Cork, Ireland-based Johnson Controls International plc (JCI) engineers, manufactures, commissions, and retrofits sustainable building products and systems. Valued at a market cap of $86.5 billion, the company’s core operations center on the OpenBlue digital platform, which integrates artificial intelligence to optimize energy efficiency, decarbonization, and mission-critical performance for industries such as data centers, healthcare, and education.

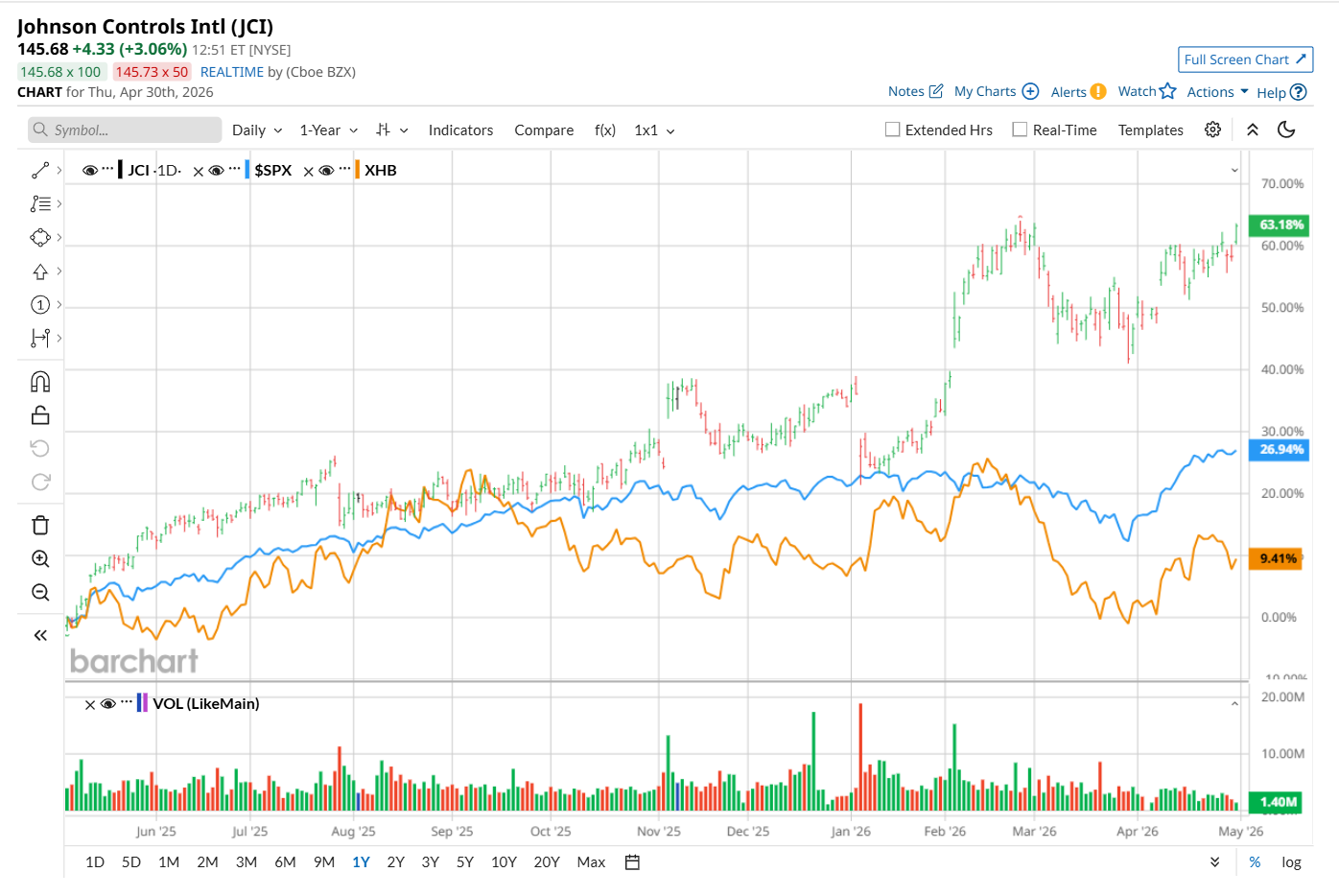

This industrial company has significantly outpaced the broader market over the past 52 weeks. Shares of JCI have rallied 73.3% over this time frame, while the broader S&P 500 Index ($SPX) has gained 28.3%. Moreover, on a YTD basis, the stock is up 21.4%, compared to SPX’s 4.2% rise.

Zooming in further, JCI has also outperformed the industry-focused SPDR S&P Homebuilders ETF’s (XHB) 11.9% uptick over the past 52 weeks and 2.9% rise on a YTD basis.

JCI’s outperformance was driven by record demand, with its backlog reaching $18.2 billion, supported by strong momentum in data center and life sciences projects. Solid execution, the launch of new chiller platforms, and its business system enhancements contributed to improved margins and service growth across regions. Additionally, management raised its full-year guidance, highlighting continued strength in energy-intensive markets, growing digital and AI adoption, and a robust pipeline for further order growth.

