The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how perishable food stocks fared in Q1, starting with Pilgrim's Pride (NASDAQ: PPC).

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

The 11 perishable food stocks we track reported a slower Q1. As a group, revenues beat analysts’ consensus estimates by 1.4%.

While some perishable food stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.1% since the latest earnings results.

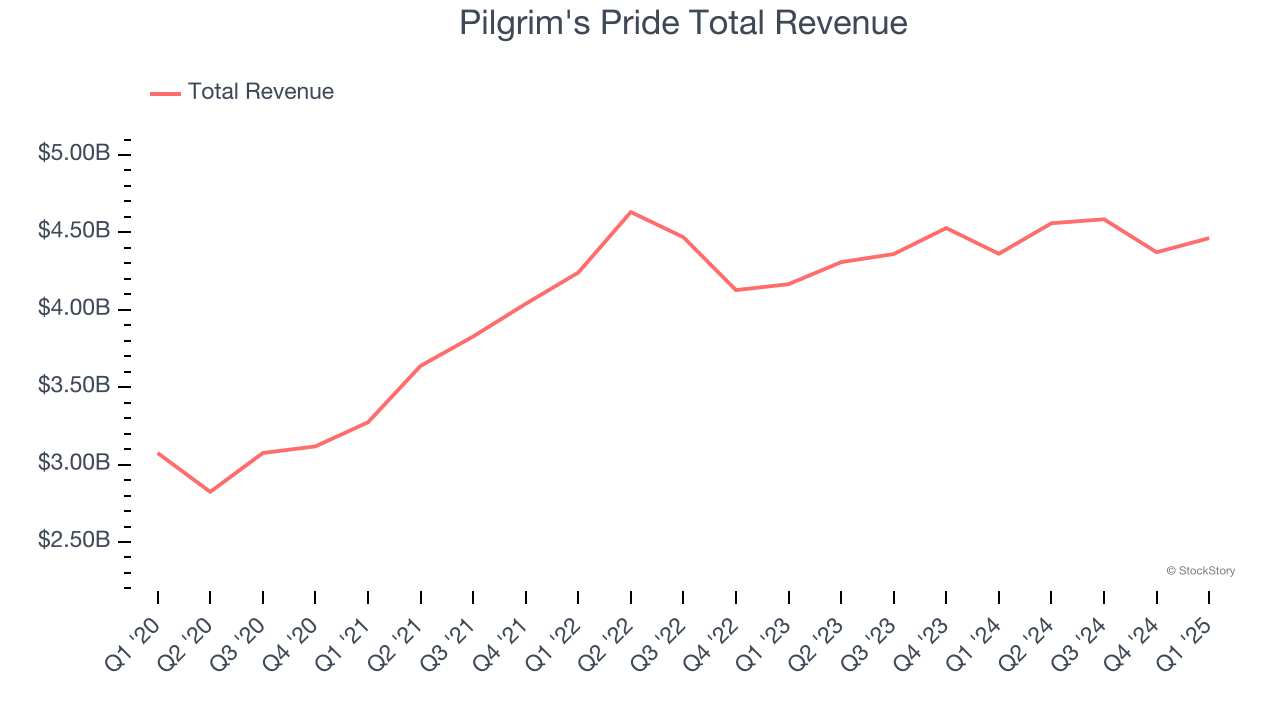

Pilgrim's Pride (NASDAQ: PPC)

Offering everything from pre-marinated to frozen chicken, Pilgrim’s Pride (NASDAQ: PPC) produces, processes, and distributes chicken products to retailers and food service customers.

Pilgrim's Pride reported revenues of $4.46 billion, up 2.3% year on year. This print fell short of analysts’ expectations by 1.6%. Overall, it was a softer quarter for the company with a miss of analysts’ EBITDA and gross margin estimates.

“While facing volatility during the quarter, we maintained our focus on controlling the controllables and consistent execution of our strategies,” said Fabio Sandri, Pilgrim’s President and CEO.

The stock is down 17.4% since reporting and currently trades at $45.11.

Read our full report on Pilgrim's Pride here, it’s free.

