Over the past six months, Meta’s stock price fell to $569.25. Shareholders have lost 12.1% of their capital, which is disappointing considering the S&P 500 has climbed by 8.4%. This might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for META? Find out in our full research report, it’s free.

Why Is META a Good Business?

Famously founded by Mark Zuckerberg in his Harvard dorm, Meta Platforms (NASDAQ: META) operates a collection of the largest social networks in the world - Facebook, Instagram, WhatsApp, and Messenger, along with its metaverse focused Reality Labs.

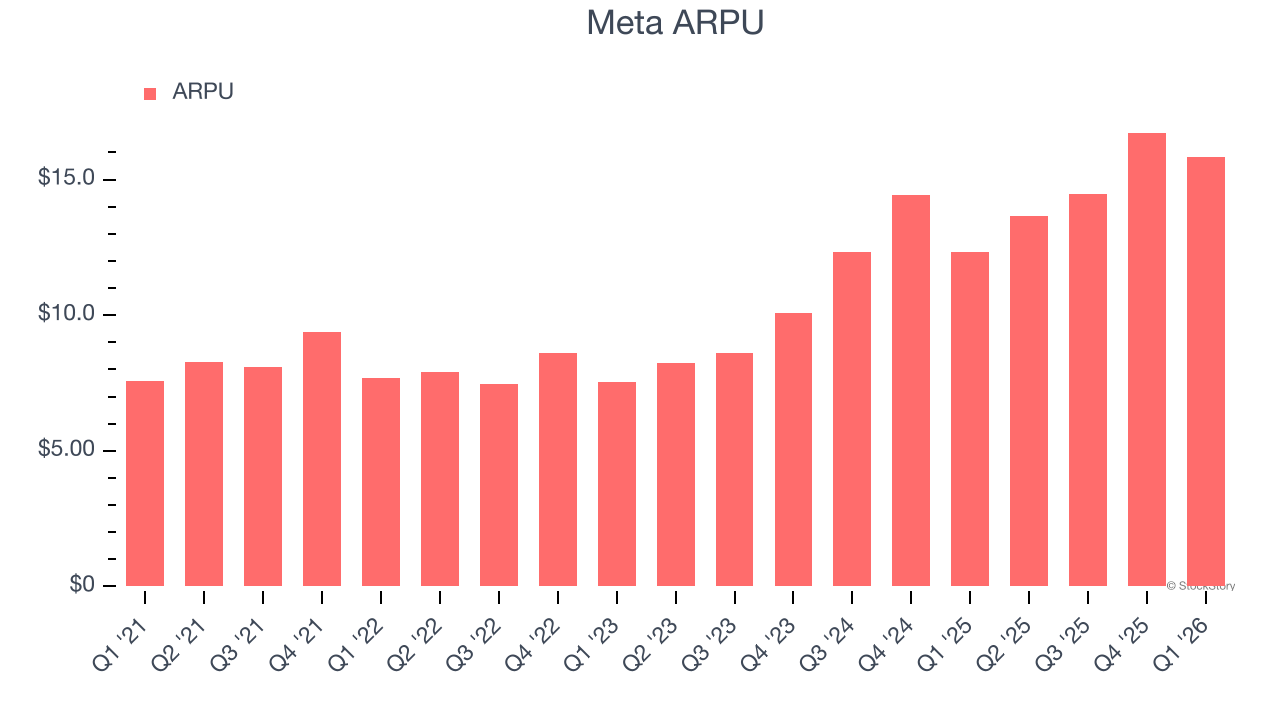

1. Eye-Popping Growth in Customer Spending

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Meta’s audience and its ad-targeting capabilities.

Meta’s ARPU growth has been exceptional over the last two years, averaging 29.6%. Although its daily active people shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing users.

