GEORGE TOWN, Grand Cayman, Aug. 14, 2024 (GLOBE NEWSWIRE) -- StoneCo Ltd. (Nasdaq: STNE, B3: STOC31) (“Stone” or the “Company”) today reports its financial results for its second quarter ended June 30, 2024.

| Adjusted EBT | MSMB CTPV (Card TPV) |

| R$652 million | R$97.8 billion |

| +45.9% year over year | +17.4% year over year |

| Adjusted Net income | Adjusted Basic EPS |

| R$497 million | R$1.61 |

| +54.4% year over year | +57.2% year over year |

Business Overview

Stone has made significant progress in the second quarter across our strategic priorities, advancing in critical areas as we work towards our 2024 and long-term targets.

Highlighting our strong growth within Financial Services, MSMB Card TPV increased by 17.4% year-over-year, representing continued market share gains within the segment. This growth was achieved with continued focus towards strong monetization, as shown by our MSMB take rates, which increased 7 basis points, reaching 2.54% in the 2Q24.

In banking, we continued to drive engagement, reaching 2.7 million active banking clients and R$ 6.5 billion in deposits. As we continue to evolve in our banking solution, we have also started to pilot interest-bearing products, such as time deposits – which is an exciting development to further help our clients with their most critical needs.

Our credit portfolio also continues to grow, reaching R$ 712 million in the quarter with strong quality, as shown by our working capital NPLs over 90 days still at 2.6% - very much in line with our expectations. On the product side, we have finalized the structuring of our Giro Fácil product, a short-term overdraft solution designed to address the immediate capital requirements of our clients.

In software, our initiative to cross-sell financial services to software clients continues to progress well, particularly in the gas station and retail verticals. This effort has led to stronger card TPV growth among software clients in priority verticals compared to the overall MSMB card TPV growth.

We have also maintained our focus on efficiency. Administrative expenses have decreased by 13% year-over-year, resulting in a 180 basis-point reduction as a percentage of revenues when compared to the 2Q23.

As a result of these positive developments, our adjusted basic EPS demonstrated strong growth, reaching R$1.61. We remain committed to our business plan and the targets established during our Investor Day.

In light of this commitment and considering short-term market fluctuations, we allocated capital to repurchase an additional 9.67 million shares, totaling R$724 million during the beginning of 3Q24, bringing us closer to completing the R$1 billion share repurchase program announced in November 2023. Additionally, as part of our liability management strategy, we allocated $295 million to the tender offer for our 2028 bonds, achieving nearly 60% participation.

Operating and Financial Highlights for 2Q24

MAIN CONSOLIDATED ADJUSTED FINANCIAL METRICS

Table 1: Main Consolidated Financial Metrics

| Main Consolidated Financial Metrics (R$mn) | 2Q24 | 1Q24 | Δ q/q % | 2Q23 | Δ y/y % | 1H24 | 1H23 | y/y % |

| Total Revenue and Income | 3,205.9 | 3,084.9 | 3.9% | 2,954.8 | 8.5% | 6,290.8 | 5,666.4 | 11.0% |

| Adjusted EBITDA | 1,587.2 | 1,512.0 | 5.0% | 1,498.8 | 5.9% | 3,099.2 | 2,750.2 | 12.7% |

| Adjusted EBITDA margin (%) | 49.5% | 49.0% | 0.5 p.p. | 50.7% | (1.2 p.p.) | 49.3% | 48.5% | 0.7 p.p. |

| Adjusted EBT | 652.2 | 567.6 | 14.9% | 447.0 | 45.9% | 1,219.8 | 771.0 | 58.2% |

| Adjusted EBT margin (%) | 20.3% | 18.4% | 1.9 p.p. | 15.1% | 5.2 p.p. | 19.4% | 13.6% | 5.8 p.p. |

| Adjusted Net Income | 497.1 | 450.4 | 10.4% | 322.0 | 54.4% | 947.6 | 558.6 | 69.6% |

| Adjusted Net income margin (%) | 15.5% | 14.6% | 0.9 p.p. | 10.9% | 4.6 p.p. | 15.1% | 9.9% | 5.2 p.p. |

| Adjusted Net Cash | 5,256.9 | 5,139.8 | 2.3% | 4,327.2 | 21.5% | 5,256.9 | 4,327.2 | 21.5% |

- Total Revenue and Income reached R$3,205.9 million in the quarter, up 8.5% year over year. This growth was mostly driven by a 10.6% increase in financial services revenues, mainly as a result of consistent active client base growth and higher client monetization.

