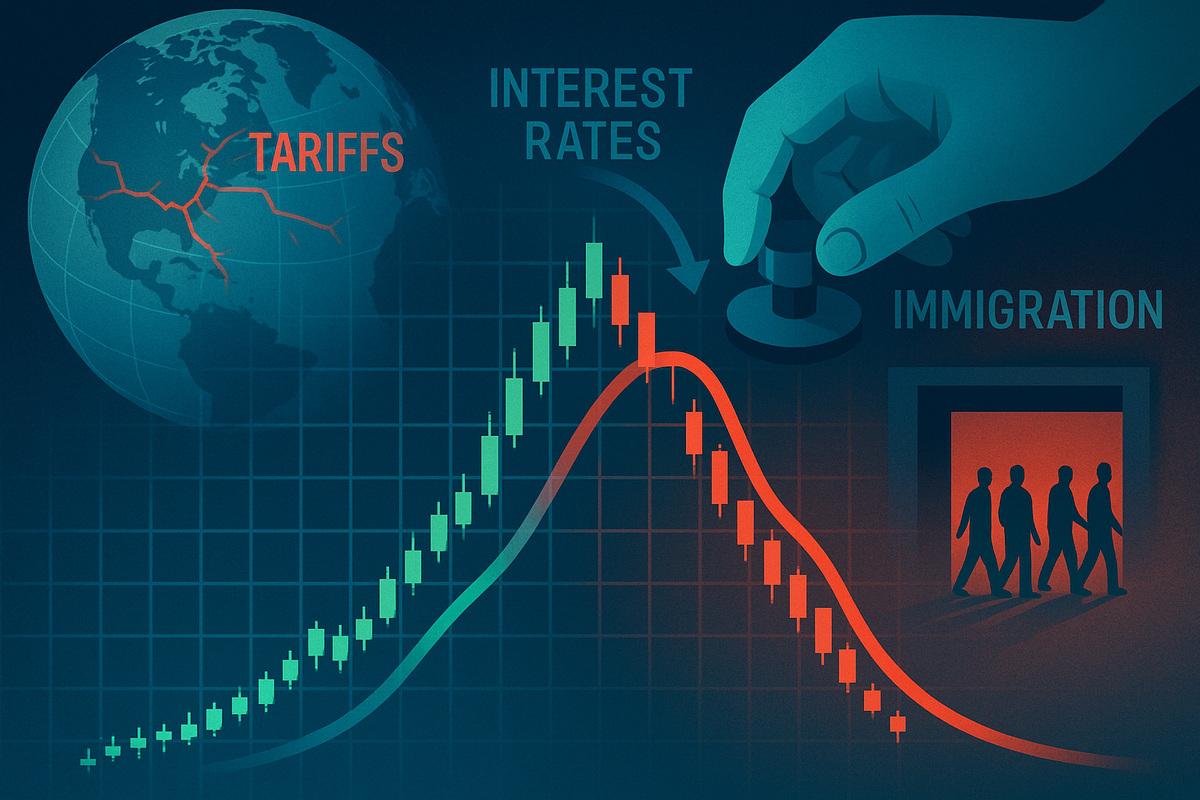

Global financial markets are treading a cautious path today, September 23, 2025, as a complex interplay of macroeconomic forces dictates investor sentiment. While the Organisation for Economic Co-operation and Development (OECD) offered a glimmer of short-term optimism by revising its global and U.S. growth forecasts upwards for 2025, this relief is overshadowed by stark warnings of a significant deceleration in 2026. This anticipated slowdown is primarily attributed to the full impact of escalating tariffs and a projected decline in immigration, creating a volatile backdrop against recent Federal Reserve interest rate cuts designed to stimulate the economy.

The market's immediate reaction reflects a push and pull between these conflicting signals. Investors are grappling with the dual reality of current resilience driven by AI investment and pre-tariff "front-loading," while simultaneously preparing for a tougher economic environment next year. This delicate balance is leading to sector-specific divergences, rewarding companies poised to benefit from lower borrowing costs and technological advancements, yet punishing those vulnerable to disrupted trade and rising input prices.

What Happened and Why It Matters

Today, the OECD delivered a mixed economic outlook, raising its global economic growth forecast for 2025 to 3.2% from a previous 2.9%, and upgrading the U.S. GDP growth forecast for 2025 from 1.6% to 1.8%. This unexpected resilience was credited to robust investment in artificial intelligence (AI) and a strategic "front-loading" of industrial production and trade by companies anticipating future tariff hikes. However, the optimism was notably tempered by the OECD's projection of a slowdown in U.S. GDP growth to 1.5% in 2026, down from 2.8% in 2024. The primary culprits cited for this deceleration are the full impact of higher tariffs and a projected drop in net immigration.

