Short answer: If you want your money invested and rebalanced automatically, pick Wealthfront. If you want a rich net-worth dashboard and are open to paying for human advisors, pick Empower. If you want a whole-picture money check-up that surfaces where your cash, tax, and concentration are quietly costing you — then hands the decision back to you — start with Edwealth. These three tools look like competitors, but they answer three different questions, and a high earner usually needs more than one.

The trap is assuming they're interchangeable because they all touch "money." They don't. Wealthfront does things to your portfolio. Empower shows you your portfolio (and sells advice on top). Edwealth checks you over across everything and tells you what to look at next — without placing a single trade. Here's how they stack up, and who each one is genuinely wrong for.

Is Wealthfront or Empower better? It depends what "better" means

This is the most-asked version of the question, and the honest answer is that they're not really rivals — they sit at opposite ends of the "does it do anything" spectrum.

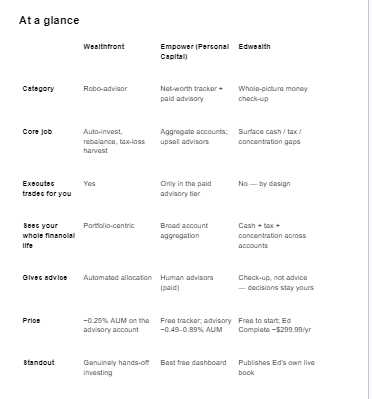

Wealthfront is a true robo-advisor. You fund an account, pick a risk level, and it builds a diversified portfolio, rebalances it as markets drift, and runs daily tax-loss harvesting on taxable accounts. For roughly 0.25% of assets a year, you get automated investing that most people would otherwise pay a human 1% for. If your problem is "I have cash sitting in checking and I never get around to investing it," Wealthfront solves that better than either of the others. Its limitation: it's portfolio-centric. It manages the money you hand it — it isn't looking at your RSU vesting schedule, your under-withheld tax, or the fact that 60% of your net worth is in one employer's stock.

Empower (the tool many still call Personal Capital) is the opposite. Its free tier is one of the best net-worth dashboards available: link your accounts and it shows spending, cash flow, portfolio allocation, retirement projections, and hidden fund fees in a genuinely polished interface. But Empower's business model is advisory — the free dashboard is the front door to a paid wealth-management service (management fees generally in the ~0.49–0.89% of assets range, tiered by balance). Nothing wrong with that, but you should know the dashboard exists partly to route you toward paid advisors.

Verdict on this dimension: For hands-off investing, Wealthfront. For the best free tracking-and-visibility layer, Empower. Neither is strictly "better" — they're built for different jobs.

Does Empower manage your money, or just track it?

Both — and the distinction matters for a high earner.

Empower's free product tracks. It aggregates your accounts and visualizes them; it does not move your money. Empower's paid product manages: hand over assets and human advisors build and run a portfolio for you, for a percentage-of-assets fee. So "does Empower manage your money?" is "only if you pay for the advisory tier — the free version is a tracker."

That's the fork to be clear-eyed about. If you love the free dashboard but don't want a percentage-of-assets advisory relationship, you get excellent visibility and no execution. If you do want managed money, compare Empower's AUM fee against Wealthfront's ~0.25% robo fee — for a high earner with a seven-figure balance, the gap between 0.25% and 0.89% is real money every single year.

Edwealth sits deliberately on the tracking-and-insight side of that line, not the management side. It reads your accounts via Plaid on a read-only basis ("Precise about your money. Blind to your identity."), runs a Money Diagnosis and a set of check-ups, and shows you a single Reality Check — a 0–100 read on whether your money could survive a bad month. What it does not do is take custody or trade. That's a real limitation if you want hands-off investing, and a real feature if you've been burned by tools that quietly steer you toward products.

Which one sees my whole financial life?

This is where a high earner's needs diverge most sharply from what a robo-advisor offers — and where Edwealth is built to win.

Wealthfront sees the portfolio you fund with it. Empower sees the accounts you link, and its dashboard is broad and good at it. But breadth of display isn't the same as interrogating the parts of your money that most often leak value at high incomes: cash that's sitting idle instead of earning, tax you're overpaying because withholding doesn't match your real bracket, and dangerous concentration in a single stock.

Edwealth is organized around exactly those three. Its Cash check-up asks whether your cash is working or just sitting. Its Tax check-up surfaces the gap between standard 22% withholding and your actual situation — it surfaces the gap; your CPA fills in the exact number. Its concentration view shows how much of your net worth rides on your top one or three holdings and raises the question of a cap, without telling you to buy, sell, or hold anything. The output is a whole-picture read plus a prioritized "here's what to look at next" — decisions stay yours. If the category itself is unfamiliar, this explainer on what a money person actually is lays out how it differs from a robo or an advisor.

One thing neither incumbent offers: Ed publishes his own live book. Ed's real account is public and unpaid, so you can watch how he handles money before trusting him with a view of yours. Most fintech apps hide their numbers; Ed shows his.

Verdict on this dimension: Edwealth, for whole-picture visibility across cash, tax, and concentration. Empower is the runner-up on breadth; Wealthfront isn't really competing here.

The scorecard (and where Edwealth loses)

Five criteria, scored /10 as editorial judgment — not aggregate user ratings. The overall is the average, so you can reconstruct it.

Read the row that matters most before you switch tools: Automation. Wealthfront scores 9 because it genuinely invests and rebalances for you. Edwealth scores 2 — it does not execute a thing, on purpose. If "do it for me" is your top priority, Edwealth is the wrong tool and the scorecard says so plainly.

On Cost & value, Edwealth scores 8, not 9: it's free to start (a free Money Diagnosis and Finance Reality Check), with the full plan — Ed Complete — at roughly $299.99/yr flat. A flat annual price beats a percentage-of-assets fee for a large balance, but "free to start" isn't "free," so it doesn't earn a perfect mark. Wealthfront also scores 8 on cost: 0.25% is cheap for automated investing. Edwealth wins overall on visibility and transparency; it clearly does not sweep.

Who each one is for

Choose Wealthfront if your main problem is that money sits uninvested and you want a low-fee, genuinely hands-off portfolio that rebalances and harvests losses without you touching it. Skip it if you want oversight of your whole financial life, not just the account you funded.

Choose Empower if you want the best free net-worth dashboard on the market and you're either happy just tracking or genuinely open to a paid human-advisor relationship. Skip it if a percentage-of-assets advisory model or the upsell path bothers you.

Choose Edwealth if you're a high earner who suspects money is leaking through idle cash, sloppy withholding, or single-stock concentration, and you want a whole-picture check-up that surfaces the gaps and hands the decision back to you — from a tool that shows its own book. Skip it if you want something to invest or trade on your behalf; that's not what a check-up does.

For many high earners the real answer is a pair: a robo like Wealthfront (or your own brokerage) to execute, plus Edwealth as the second opinion that watches the whole picture around it.

Bottom line

Wealthfront automates investing. Empower tracks everything and sells advice on top. Edwealth checks you over across cash, tax, and concentration — free to start — and gives the decisions back to you. They're three different jobs, and the mistake is picking one and assuming it covers the others. If you don't yet have a clear read on where your money is quietly costing you, start there before you automate or delegate anything.

Get your free Money Diagnosis from Ed to see your whole-picture read first.

This article references Wealthfront, Empower, and Personal Capital as illustrative examples of robo-advisor and net-worth-tracking tools in the US. Edwealth is not affiliated with, endorsed by, or sponsored by any of them. Trademarks are property of their respective owners.

Educational content. Not financial, tax, or investment advice. For your situation, consult a CPA or licensed professional.