Healthcare products company West Pharmaceutical Services (NYSE: WST) announced better-than-expected revenue in Q1 CY2025, but sales were flat year on year at $698 million. The company’s full-year revenue guidance of $2.96 billion at the midpoint came in 2% above analysts’ estimates. Its non-GAAP profit of $1.45 per share was 18.1% above analysts’ consensus estimates.

Is now the time to buy West Pharmaceutical Services? Find out by accessing our full research report, it’s free.

West Pharmaceutical Services (WST) Q1 CY2025 Highlights:

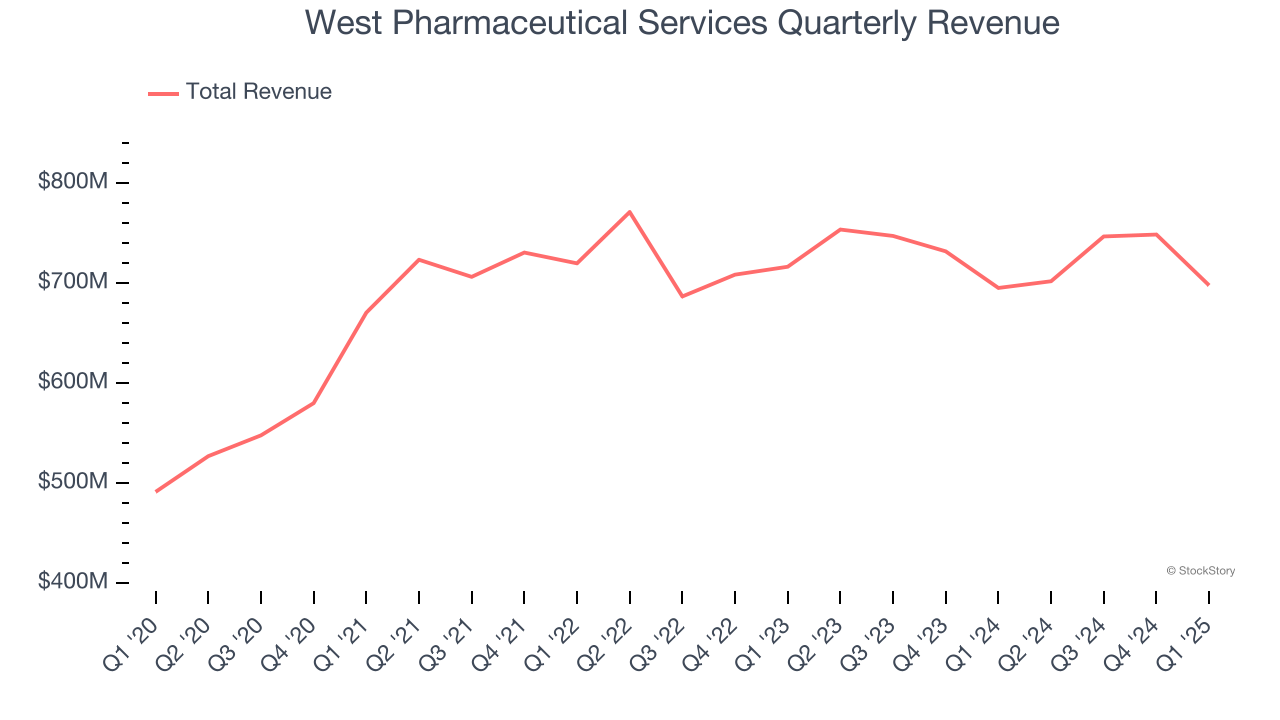

- Revenue: $698 million vs analyst estimates of $684.5 million (flat year on year, 2% beat)

- Adjusted EPS: $1.45 vs analyst estimates of $1.23 (18.1% beat)

- Adjusted EBITDA: $147 million vs analyst estimates of $150.6 million (21.1% margin, 2.4% miss)

- The company lifted its revenue guidance for the full year to $2.96 billion at the midpoint from $2.89 billion, a 2.4% increase

- Management raised its full-year Adjusted EPS guidance to $6.25 at the midpoint, a 2.5% increase

