Valued at a market cap of $9.8 billion, Norwegian Cruise Line Holdings Ltd. (NCLH) is a leading global cruise company that operates three award-winning brands, Norwegian Cruise Line, Oceania Cruises, and Regent Seven Seas Cruises, together ranking among the world’s largest cruise operators. Headquartered in Miami, Florida, the company offers a broad portfolio of cruise experiences spanning contemporary, premium, and luxury segments, with itineraries to more than 700 destinations worldwide.

Companies valued between $2 billion and $10 billion are typically classified as “mid-cap stocks,” and NCLH fits the label perfectly. NCLH’s fleet and capacity continue to expand with new vessels on order through 2036, supporting long-term growth. The company’s performance reflects resilient consumer demand and a gradual return to profitability following pandemic disruptions.

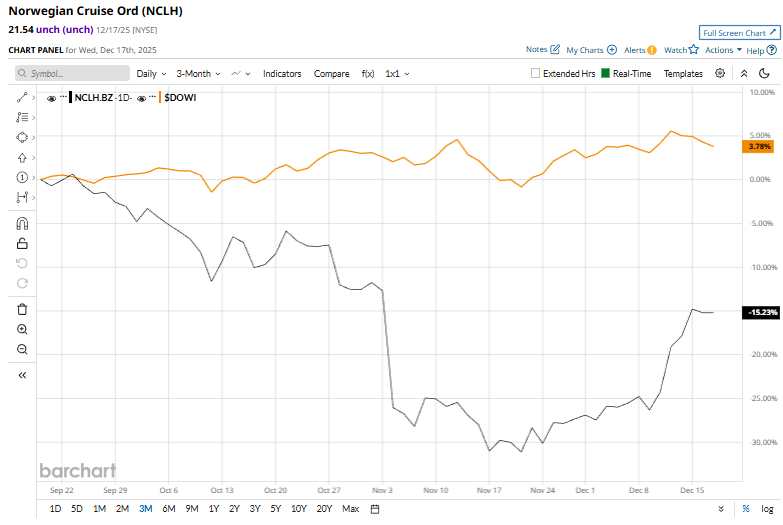

However, this cruise titan is currently trading 26.5% below its 52-week high of $29.29, reached on Jan. 31. Shares of Norwegian Cruise Line have declined 15.1% over the past three months, considerably underperforming the Dow Jones Industrial Average’s ($DOWI) 4.1% rise during the same time frame.

In the longer term, NCLH has dropped 18.4% over the past 52 weeks, trailing DOWI’s 10.2% uptick over the same time period. Moreover, on a YTD basis, shares of NCLH are down 16.3%, compared to XLF’s 12.6% rise.

NCLH has recently climbed above its 50-day and 200-day moving averages, indicating an uptrend.

On Dec. 11, Norwegian Cruise Line shares rose 4.9% following the announcement that travel industry veteran Marc Kazlauskas will become President effective Jan. 19, 2026. With over 30 years of leadership experience, including his recent role as CEO of Avoya Travel, Kazlauskas succeeds David Herrera. The market reacted positively, reflecting investor confidence in his ability to enhance commercial performance and customer experience in line with the cruise line’s strategic goals.

NCLH has considerably underperformed its rival, Carnival Corporation & plc (CCL), which rallied 9% over the past 52 weeks and 12.5% on a YTD basis.

The stock has a consensus rating of "Moderate Buy” from the 23 analysts covering it, and the mean price target of $27.18 suggests a 26.2% premium to its current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart