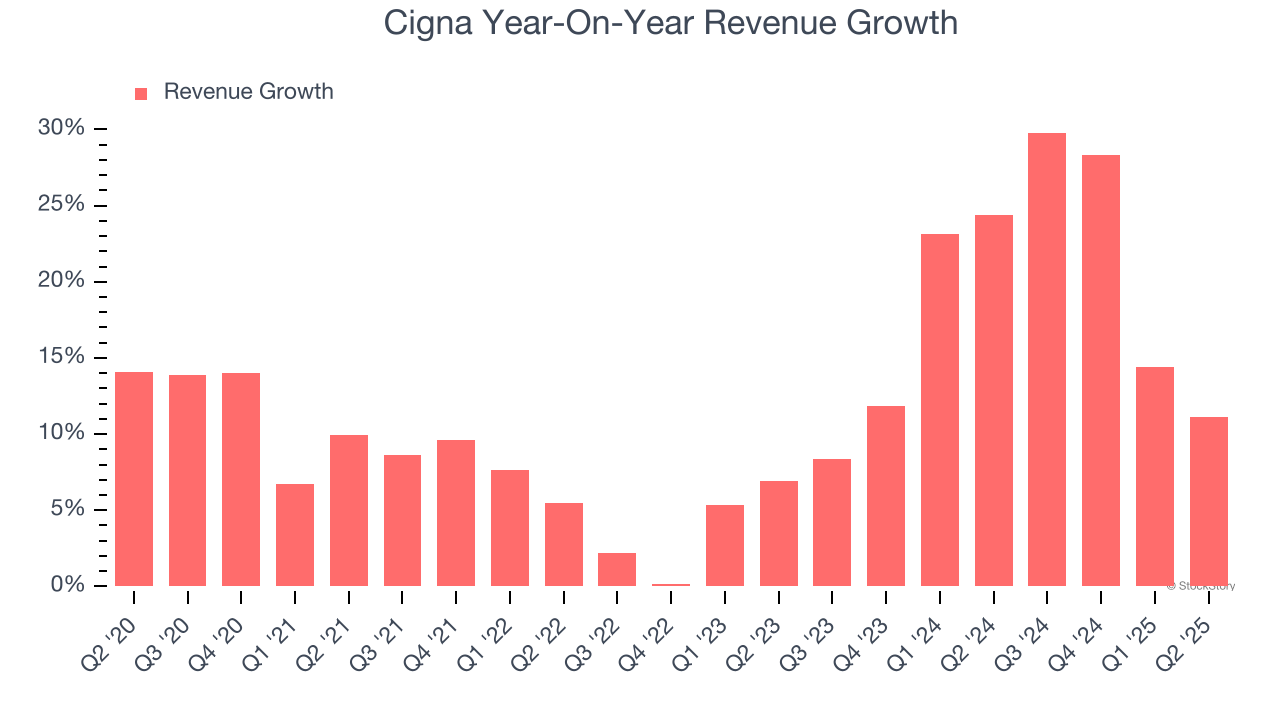

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Cigna’s annualized revenue growth of 18.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

Cigna also reports its number of customers, which reached 16.36 million in the latest quarter. Over the last two years, Cigna neither added nor lost customers. Because this number is lower than its revenue growth, we can see the average customer spent more money each year on the company’s products and services.

This quarter, Cigna reported year-on-year revenue growth of 11.1%, and its $67.18 billion of revenue exceeded Wall Street’s estimates by 8%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