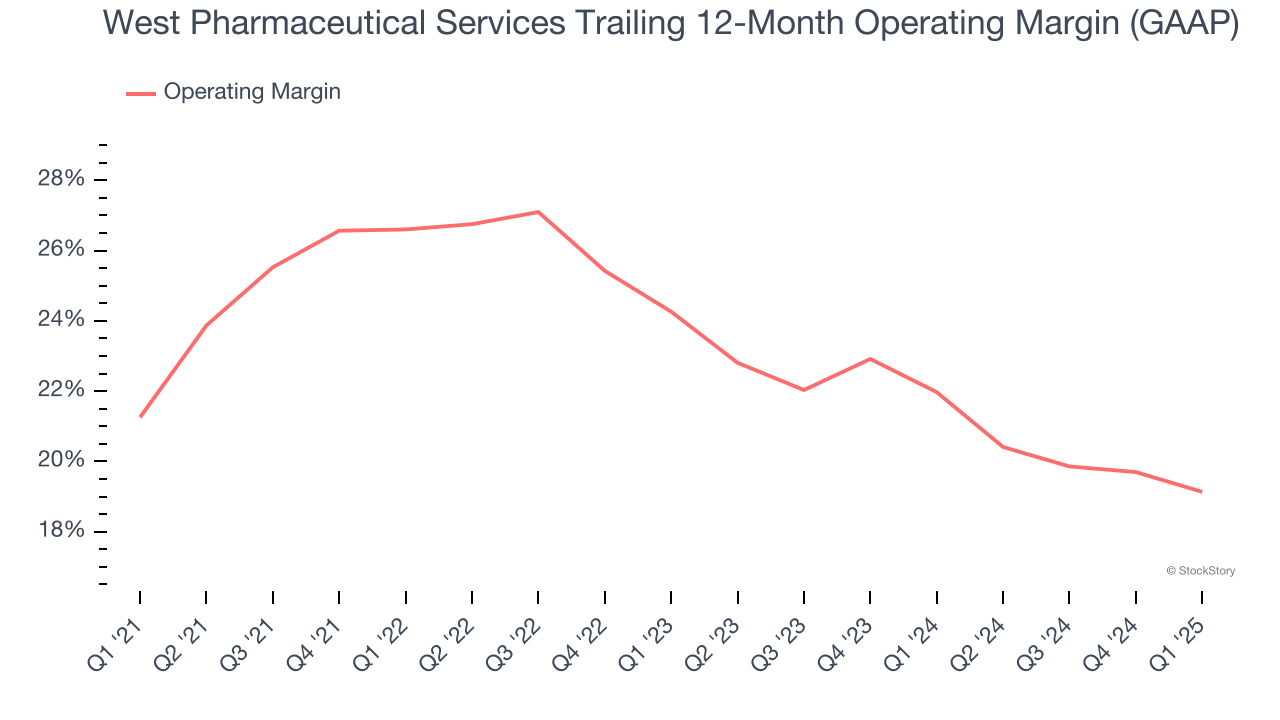

- Operating Margin: 15.3%, down from 17.7% in the same quarter last year

- Free Cash Flow Margin: 8.3%, up from 4% in the same quarter last year

- Market Capitalization: $15.77 billion

Eric M. Green, President, Chief Executive Officer and Chair of the Board, commented: "I am pleased to report we delivered a solid first quarter as both revenues and adjusted-diluted EPS exceeded our first quarter guidance. We are capitalizing on areas of strength and making progress to improve margins and returns on invested capital. As such, we expect our positive trends to continue and remain confident in our ability to execute and achieve our guidance. We are closely monitoring potential impacts, both political and macroeconomic, in order to react as quickly as possible with offsetting mitigating measures. Our team continues to enable the success of our customers and deliver value for all of our stakeholders."

Company Overview

Founded in 1923 and serving as a critical link in the pharmaceutical supply chain, West Pharmaceutical Services (NYSE: WST) manufactures specialized packaging, containment systems, and delivery devices for injectable drugs and healthcare products.

