Based in Pawtucket, Rhode Island, Hasbro, Inc. (HAS) runs a global entertainment and toy company that delivers groundbreaking play experiences to over 500 million kids, families, and fans worldwide through physical and digital games, video games, toys, licensed consumer products, location-based entertainment, film, TV, and more.

The company stands behind some of the most recognizable names in the business, including Monopoly, Transformers, NERF, Play-Doh, Dungeons & Dragons, and Magic: The Gathering. Carrying a market cap of roughly $13.3 billion, it has been playing the long game for over 164 years now.

On the price performance front, HAS stock has left the broader market eating its dust. Over the past 52 weeks, the stock climbed 42.5%, and in 2026 alone, it tacked on 18.5%. To put that in perspective, the S&P 500 Index ($SPX) posted gains of 23.3% and 7.4% over those same respective periods, meaning Hasbro has outrun the broader index on both timelines.

The story gets even better when stacked against the sector. The State Street Consumer Discretionary Select Sector SPDR ETF (XLY) has gained only 5.9% over the last 52 weeks and sits 3.4% in the red year-to-date (YTD), which puts HAS stock well ahead of its own sector on both counts.

The momentum carried straight into the earnings season. On April 23, HAS stock jumped nearly 6.6% after the company shared certain unaudited preliminary financial figures for Q1 FY2026. Preliminary revenue pointed to approximately $970 million to $985 million, reflecting a 9% to 11% increase over the prior year.

Preliminary operating profit landed between approximately $235 million and $245 million, marking a 38% to 44% jump year over year. Meanwhile, preliminary adjusted operating profit came in at roughly $250 million to $260 million, up 12% to 17% from the prior year. The company will put the full picture on the table when it releases its official Q1 FY2026 results before the market opens on Wednesday, May 20.

The broader earnings outlook keeps the optimism going as analysts have penciled in diluted EPS growth of 4.7% year over year for FY2026, which ends in December, putting the figure at $5.80. Notably, Hasbro has beaten EPS estimates in each of its four most recent quarters, building a track record of consistently clearing the bar it sets for itself.

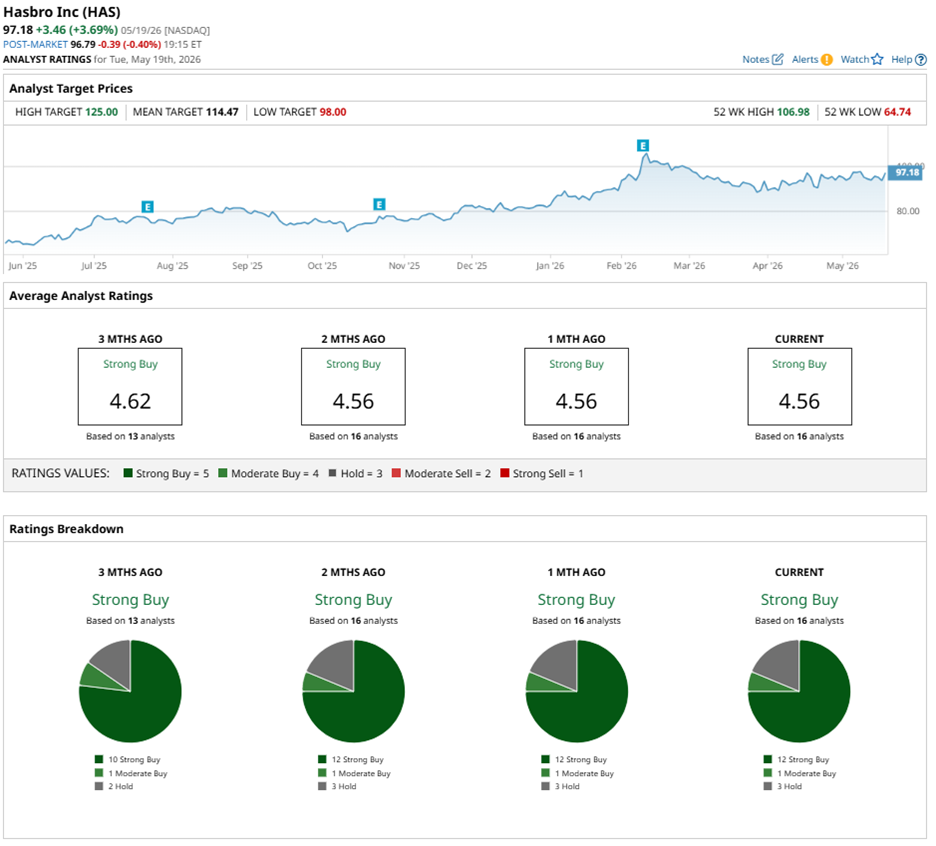

Wall Street has placed HAS stock in "Strong Buy" territory, and the conviction behind that call has only grown stronger. Among 16 analysts currently covering the stock, 12 rate it a "Strong Buy," one has issued a "Moderate Buy," while three carry a "Hold" rating.

The current analyst sentiment marks a clear improvement from three months ago, when only 10 analysts had assigned the stock a "Strong Buy," signaling that more of the Street is coming around to the bull case.

In fact, Morgan Stanley analyst Megan Alexander joined the chorus on May 14 by upping her price target from $122 to $123 while keeping her "Overweight" rating on HAS stock.

To that end, the average price target of $114.47 implies potential upside of 17.8%, while the Street-High target of $125 suggests a gain of 28.6% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Amesite Stock Soars 150% on New Enterprise Deal. What to Know.

- Cerebras Systems Is Being Called the Next Nvidia, But 2 Surprising Details Change the Story

- Nasdaq Futures Climb as Bond Yields Fall, Nvidia Earnings in Focus

- This High-Yield REIT Just Hiked Its Dividend By 7.1%. Its Shares Look Compelling Here.