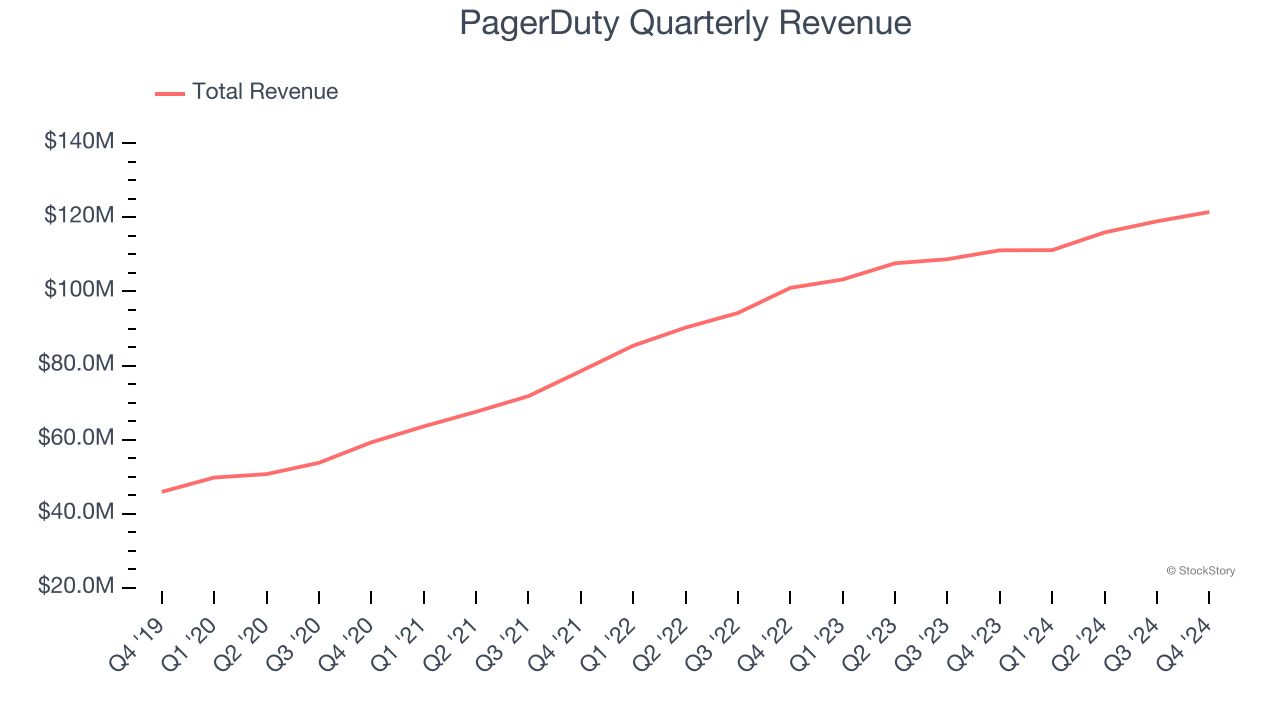

IT incident response platform PagerDuty (NYSE:PD) announced better-than-expected revenue in Q4 CY2024, with sales up 9.3% year on year to $121.4 million. On the other hand, next quarter’s revenue guidance of $119 million was less impressive, coming in 1.9% below analysts’ estimates. Its non-GAAP profit of $0.22 per share was 36% above analysts’ consensus estimates.

Is now the time to buy PagerDuty? Find out by accessing our full research report, it’s free.