Drug Development Inputs & Services

Companies specializing in drug development inputs and services play a crucial role in the pharmaceutical and biotechnology value chain. Essential support for drug discovery, preclinical testing, and manufacturing means stable demand, as pharmaceutical companies often outsource non-core functions with medium to long-term contracts. However, the business model faces high capital requirements, customer concentration, and vulnerability to shifts in biopharma R&D budgets or regulatory frameworks. Looking ahead, the industry will likely enjoy tailwinds such as increasing investment in biologics, cell and gene therapies, and advancements in precision medicine, which drive demand for sophisticated tools and services. There is a growing trend of outsourcing in drug development for nimbleness and cost efficiency, which benefits the industry. On the flip side, potential headwinds include pricing pressures as efforts to contain healthcare costs are always top of mind. An evolving regulatory backdrop could also slow innovation or client activity.

Sales Growth

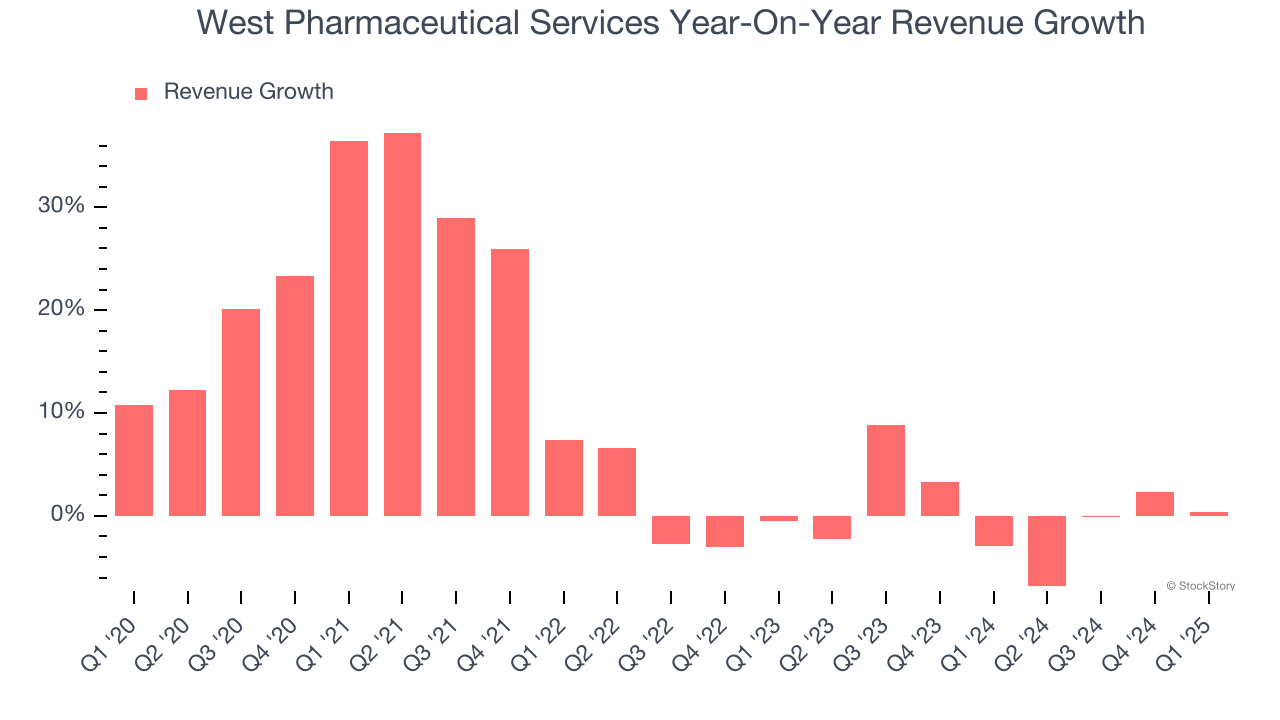

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, West Pharmaceutical Services grew its sales at a decent 8.9% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. West Pharmaceutical Services’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, West Pharmaceutical Services’s $698 million of revenue was flat year on year but beat Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to grow 1.7% over the next 12 months, similar to its two-year rate. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

West Pharmaceutical Services has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 22.7%.