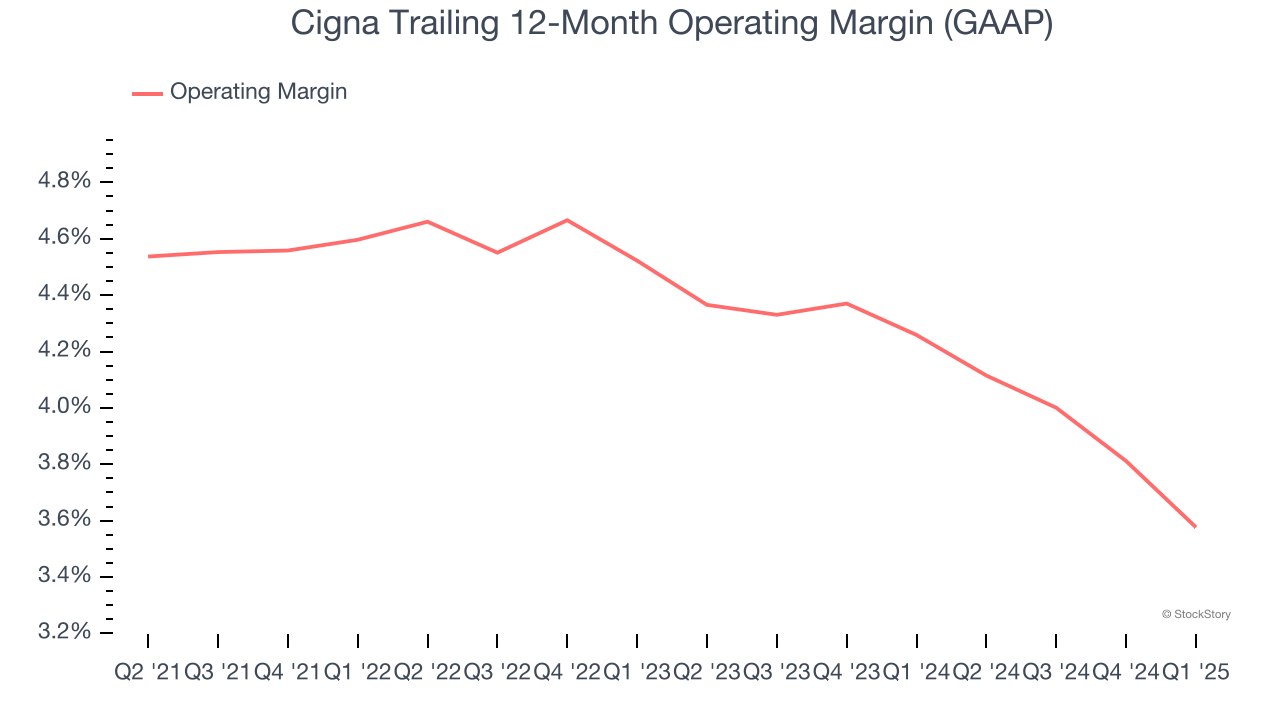

Operating Margin

Cigna’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 4.2% over the last five years. This profitability was paltry for a healthcare business and caused by its suboptimal cost structure.

Looking at the trend in its profitability, Cigna’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

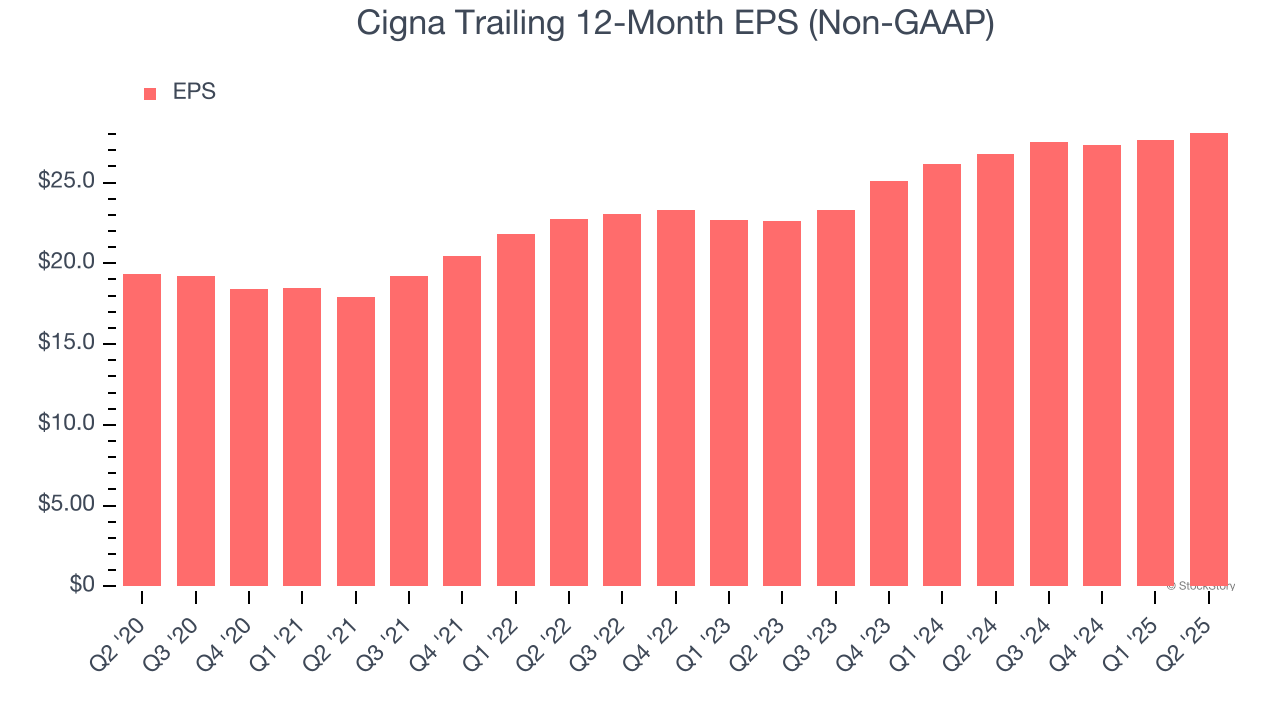

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Cigna’s EPS grew at a solid 7.7% compounded annual growth rate over the last five years. However, this performance was lower than its 11.8% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q2, Cigna reported adjusted EPS at $7.20, up from $6.72 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Cigna’s full-year EPS of $28.09 to grow 13.3%.

Key Takeaways from Cigna’s Q2 Results

We were impressed by how significantly Cigna blew past analysts’ revenue expectations this quarter. Looking ahead, the company maintained full-year EPS guidance, showing the business is on track. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 2.8% to $306.30 immediately following the results.

Cigna may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.