For the current fiscal year, ending in September, analysts expect JCI’s EPS to grow 26.1% year over year to $4.74. The company’s earnings surprise history is promising. It exceeded the consensus estimates in each of the last four quarters.

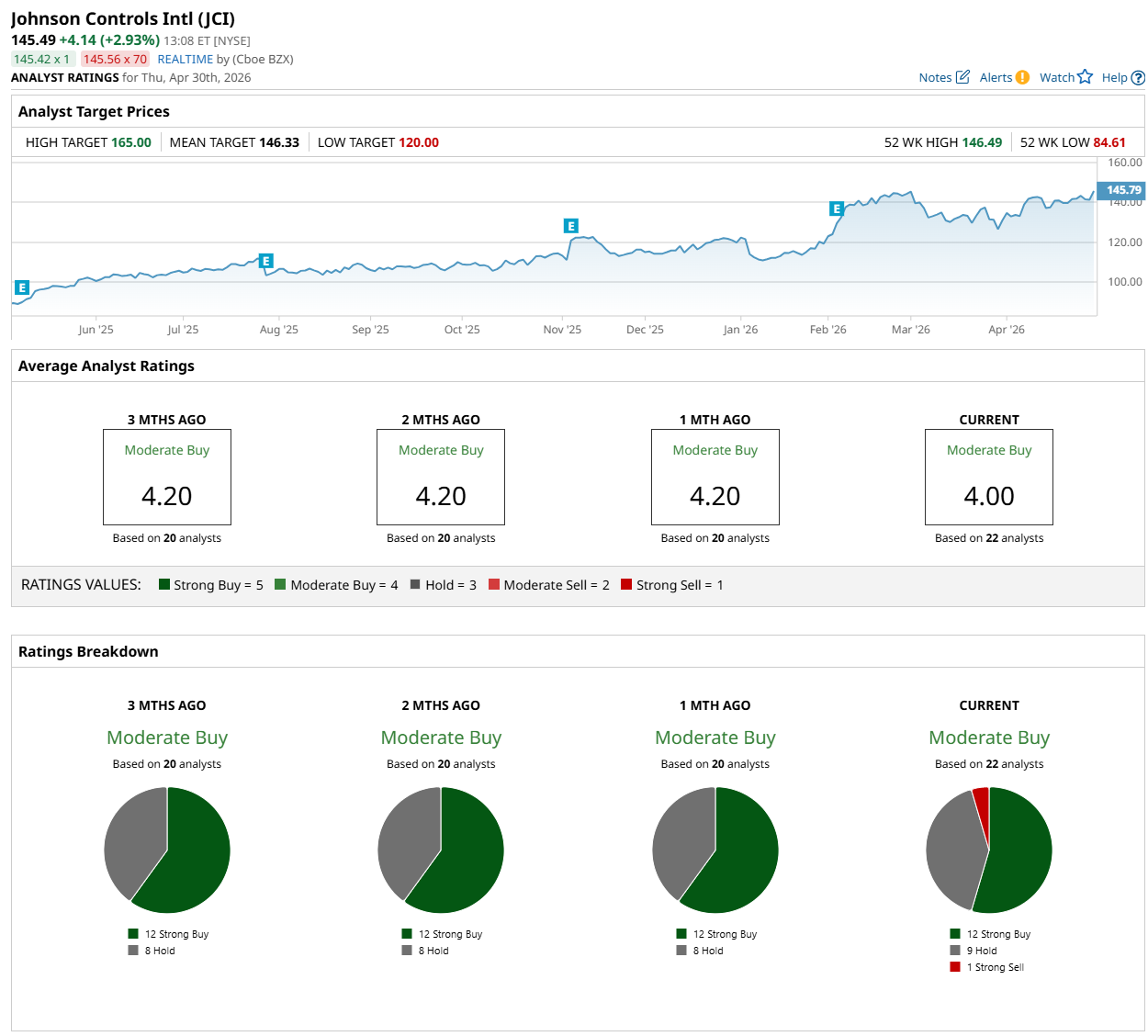

Among the 22 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on 12 “Strong Buy,” nine “Hold,” and one “Strong Sell” rating.

The configuration is less bullish than a month ago, with no analyst suggesting a "Strong Sell” rating.

On Apr. 14, BNP Paribas initiated coverage of JCI with an “Underperform” rating and $120 price target.

The mean price target of $146.33 indicates a marginal potential upside from the current levels, while its Street-high price target of $165 suggests a 13.4% premium.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- A $20 Billion Reason to Buy Dividend-Paying Visa Stock Now

- SanDisk Stock Just Hit New Record Highs With Wall Street

- GLP-1 Sales Continue to Lift Eli Lilly. Does That Make LLY Stock a Buy?

- Western Digital Stock Has More Than Doubled YTD, but Bank of America Still Thinks You Should Buy Ahead of Earnings