This revision comes on the heels of the Federal Reserve's recent decision in September 2025 to cut interest rates by 25 basis points, bringing the federal-funds rate to a range of 4.00%-4.25%, with two more cuts signaled for the remainder of the year. This dovish pivot was largely a response to a weakening labor market, aiming to stimulate economic activity by reducing borrowing costs. Simultaneously, concerns over trade protectionism have intensified, with the overall effective tariff rate in the U.S. rising to approximately 19.5% by the end of August 2025—the highest since 1933. These "reciprocal" tariffs have already triggered retaliatory measures globally, fueling fears of a full-blown trade war. Adding to the long-term economic headwinds, Goldman Sachs Research anticipates a slowdown in net immigration to the U.S. to 750,000 per year, which is expected to shave 30-40 basis points off potential U.S. GDP growth compared to recent years.

These factors create a complex scenario for policymakers and investors alike. The immediate boost from AI investment and the Fed's accommodative stance offers some near-term stability, but the looming shadow of protectionist trade policies and demographic shifts presents significant structural challenges. The high tariff rates act as a tax on imported goods, leading to higher consumer prices, reduced purchasing power, and squeezed corporate profit margins, while lower immigration can impact labor supply and overall demand. The confluence of these forces means that while the economy may show some robustness in the short term, the path ahead is fraught with potential for deceleration and increased volatility.

Macroeconomic Headwinds and Tailwinds

The current macroeconomic environment is creating a distinct bifurcation in market performance, with certain sectors and companies poised to benefit while others face significant headwinds. The Federal Reserve's rate cuts typically provide a tailwind for interest-rate-sensitive sectors. Home construction companies, such as Pultegroup (NYSE: PHM), D.R. Horton (NYSE: DHI), Lennar (NYSE: LEN), and Builders FirstSource (NYSE: BLDR), stand to gain from lower mortgage rates, making homes more affordable and stimulating demand. Similarly, financials, particularly those involved in capital markets like Goldman Sachs (NYSE: GS), could see increased activity and profitability from reduced borrowing costs and a more active investment landscape. Small-cap stocks, generally represented by the Russell 2000, also tend to perform well in an environment of lower interest rates and anticipated economic stimulus.

Furthermore, the OECD's emphasis on strong investment in artificial intelligence (AI) as a driver for 2025 growth points to continued strength in the technology sector. Companies at the forefront of AI infrastructure and development, such as Arista Networks (NYSE: ANET), ASML Holding (NASDAQ: ASML), Credo Technology Group (NASDAQ: CRDO), and cloud service providers like Amazon's (NASDAQ: AMZN) AWS, are likely to attract sustained investor interest. Their growth trajectories appear less susceptible to the immediate impacts of tariffs, given the domestic nature of much of their investment and innovation.

Conversely, industries heavily reliant on global supply chains or exposed to import costs are facing significant pressure from the escalating tariffs. Retailers will struggle with higher input costs, which they may or may not be able to pass on to consumers, potentially squeezing profit margins. Auto manufacturers, especially those importing parts or finished vehicles, including major German brands with significant U.S. market presence, are vulnerable to increased costs and retaliatory tariffs. The tech hardware and semiconductor sectors, with their intricate global supply networks, could also see disruptions and higher production expenses. Parts of the industrials sector, along with transportation and materials companies, are also likely to lag as global trade routes are disrupted and trade tensions escalate. Companies with limited pricing power that cannot effectively pass on increased tariff costs to consumers will be particularly vulnerable to reduced profitability.

In the broader market, lower Federal Reserve interest rates generally lead to falling bond yields and rising bond prices, making fixed-income investments more attractive in the short term. However, if tariffs lead to persistent inflation, this could create upward pressure on bond yields over time, partially offsetting the Fed's easing. In commodities, gold prices are likely to see support, benefiting from lower opportunity costs due to reduced interest rates and increased demand for safe-haven assets amidst economic uncertainty stemming from trade tensions. Crude oil prices might remain steady or experience volatility depending on the balance between anticipated increased demand from economic stimulus and ongoing concerns about global oversupply and geopolitical risks. Lastly, the US Dollar typically weakens following interest rate cuts, as lower yields reduce its attractiveness to foreign investors. Furthermore, universal tariffs are generally seen as negative for the US dollar, potentially contributing to its depreciation.

