Pennsylvania-based EPAM Systems, Inc. (EPAM) is a global technology and consulting firm focused on helping organizations navigate digital and AI-driven transformation. The company works with a wide range of clients, from large multinational corporations to emerging startups, offering services that span software development, product engineering, and platform design.

With more than three decades of experience, EPAM has built capabilities across custom software and digital solutions, supporting businesses as they integrate data, automation, and AI into their operations. Its work often centers on improving efficiency, modernizing legacy systems, and enabling new digital products.

Companies with market capitalizations between $2 billion and $10 billion are typically classified as mid-cap stocks, and EPAM Systems fits squarely within that range, with a valuation of about $7.6 billion. Operating across multiple regions, the company blends global delivery with local expertise, supporting clients in long-term digital transformation initiatives.

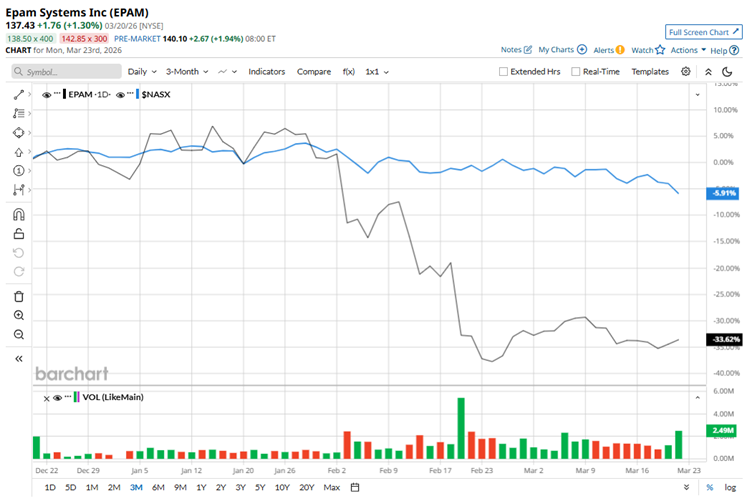

However, the company’s performance on Wall Street has been less than stellar. After hitting a 52-week peak of $222.53 in January, the stock has crashed by almost 38%. In the last three months alone, shares are down 33.6%, heavily lagging behind the broader Nasdaq Composite ($NASX), which has declined roughly 7.1% during the same stretch.

The underperformance has persisted over the longer term. Over the past year, EPAM Systems has shed nearly 21.3%, significantly trailing the Nasdaq Composite, which has advanced 22.4% during the same period. Moreover, the stock has been trading well below both its 50-day and 200-day moving averages since mid-February, signaling sustained technical weakness.

EPAM shares have come under sustained selling pressure, weighed down by the broader tech sector downturn and growing uncertainty around how AI will reshape the IT and consulting landscape. The pressure intensified following the company’s fiscal 2025 fourth-quarter results, released on Feb. 19.

While EPAM delivered better-than-expected performance on both revenue and earnings, investor focus quickly shifted to its cautious 2026 outlook. Muted growth projections and client-specific headwinds raised concerns about near-term demand, triggering a sharp 17% post-earnings selloff and reinforcing the stock’s negative momentum.

Although EPAM Systems has struggled over the past year, the pain has been even more pronounced for industry peer Gartner, Inc. (IT), whose stock has tumbled about 61.5%.

Overall, Wall Street remains cautiously optimistic on EPAM. Among the 18 analysts covering the stock, the consensus lands at a “Moderate Buy,” reflecting a balanced but positive outlook. The average price target of $194.81 suggests a potential upside of about 40% from current levels, indicating meaningful recovery potential.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Hegseth Says It ‘Takes Money to Kill Bad Guys’ Amid $200 Billion Spending Push. Why Axon and L3Harris Are the 2 Top-Rated Defense Stocks to Buy Now

- As the Market Gives Us Lemons, This Nvidia Collar Might Just Taste Like Lemonade

- The Super Micro Computer Co-Founder Faces New Chip Smuggling Charges. Does That Actually Matter for SMCI Stock?

- A Plunge in Aluminum Futures Sends Alcoa Stock Below Its 50-Day Moving Average. Should You Buy the Dip?