Looking at the trend in its profitability, West Pharmaceutical Services’s operating margin decreased by 2.1 percentage points over the last five years. This performance was caused by more recent speed bumps as the company’s margin fell by 5.1 percentage points on a two-year basis. We’re disappointed in these results because it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, West Pharmaceutical Services generated an operating profit margin of 15.3%, down 2.3 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

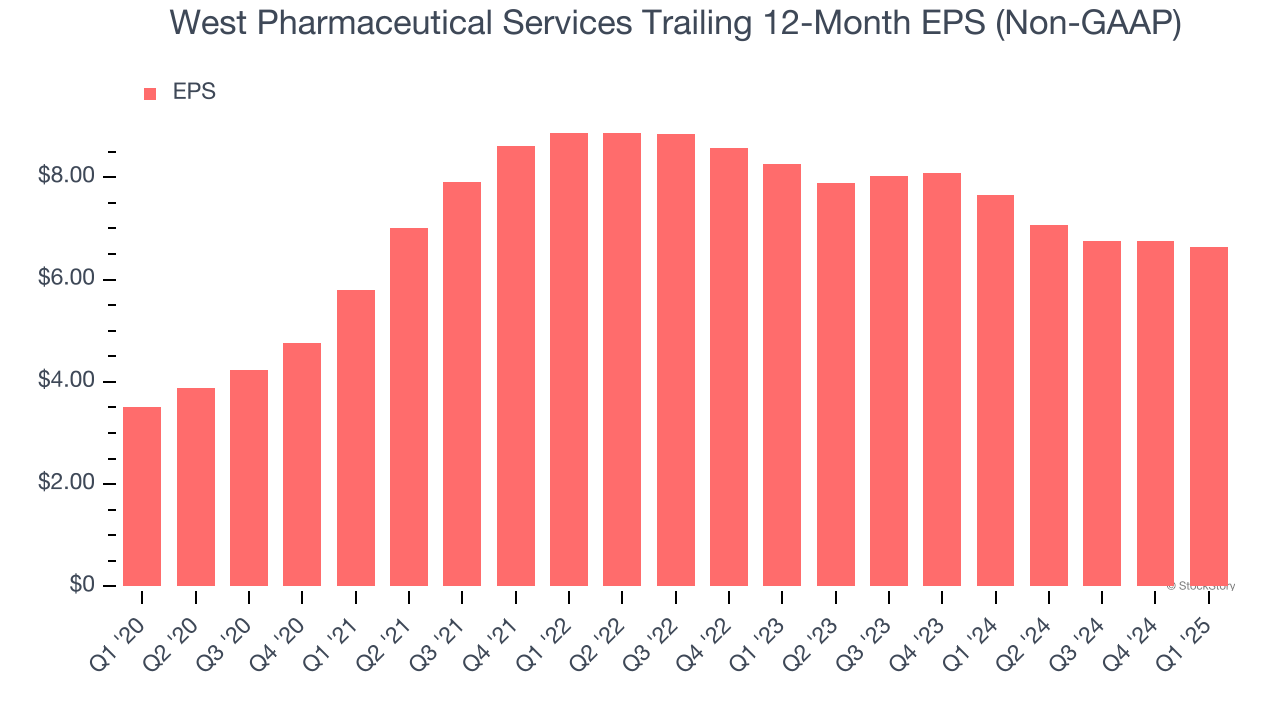

West Pharmaceutical Services’s EPS grew at a spectacular 13.6% compounded annual growth rate over the last five years, higher than its 8.9% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t expand.

We can take a deeper look into West Pharmaceutical Services’s earnings to better understand the drivers of its performance. A five-year view shows that West Pharmaceutical Services has repurchased its stock, shrinking its share count by 3.3%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, West Pharmaceutical Services reported EPS at $1.45, down from $1.56 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects West Pharmaceutical Services’s full-year EPS of $6.64 to shrink by 4.6%.

Key Takeaways from West Pharmaceutical Services’s Q1 Results

We enjoyed seeing West Pharmaceutical Services beat analysts’ revenue and EPS expectations this quarter. We were also glad it lifted its full-year revenue and EPS guidance. Overall, we think this was a solid "beat-and-raise" quarter. The stock traded up 5.9% to $230.42 immediately after reporting.

West Pharmaceutical Services may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.