PagerDuty (PD) Q4 CY2024 Highlights:

- Revenue: $121.4 million vs analyst estimates of $119.8 million (9.3% year-on-year growth, 1.4% beat)

- Adjusted EPS: $0.22 vs analyst estimates of $0.16 (36% beat)

- Adjusted Operating Income: $22.27 million vs analyst estimates of $15.49 million (18.3% margin, 43.8% beat)

- Management’s revenue guidance for the upcoming financial year 2026 is $503.5 million at the midpoint, missing analyst estimates by 1.3% and implying 7.7% growth (vs 8.5% in FY2025)

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.93 at the midpoint, beating analyst estimates by 3.8%

- Operating Margin: -9.6%, up from -30.1% in the same quarter last year

- Free Cash Flow Margin: 23.5%, up from 16.3% in the previous quarter

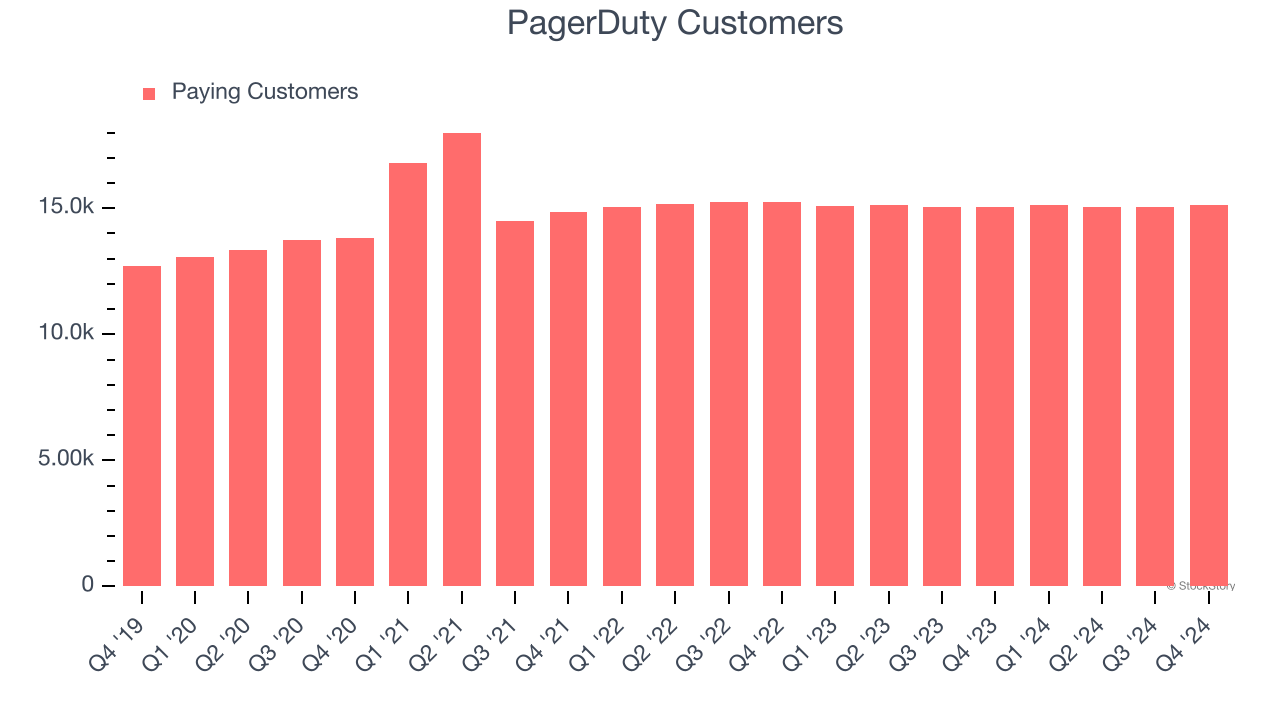

- Customers: 15,114, up from 15,050 in the previous quarter

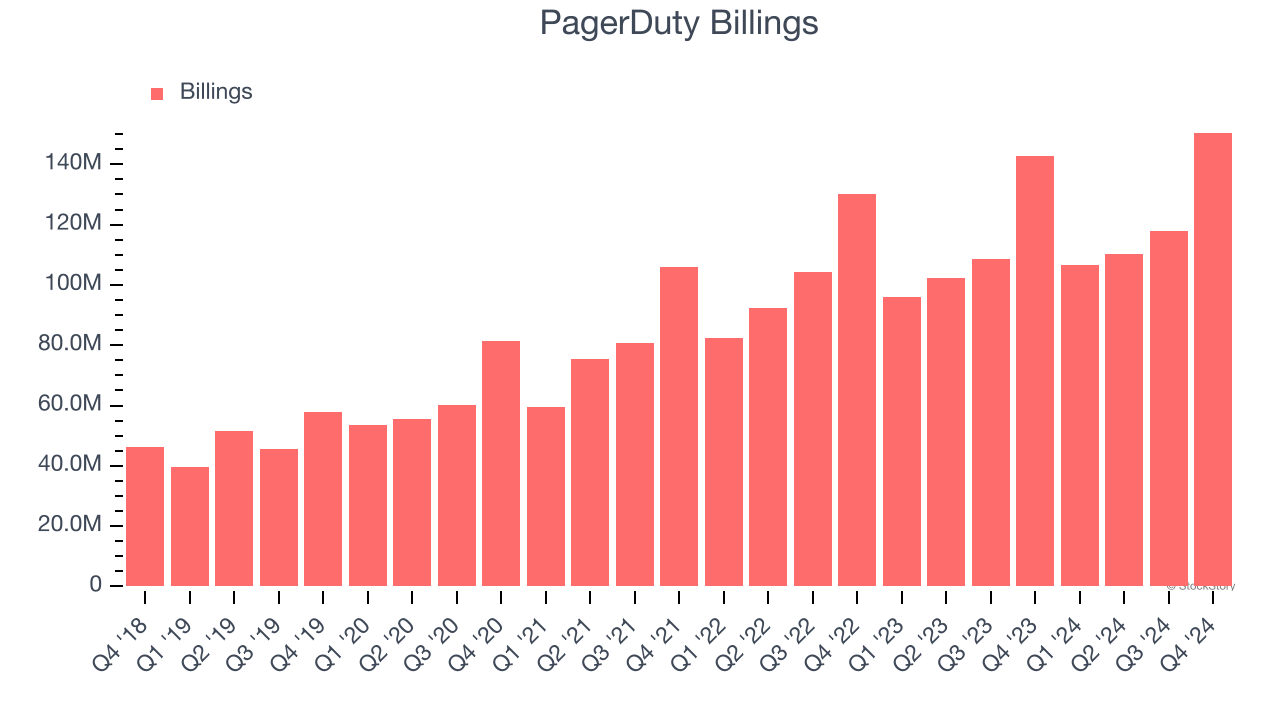

- Billings: $150.5 million at quarter end, up 5.4% year on year

- Market Capitalization: $1.47 billion

Company Overview

Started by three former Amazon engineers, PagerDuty (NYSE:PD) is a software-as-a-service platform that helps companies respond to IT incidents fast and make sure that any downtime is minimized.

Cloud Monitoring

Software is eating the world, increasing organizations’ reliance on digital-only solutions. As more workloads and applications move to the cloud, the reliability of the underlying cloud infrastructure becomes ever more critical and ever more complex. To solve this challenge, companies and their engineering teams have turned to a range of cloud monitoring tools that provide them with the visibility to troubleshoot issues in real-time.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, PagerDuty grew its sales at a 18.4% annual rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, PagerDuty reported year-on-year revenue growth of 9.3%, and its $121.4 million of revenue exceeded Wall Street’s estimates by 1.4%. Company management is currently guiding for a 7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.3% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

PagerDuty’s billings came in at $150.5 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 8.1% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Customer Base

PagerDuty reported 15,114 customers at the end of the quarter, a sequential increase of 64. That’s a little better than last quarter and quite a bit above the typical growth we’ve seen over the previous year. Shareholders should take this as an indication that PagerDuty has made some recent improvements to its go-to-market strategy and that they are working well for the time being.

Key Takeaways from PagerDuty’s Q4 Results

We were impressed by PagerDuty’s strong growth in customers this quarter, which allowed it to beat analysts' revenue, EPS, and adjusted operating income expectations. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. On the other hand, its full-year revenue guidance slightly missed. Overall, this quarter was mixed due to the weaker top-line outlook. The good news seems to be driving the move as the stock traded up 9.2% to $17 immediately after reporting.

Is PagerDuty an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.