- Adjusted EBITDA was R$1,587.2 million in the quarter, an increase of 5.9% year over year and 5.0% quarter over quarter. Adjusted EBITDA Margin increased from 49.0% to 49.5% sequentially, primarily due to consolidated revenue growth, combined with lower selling expenses as a percentage of revenues.

- Adjusted EBT was R$652.2 million in 2Q24, a 45.9% increase year over year, with an adjusted EBT margin of 20.3%, a 5.2 percentage points increase over the same period. Adjusted EBT was up 14.9% sequentially, with adjusted EBT margin increasing 1.9 percentage point. The quarter over quarter margin increase is primarily attributed to consolidated revenue growth, combined with lower financial and selling expenses as percentage of revenues, being partially offset by more normalized levels of other operating expenses.

- Adjusted Net Income reached R$497.1 million in 2Q24, a 54.4% growth year over year, with an adjusted net margin of 15.5% compared with R$450.4 million and a margin of 14.6% in 1Q24. The sequential margin increase was primarily driven by the same factors that impacted Adjusted EBT margin, partially compensated by a higher effective tax rate.

- Adjusted Net Cash position was R$5,256.9 million in 2Q24, representing a 21.5% increase year over year or 2.3% sequentially. The R$117.1 million quarter over quarter growth is mainly explained by cash generation from our operations with the main outflows being capex and buyback of shares.

OUTLOOK

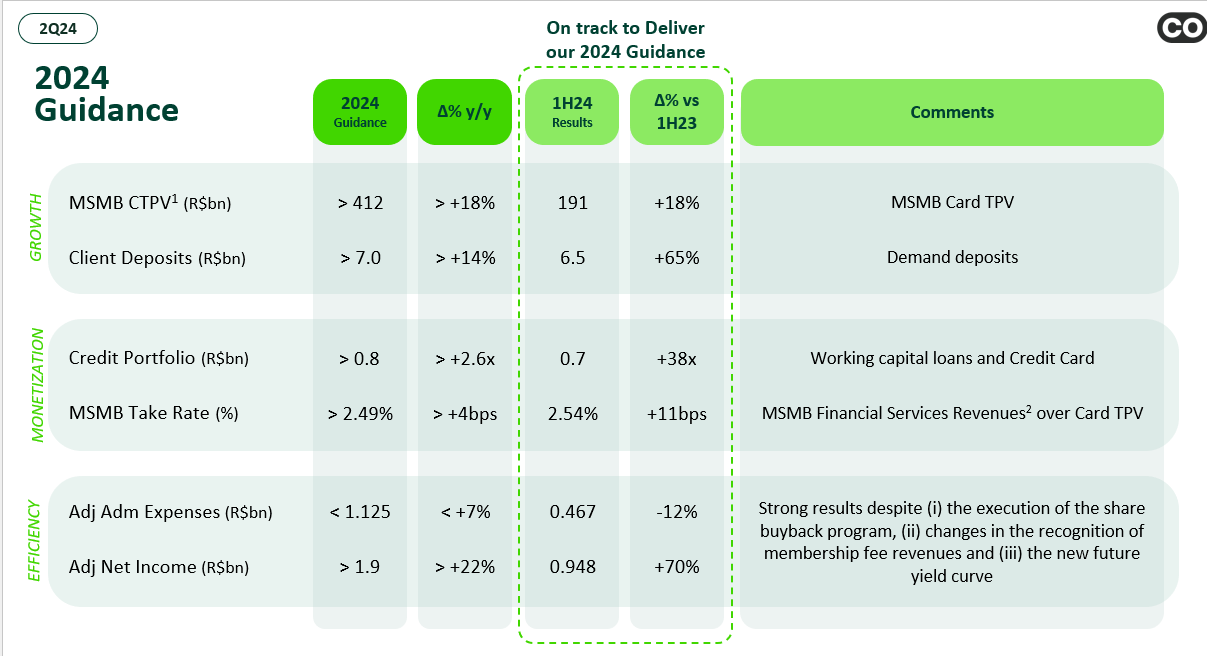

We are on track to deliver our 2024 guidance. The profitability achieved in 1H24 has positioned us favorably to meet our full-year guidance, despite several headwinds. These include a ~R$120 million reduction in revenues in 1H24 alone due to changes in the recognition of membership fee revenues and a challenging macroeconomic environment with a higher yield curve.

