Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at TFS Financial (NASDAQ: TFSL) and its peers.

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

The 16 thrifts & mortgage finance stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 4.7% while next quarter’s revenue guidance was 0.5% below.

Thankfully, share prices of the companies have been resilient as they are up 5.4% on average since the latest earnings results.

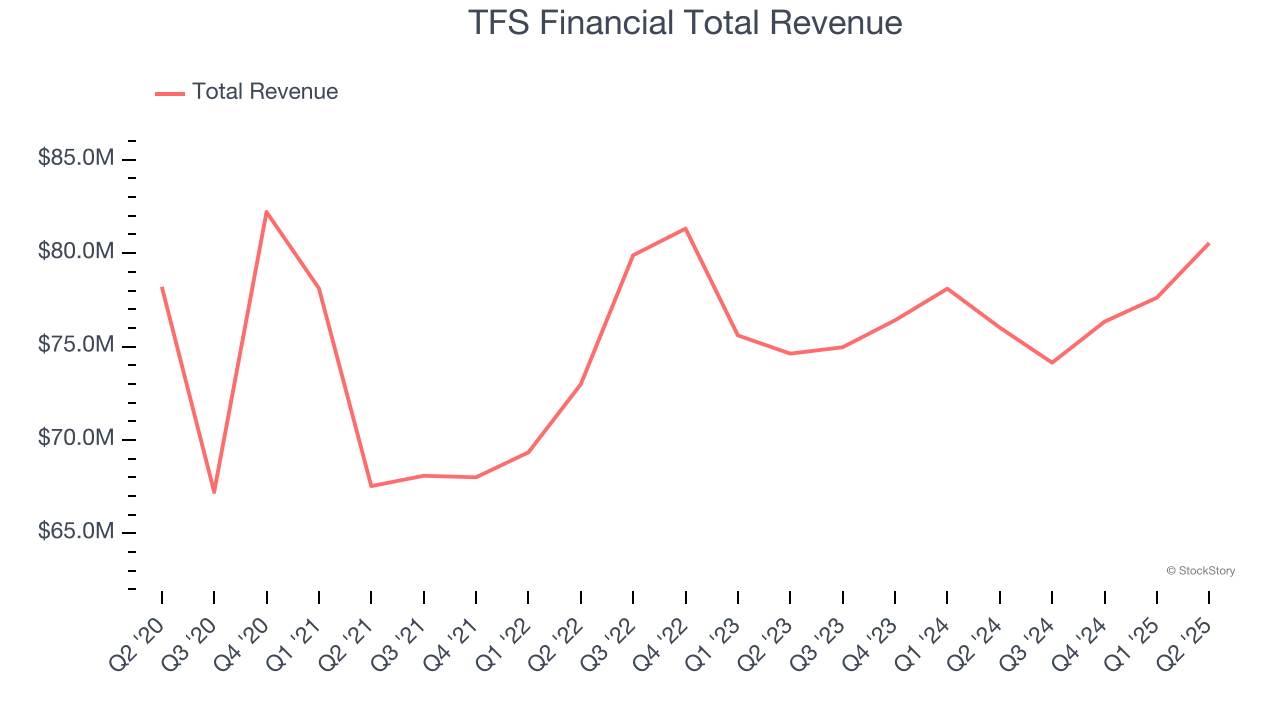

TFS Financial (NASDAQ: TFSL)

Tracing its roots back to 1938 during the Great Depression era when savings and loans were vital to homeownership, TFS Financial (NASDAQ: TFSL) is a savings and loan holding company that provides mortgage lending, deposit services, and other retail banking products primarily in Ohio and Florida.

TFS Financial reported revenues of $80.54 million, up 6% year on year. This print fell short of analysts’ expectations by 0.8%. Overall, it was a slower quarter for the company with EPS in line with analysts’ estimates and a slight miss of analysts’ revenue estimates.

Interestingly, the stock is up 11.6% since reporting and currently trades at $14.10.

Read our full report on TFS Financial here, it’s free for active Edge members.