A New Era of Economic Nationalism and Demographic Shifts

The current economic landscape signals a significant shift towards a new era defined by economic nationalism and evolving demographic realities. The sustained rise in tariffs, reaching levels not seen since the Great Depression in 1933, underscores a global trend away from unfettered free trade. This move has profound implications for global supply chains, forcing multinational corporations to reassess their manufacturing and sourcing strategies. We could see an acceleration of "reshoring" or "friend-shoring" initiatives, where companies bring production back to their home countries or to politically aligned nations, prioritizing supply chain resilience over pure cost efficiency. This trend could reshape global trade flows and lead to a more regionalized economic system.

The ripple effects extend to competitors and partners across various industries. Companies that have diversified their manufacturing bases or invested in automation may be better positioned to weather tariff shocks, potentially gaining a competitive advantage over those with highly concentrated, tariff-exposed supply chains. For instance, manufacturers in Vietnam or Mexico, often viewed as alternative production hubs, could see increased investment and demand. Simultaneously, the threat of retaliatory tariffs creates uncertainty for export-oriented industries, prompting them to explore new markets or reconfigure their product offerings for domestic consumption.

From a regulatory and policy standpoint, the current trajectory suggests continued debates over trade policy and potential legislative action to mitigate the negative impacts of tariffs, such as targeted subsidies or tax breaks for affected industries. The anticipated slowdown in immigration also brings to the forefront discussions about labor market policies, automation, and workforce development. Governments may need to explore policies that encourage domestic labor force participation and investment in education and training to compensate for reduced immigration. Historically, periods of high tariffs have often led to reduced global trade and economic contraction, as seen in the 1930s. While the current context is different due to the presence of globalized financial markets and diverse economies, the parallels serve as a cautionary tale, emphasizing the potential for protectionist measures to stifle global growth.

Watching for Policy Shifts and Corporate Adaptations

Looking ahead, the next few months will be critical in determining the trajectory of the global economy and market sentiment. In the short term, investors will closely monitor central bank communications for further signals on interest rate policy. While the Fed has signaled more cuts, any unexpected shifts in inflation or labor market data could alter this path. The immediate impact of the OECD's 2025 growth revision will likely provide some temporary market support, but the focus will quickly shift to incoming data for 2026 to confirm or contradict the forecasted slowdown.

Companies, particularly those in vulnerable sectors, will need to accelerate strategic pivots and adaptations. This includes further diversification of supply chains, investing in automation to reduce reliance on potentially constrained labor pools, and exploring new markets to offset tariff-affected trade routes. For example, some manufacturers might explore establishing production facilities within tariff-imposing countries to bypass import duties. Market opportunities may emerge in areas less exposed to trade tensions, such as domestic services, or in sectors that benefit from government stimulus and infrastructure spending. Conversely, challenges will persist for export-heavy industries and those with thin margins facing increased input costs.

Potential scenarios range from a "soft landing" where the Fed's rate cuts successfully cushion the economy against tariff and immigration impacts, leading to a moderate slowdown in 2026, to a more severe "hard landing" if trade wars escalate and economic nationalism stifles global demand. Investors should pay close attention to the rhetoric surrounding international trade negotiations, the implementation of new tariff measures, and any shifts in immigration policy. The interplay between monetary policy, fiscal policy (especially regarding trade), and demographic trends will be key determinants of market performance and economic stability in the coming year.

A Delicate Balance for Global Growth

Today's market movements underscore a pivotal moment for the global economy, characterized by a delicate balance between immediate resilience and looming structural challenges. The OECD's revised 2025 growth forecasts, fueled by AI investment and strategic corporate maneuvers, offer a temporary reprieve. However, this optimism is profoundly tempered by the explicit warnings of a significant economic slowdown in 2026, driven by the full force of escalating tariffs and a projected decline in immigration. The Federal Reserve's accommodative monetary policy, while providing a crucial economic cushion, faces the arduous task of counteracting these formidable headwinds.

The key takeaway for investors is the increasing importance of sector-specific analysis and a vigilant eye on geopolitical developments. The era of seamless global supply chains appears to be receding, giving way to a more fragmented and protectionist trade environment. Companies that can adapt quickly, diversify their operations, and innovate in areas less susceptible to trade friction will likely emerge as winners. Conversely, those heavily reliant on traditional global trade routes and sensitive to import costs face an uphill battle.

Moving forward, investors should closely monitor the evolution of trade policies, the effectiveness of central bank interventions, and demographic shifts. The resilience of consumer spending, corporate investment in innovation, and the ability of businesses to navigate a complex regulatory and trade landscape will be critical indicators. The coming months will undoubtedly test the adaptability of global markets, requiring a strategic and informed approach to investment amidst a period of profound economic transition.

This content is intended for informational purposes only and is not financial advice