| On track to deliver our 2024 Guidance | |||||||||

| 2024 Guidance | 2024 Guidance | ∆% y/y | 1H24 | ∆% vs 1H23 | Comments | ||||

| MSMB CTPV (Card TPV) (R$bn) | > 412 | > +18% | 191 | +18% | MSMB Card TPV | ||||

| Clients Deposits (R$bn) | > 7.0 | > +14% | 6.5 | 65% | Demand deposits | ||||

| Growth ↑ | |||||||||

| Credit Portfolio (R$bn) | > 0.8 | > +2.6x | 0.7 | +38x | Working capital loans and Credit Card | ||||

| MSMB Take Rate (%) | > 2.49% | > +4bps | 2.54% | +15bps | MSMB Financial Services Revenues over Card TPV | ||||

| Monetization ↑ | |||||||||

| Adjusted Administrative Expenses (R$bn) | < 1.125 | < +7% | 0.948 | -12% | Strong results despite (i) the execution of the share buyback program, (ii) changes in the recognition of the membership fee revenues and (iii) the new future yield curve | ||||

| Adjusted Net Income (R$bn) | > 1.9 | > +22% | 0.467 | +70% | |||||

| Efficiency ↑ | |||||||||

MAIN OPERATING METRICS

Table 2: Payments

| Payments Operating Metrics | 2Q24 | 1Q24 | Δ q/q % | 2Q23 | Δ y/y % |

| Total TPV1 (R$bn) | 126.1 | 117.3 | 7.5% | 103.7 | 21.6% |

| CTPV2 (Card TPV) | 110.9 | 105.8 | 4.8% | 97.4 | 13.8% |

| PIX QR Code | 15.2 | 11.5 | 32.1% | 6.3 | 141.5% |

| MSMB TPV1 | 109.3 | 101.9 | 7.2% | 87.7 | 24.6% |

| CTPV2 (Card TPV) | 97.8 | 93.4 | 4.7% | 83.3 | 17.4% |

| PIX QR Code | 11.5 | 8.5 | 34.8% | 4.3 | 164.5% |

| Key Accounts TPV1 | 16.8 | 15.3 | 9.7% | 16.0 | 4.8% |

| CTPV2 (Card TPV) | 13.1 | 12.3 | 6.0% | 14.1 | (7.2%) |

| PIX QR Code | 3.8 | 3.0 | 24.6% | 2.0 | 90.7% |

| Active Client Base ('000) | 3,904.1 | 3,720.6 | 4.9% | 3,014.7 | 29.5% |

| MSMB | 3,860.2 | 3,676.2 | 5.0% | 2,962.0 | 30.3% |

| Key Accounts | 51.8 | 51.9 | (0.2%) | 62.6 | (17.2%) |

| Net Adds ('000) | 183.6 | 198.5 | (7.5%) | 196.6 | (6.6%) |

| MSMB | 184.0 | 204.9 | (10.2%) | 203.9 | (9.8%) |

| Key Accounts | (0.1) | (6.4) | (98.4%) | (5.0) | (97.9%) |

- Total TPV (including PIX QR Code) reached R$126.1 billion in 2Q24, 21.6% higher on a year over year basis. This growth is mainly explained by (i) continuous growth in the MSMB segment, with CTPV (Card TPV) growing 17.4% and (ii) the increase in PIX QR Code volumes which grew 141.5% compared with the prior-year period.

- Total Payments Active Client base reached 3.9 million with a net addition of 183,600 active clients in the quarter.

MSMB (Micro and SMB clients)

- MSMB Active Payment Clients were 3.9 million in 2Q24, growing 30.3% year over year. The quarterly net addition was 184,000, a 10.2% quarter over quarter decrease, which can be mainly attributed to higher net adds in 1Q24 due to a specific marketing campaign in that period.