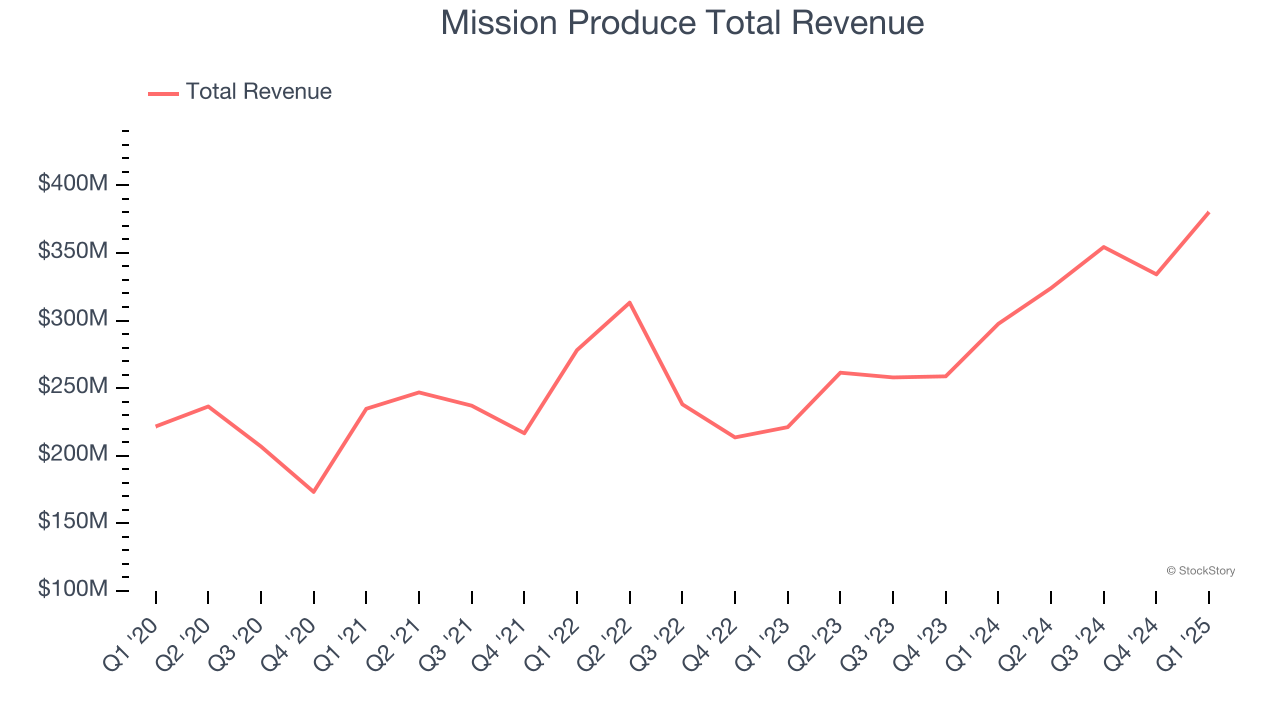

Best Q1: Mission Produce (NASDAQ: AVO)

Founded in 1983 in California, Mission Produce (NASDAQ: AVO) grows, packages, and distributes avocados.

Mission Produce reported revenues of $380.3 million, up 27.8% year on year, outperforming analysts’ expectations by 28.4%. The business had a stunning quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Mission Produce delivered the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 11% since reporting. It currently trades at $11.70.

Is now the time to buy Mission Produce? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Beyond Meat (NASDAQ: BYND)

A pioneer at the forefront of the plant-based protein revolution, Beyond Meat (NASDAQ: BYND) is a food company specializing in alternatives to traditional meat products.

Beyond Meat reported revenues of $68.73 million, down 9.1% year on year, falling short of analysts’ expectations by 8.3%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

Beyond Meat delivered the weakest performance against analyst estimates and slowest revenue growth in the group. Interestingly, the stock is up 32.5% since the results and currently trades at $3.38.

Read our full analysis of Beyond Meat’s results here.

Freshpet (NASDAQ: FRPT)

Standing out from typical processed pet foods, Freshpet (NASDAQ: FRPT) is a pet food company whose product portfolio includes natural meals and treats for dogs and cats.

Freshpet reported revenues of $263.2 million, up 17.6% year on year. This number beat analysts’ expectations by 1.4%. Zooming out, it was a mixed quarter as it also logged a solid beat of analysts’ adjusted operating income estimates but full-year revenue guidance missing analysts’ expectations significantly.

Freshpet had the weakest full-year guidance update among its peers. The stock is flat since reporting and currently trades at $76.22.

Read our full, actionable report on Freshpet here, it’s free.

Tyson Foods (NYSE: TSN)

Started as a simple trucking business, Tyson Foods (NYSE: TSN) is one of the world’s largest producers of chicken, beef, and pork.

Tyson Foods reported revenues of $13.07 billion, flat year on year. This result missed analysts’ expectations by 0.7%. More broadly, it was actually a strong quarter as it recorded an impressive beat of analysts’ EBITDA estimates and a decent beat of analysts’ EPS estimates.

The stock is down 8.9% since reporting and currently trades at $55.40.

Read our full, actionable report on Tyson Foods here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.