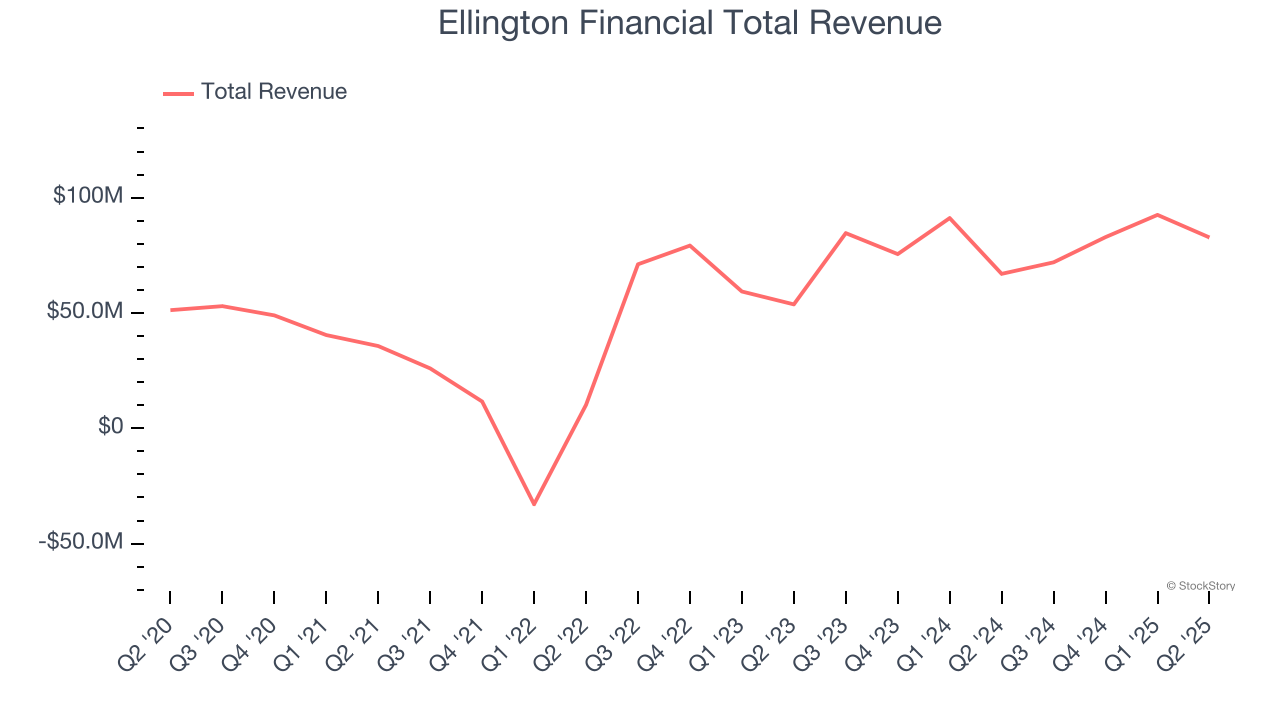

Best Q2: Ellington Financial (NYSE: EFC)

Operating under the guidance of Ellington Management Group, a respected name in structured credit markets, Ellington Financial (NYSE: EFC) acquires and manages a diverse portfolio of mortgage-related, consumer-related, and other financial assets to generate returns for investors.

Ellington Financial reported revenues of $82.76 million, up 23.6% year on year, outperforming analysts’ expectations by 4.9%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ revenue estimates.

However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $13.67.

Is now the time to buy Ellington Financial? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q2: WaFd Bank (NASDAQ: WAFD)

Founded in 1917 and rebranded from Washington Federal in 2023, WaFd (NASDAQ: WAFD) is a bank holding company that provides lending, deposit services, and insurance through its Washington Federal Bank subsidiary across eight western states.

WaFd Bank reported revenues of $187.2 million, flat year on year, falling short of analysts’ expectations by 2%. It was a disappointing quarter as it posted a significant miss of analysts’ net interest income estimates and a significant miss of analysts’ EPS estimates.

Interestingly, the stock is up 16.1% since the results and currently trades at $32.30.

Read our full analysis of WaFd Bank’s results here.

PennyMac Financial Services (NYSE: PFSI)

Founded during the 2008 financial crisis to help address the mortgage market meltdown, PennyMac Financial Services (NYSE: PFSI) is a specialty financial services company that originates, services, and manages investments related to residential mortgage loans in the United States.

PennyMac Financial Services reported revenues of $637.1 million, up 11.3% year on year. This print beat analysts’ expectations by 10.7%. Overall, it was an exceptional quarter as it also put up an impressive beat of analysts’ net interest income estimates and a solid beat of analysts’ revenue estimates.

The stock is up 10.7% since reporting and currently trades at $133.88.

Arbor Realty Trust (NYSE: ABR)

With roots dating back to 2003 and a focus on the stability of multifamily housing, Arbor Realty Trust (NYSE: ABR) is a specialized lender that provides financing solutions for multifamily and commercial real estate while also originating and servicing government-backed mortgage loans.

Arbor Realty Trust reported revenues of $112.4 million, down 28.2% year on year. This number came in 25.8% below analysts' expectations. Aside from that, it was a mixed quarter as it also logged a beat of analysts’ EPS estimates but a significant miss of analysts’ revenue estimates.

Arbor Realty Trust had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is down 21.5% since reporting and currently trades at $9.07.

Read our full, actionable report on Arbor Realty Trust here, it’s free for active Edge members.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.