As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the outpatient & specialty care industry, including agilon health (NYSE: AGL) and its peers.

The outpatient and specialty care industry delivers targeted medical services in non-hospital settings that are often cost-effective compared to inpatient alternatives. This means that they are more desired as rising healthcare costs and ways to combat them become more and more top-of-mind. Outpatient and specialty care providers boast revenue streams that are stable due to the recurring nature of treatment for chronic conditions and long-term patient relationships. However, their reliance on government reimbursement programs like Medicare means stroke-of-the-pen risk. Additionally, scaling a network of facilities can be capital-intensive with uneven return profiles amid competition from integrated healthcare systems. Looking ahead, the industry is positioned to grow as demand for outpatient services expands, driven by aging populations, a rising prevalence of chronic diseases, and a shift toward value-based care models. Tailwinds include advancements in medical technology that support more complex procedures in outpatient settings and the increasing focus on preventive care, which can be aided by data and AI. However, headwinds such as reimbursement rate cuts, labor shortages, and the financial strain of digitization may temper growth.

The 7 outpatient & specialty care stocks we track reported a mixed Q1. As a group, revenues beat analysts’ consensus estimates by 0.7% while next quarter’s revenue guidance was 0.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 12.1% since the latest earnings results.

agilon health (NYSE: AGL)

Transforming how doctors care for seniors by shifting financial incentives from volume to outcomes, agilon health (NYSE: AGL) provides a platform that helps primary care physicians transition to value-based care models for Medicare patients through long-term partnerships and global capitation arrangements.

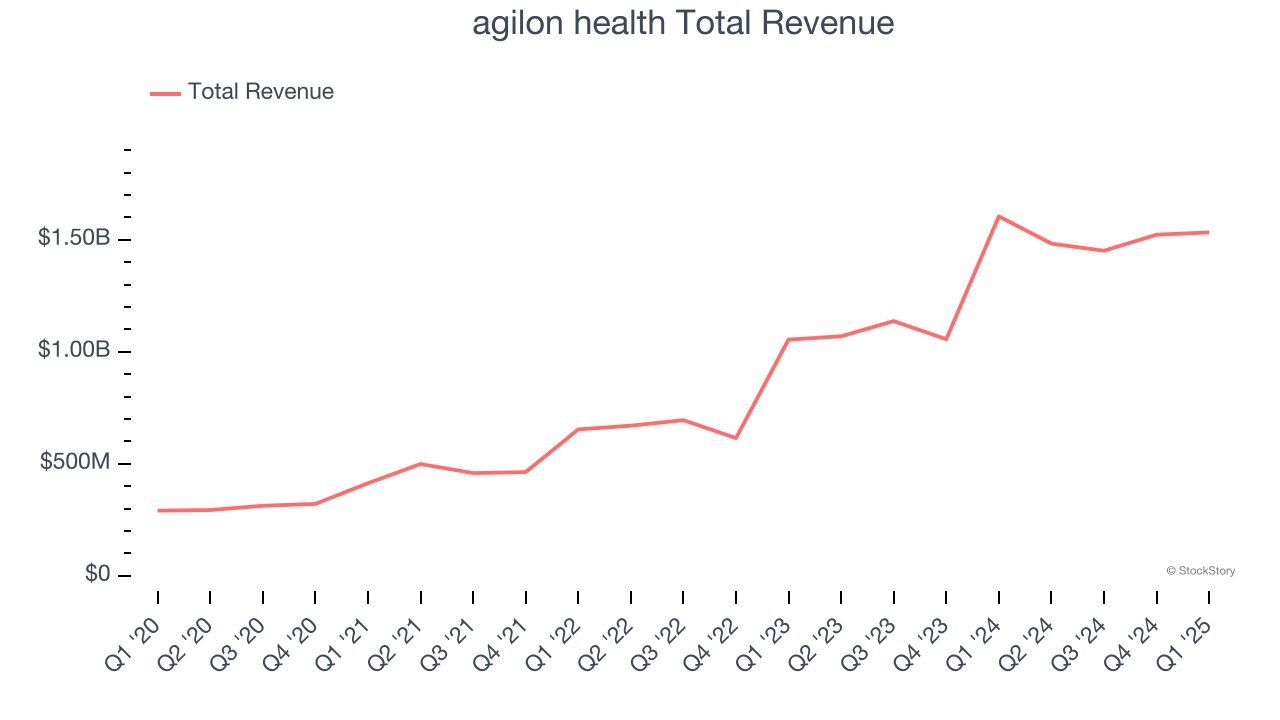

agilon health reported revenues of $1.53 billion, down 4.5% year on year. This print exceeded analysts’ expectations by 1.8%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ EPS estimates and EBITDA guidance for next quarter missing analysts’ expectations.

“I’m encouraged by our first quarter results and the progress we are making on key initiatives to drive improved operating performance. With our differentiated Total Care Model, our partnerships remain focused on the entire health of their patients, continuing to deliver significant quality outcomes, and cost-effective care to senior patients,” said Steven Sell, CEO, agilon health.

agilon health delivered the slowest revenue growth of the whole group. The company lost 36,000 customers and ended up with a total of 491,000. Unsurprisingly, the stock is down 51.4% since reporting and currently trades at $2.18.

Is now the time to buy agilon health? Access our full analysis of the earnings results here, it’s free.

Best Q1: U.S. Physical Therapy (NYSE: USPH)

With a nationwide footprint spanning 671 clinics across 42 states, U.S. Physical Therapy (NYSE: USPH) operates a network of outpatient physical therapy clinics and provides industrial injury prevention services to employers across the United States.