- MSMB TPV (including PIX QR Code) was R$109.3 billion in the quarter, an year over year increase of 24.6% and 7.2% sequentially.

- MSMB CTPV (Card TPV) was R$97.8 billion, growing 17.4% year over year and 4.7% sequentially. The year over year increase was primarily driven by the continuous growth of our active payments client base in the segment.

- MSMB PIX QR Code reached R$11.5 billion in the quarter, 1.6x higher year over year or a 34.8% growth over the previous quarter. From 2Q24 onwards, MSMB PIX QR Code volumes will include those from Pagar.me SMB clients, who are now fully integrated into the complete Stone banking solution, which contributed with R$1.4 billion in the quarter.

________________________

1 TPV means “Total Payment Volume”. Considers all volumes settled by StoneCo, including PIX QR Code),defined as transactions from dynamic POS QR Code and static QR Code, unless otherwise noted.

2 CTPV means “Card Total Payments Volume” and considers only card volumes settled by the Company.

Table 3: Banking

| Banking Operating Metrics | 2Q24 | 1Q24 | Δ q/q % | 2Q23 | Δ y/y % |

| MSMB Active Client Base ('000) | 2,704.2 | 2,379.7 | 13.6% | 1,672.0 | 61.7% |

| Client Deposits (R$mn) | 6,471.6 | 5,985.0 | 8.1% | 3,918.6 | 65.2% |

| MSMB ARPAC (R$) | 25.7 | 29.3 | (12.6%) | 25.3 | 1.2% |

- Banking solutions

- Banking active client base in 1Q24 was 2.7 million active clients, up 61.7% year over year or 13.6% quarter over quarter. The sequential growth was mainly a result of (i) the increase of our payments active client base, (ii) the continued activation of new banking accounts within our existing Stone payments client base, in line with the execution of our strategy of selling integrated solutions, and (iii) the migration of Pagar.me clients to the full banking solution.

- Total deposits achieved R$6.5 billion in the quarter, increasing 65.2% year over year and 8.1% quarter over quarter. The sequential increase is mainly attributed to the growth in our banking active client base.

- Banking ARPAC was R$25.7 per client per month, representing a 1.2% increase year over year and a 12.6% decrease quarter over quarter. The quarter over quarter decrease is mainly explained by (i) a lower average CDI in the period which impacts our floating revenues and (ii) higher contribution of Ton clients in the MSMB Active Banking Client Base, as Ton clients generate lower revenue contribution compared to Stone clients.

- Banking active client base in 1Q24 was 2.7 million active clients, up 61.7% year over year or 13.6% quarter over quarter. The sequential growth was mainly a result of (i) the increase of our payments active client base, (ii) the continued activation of new banking accounts within our existing Stone payments client base, in line with the execution of our strategy of selling integrated solutions, and (iii) the migration of Pagar.me clients to the full banking solution.

Table 4: Credit

| Credit Metrics | 2Q24 | 1Q24 | Δ q/q % | 2Q23 | Δ y/y % |

| Consolidated credit metrics | |||||

| Portfolio (R$mn) | 711.8 | 539.6 | 31.9% | 18.7 | 3704.1% |

| Provisions for losses (R$mn) | (18.1) | (44.8) | (59.7%) | (3.7) | 382.9% |

| Working capital loans metrics | |||||

| Active contracts | 24,264 | 18,754 | 29.4% | 672 | 3510.7% |

| Portfolio (R$mn) | 681.6 | 531.7 | 28.2% | 18.7 | 3542.7% |

| Disbursements (R$mn) | 275.6 | 294.9 | (6.6%) | 19.0 | 1350.8% |

| Provision for losses (R$mn) | (16.9) | (44.4) | (62.0%) | (3.7) | 350.6% |

| Accumulated provision for losses (R$mn) | (123.1) | (106.3) | 15.9% | (3.7) | 3186.8% |

| Provisions ratio | (18.1%) | (20.0%) | 1.92 p.p. | (20.0%) | 1.96 p.p. |

| NPL 15-90 days | 2.85% | 2.20% | 0.66 p.p. | 0.31% | 2.55 p.p. |

| NPL > 90 days | 2.60% | 1.47% | 1.13 p.p. | n.a. | n.a. |

- Working Capital loans:

- In 2Q24 we disbursed R$275.6 million, reaching 24,264 contracts and a portfolio of R$681.6 million at month-end. The Company remains focused on offering this credit solution to the SMB client segment.