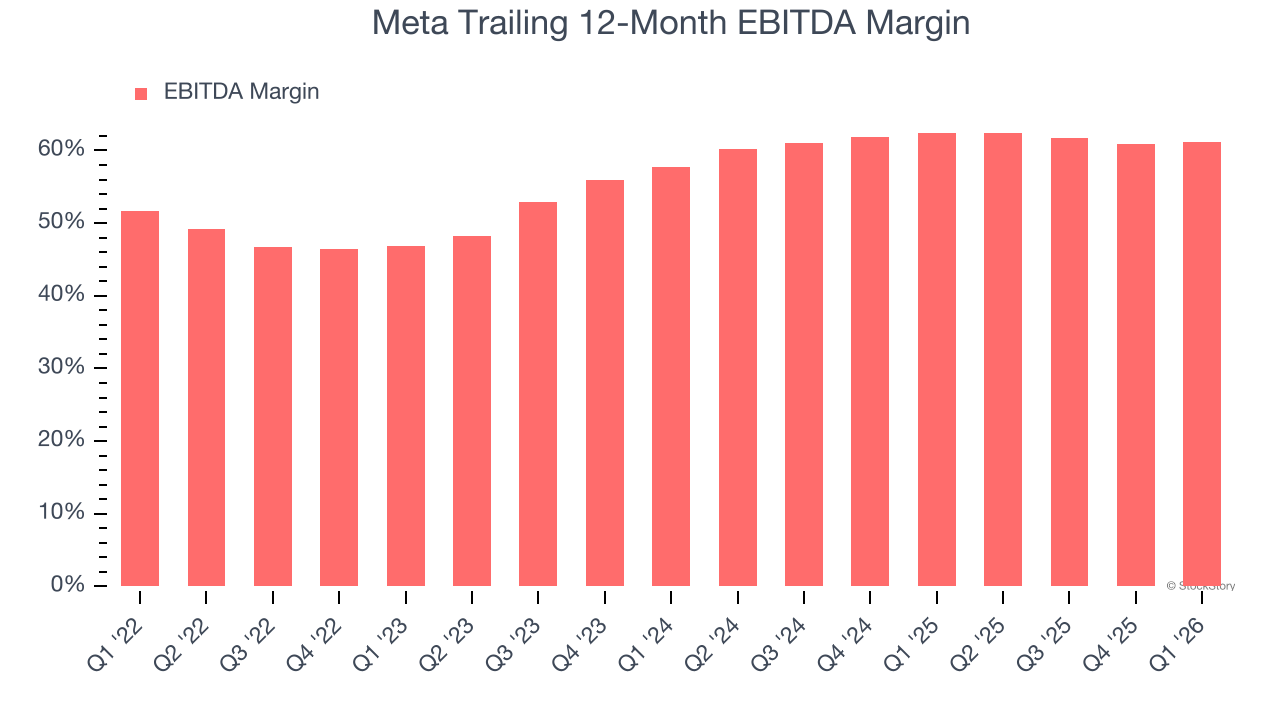

2. EBITDA Margin Reveals a Well-Run Organization

EBITDA is a good way of judging operating profitability for consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a more standardized view of the business’s profit potential.

Meta has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 61.8%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

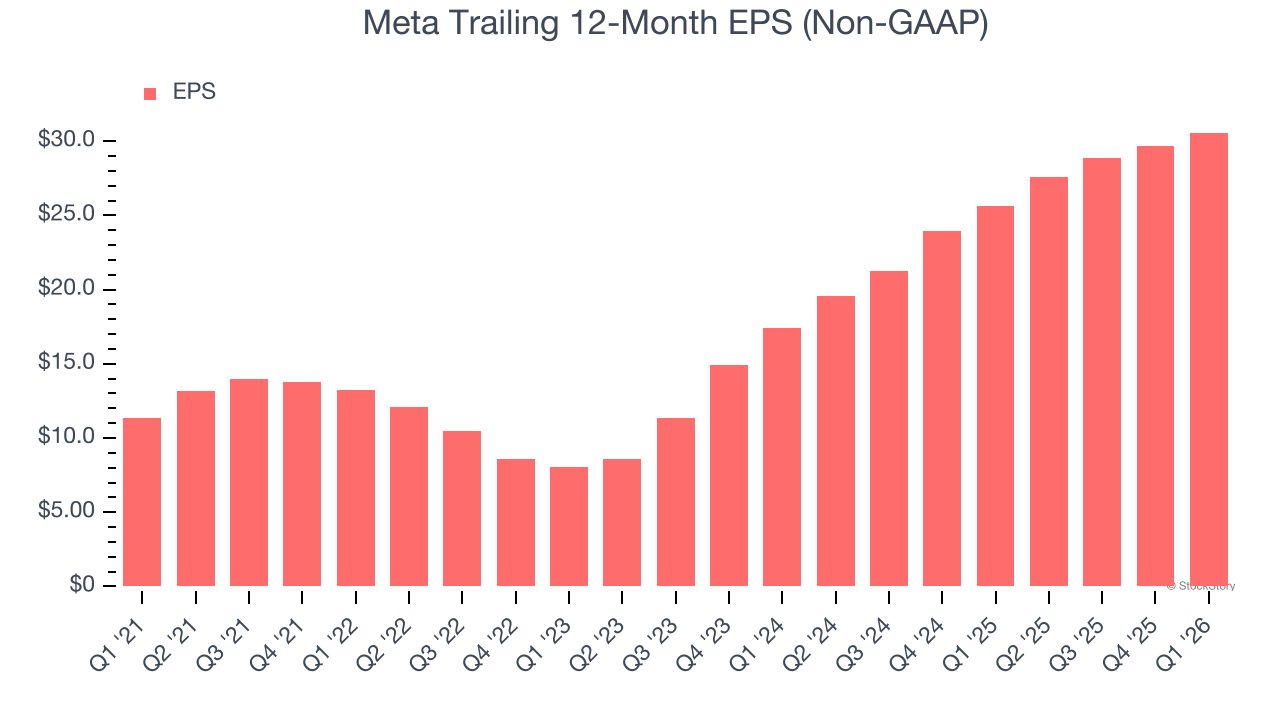

3. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Meta’s EPS grew at 56% compounded annual growth rate over the last three years, higher than its 22.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

These are just a few reasons why we think Meta is an elite consumer internet company. With the recent decline, the stock trades at 9.7× forward EV/EBITDA (or $569.25 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.