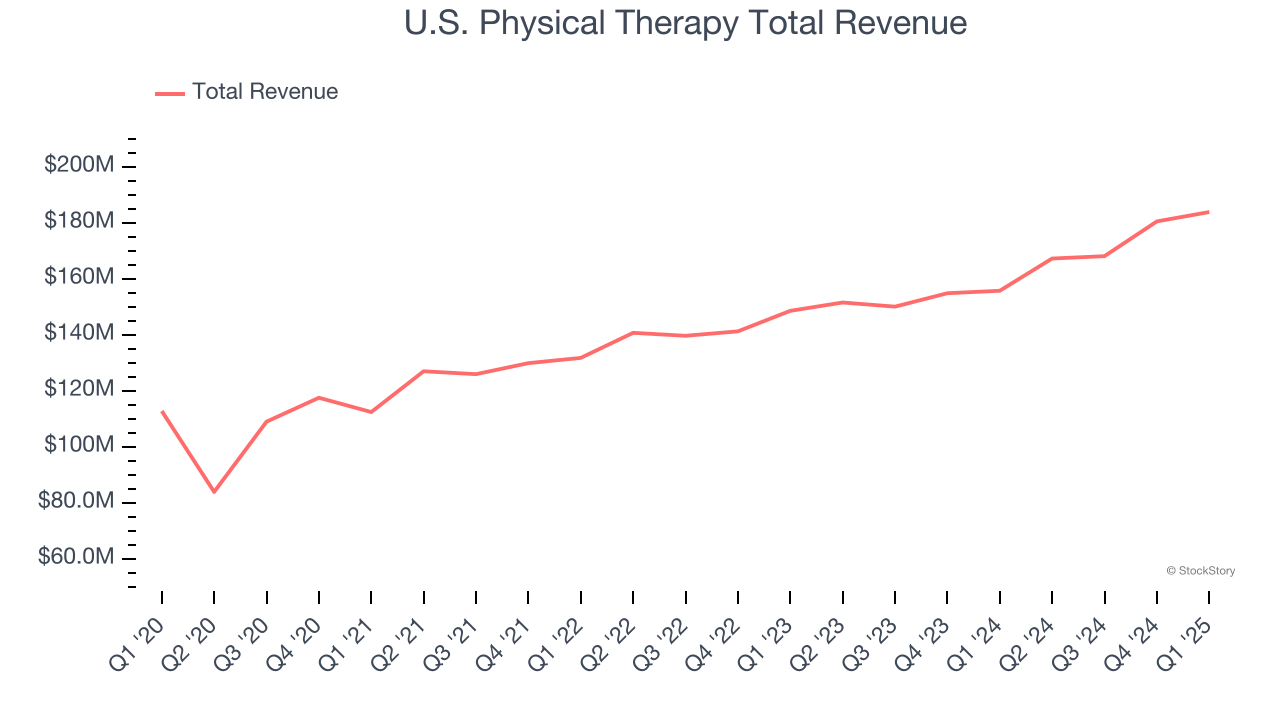

U.S. Physical Therapy reported revenues of $183.8 million, up 18.1% year on year, outperforming analysts’ expectations by 4.4%. The business had an exceptional quarter with a solid beat of analysts’ sales volume estimates and a decent beat of analysts’ EPS estimates.

U.S. Physical Therapy scored the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems content with the results as the stock is up 4.1% since reporting. It currently trades at $73.79.

Is now the time to buy U.S. Physical Therapy? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Select Medical (NYSE: SEM)

With a nationwide network spanning 46 states and over 2,700 healthcare facilities, Select Medical (NYSE: SEM) operates critical illness recovery hospitals, rehabilitation hospitals, outpatient rehabilitation clinics, and occupational health centers across the United States.

Select Medical reported revenues of $1.35 billion, up 2.4% year on year, falling short of analysts’ expectations by 2.6%. It was a softer quarter as it posted a significant miss of analysts’ EPS estimates and full-year revenue guidance missing analysts’ expectations.

Select Medical delivered the weakest performance against analyst estimates and weakest full-year guidance update in the group. As expected, the stock is down 18.2% since the results and currently trades at $14.92.

Read our full analysis of Select Medical’s results here.

LifeStance Health Group (NASDAQ: LFST)

With over 6,600 licensed mental health professionals treating more than 880,000 patients annually, LifeStance Health (NASDAQ: LFST) provides outpatient mental health services through a network of clinicians offering psychiatric evaluations, psychological testing, and therapy across 33 states.

LifeStance Health Group reported revenues of $333 million, up 10.8% year on year. This number met analysts’ expectations. Taking a step back, it was a mixed quarter as it also produced an impressive beat of analysts’ EPS estimates but EBITDA guidance for next quarter missing analysts’ expectations.

The stock is down 21.2% since reporting and currently trades at $5.16.

Read our full, actionable report on LifeStance Health Group here, it’s free.

DaVita (NYSE: DVA)

With over 2,600 dialysis centers across the United States and a presence in 13 countries, DaVita (NYSE: DVA) operates a network of dialysis centers providing treatment and care for patients with chronic kidney disease and end-stage kidney disease.

DaVita reported revenues of $3.22 billion, up 5% year on year. This result topped analysts’ expectations by 0.5%. Taking a step back, it was a slower quarter as it logged a significant miss of analysts’ full-year EPS guidance estimates.

The stock is down 5.8% since reporting and currently trades at $135.79.

Read our full, actionable report on DaVita here, it’s free.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.