- Provision for expected working capital losses was R$16.9 million in the quarter compared with R$44.4 million in the previous quarter. We have started to converge provision levels to our expected loss levels as the portfolio matures. As a result, the ratio of accumulated loan loss provision expenses over the working capital portfolio was 18.1% in the period compared with 20.0% in previous quarters.

- Working capital NPL 15-90 days was 2.85% and NPL over 90 days was 2.60% in 2Q24 compared with 2.20% and 1.47% in 1Q24 respectively. This expected increase is a natural result of the portfolio maturation process.

Table 5: Monetization

| Take Rate | 2Q24 | 1Q24 | Δ q/q % | 2Q23 | Δ y/y % |

| MSMB | 2.54% | 2.54% | 0.01 p.p. | 2.48% | 0.07 p.p. |

| Key Accounts | 1.33% | 1.29% | 0.04 p.p. | 1.14% | 0.19 p.p. |

- MSMB Take Rate was flat sequentially in 2Q24 at 2.54%. For more information about reconciling our reported take rates with our financial services revenue, please refer to the “Build-up Take Rate” tab in our Results Spreadsheet.

Table 6: Software

| Software Operating Metrics (R$bn) | 2Q24 | 1Q24 | Δ q/q % | 2Q23 | Δ y/y % |

| CTPV3 (Card TPV) Overlap | 5.5 | 5.1 | 8.2% | n.a. | n.a. |

- CTPV (Card TPV) Overlap is measured by the MSMB CTPV overlap between financial services and the priority verticals, being a key metric to measure our cross sell performance. In 2Q24, CTPV Overlap was R$5.5 billion, representing an 8.2% increase on a quarter over quarter basis, higher than MSMB CPTV growth of 4.7% over the same period. This growth can be mainly attributed to the Gas Station and Retail verticals, which are the ones we are mostly focused on at the moment.

Income Statement

Table 7: Statement of Profit or Loss (IFRS, as Reported)

| Statement of Profit or Loss (R$mn) | 2Q24 | % Rev. | 1Q24 | % Rev. | Δ q/q % | 2Q23 | % Rev. | Δ y/y% |

| Net revenue from transaction activities and other services | 807.5 | 25.2% | 749.8 | 24.3% | 7.7% | 840.1 | 28.4% | (3.9%) |

| Net revenue from subscription services and equipment rental | 453.3 | 14.1% | 456.7 | 14.8% | (0.8%) | 457.3 | 15.5% | (0.9%) |

| Financial income | 1,826.7 | 57.0% | 1,741.1 | 56.4% | 4.9% | 1,462.6 | 49.5% | 24.9% |

| Other financial income | 118.4 | 3.7% | 137.3 | 4.4% | (13.7%) | 194.8 | 6.6% | (39.2%) |

| Total revenue and income | 3,205.9 | 100.0% | 3,084.9 | 100.0% | 3.9% | 2,954.8 | 100.0% | 8.5% |

| Cost of services | (841.4) | (26.2%) | (809.9) | (26.3%) | 3.9% | (685.3) | (23.2%) | 22.8% |

| Provision for expected credit losses4 | (18.1) | (0.6%) | (44.8) | (1.5%) | (59.7%) | 0.0 | 0.0% | n.a. |

| Administrative expenses | (255.5) | (8.0%) | (257.0) | (8.3%) | (0.6%) | (303.9) | (10.3%) | (15.9%) |

| Selling expenses | (524.9) | (16.4%) | (529.7) | (17.2%) | (0.9%) | (411.9) | (13.9%) | 27.4% |

| Financial expenses, net | (851.1) | (26.5%) | (896.5) | (29.1%) | (5.1%) | (1,073.8) | (36.3%) | (20.7%) |

| Mark-to-market on equity securities designated at FVPL | 0.0 | 0.0% | 0.0 | 0.0% | n.a. | 0.0 | 0.0% | n.a. |

| Other income (expenses), net | (80.9) | (2.5%) | (108.1) | (3.5%) | (25.1%) | (56.7) | (1.9%) | 42.6% |

| Loss on investment in associates | (0.4) | (0.0%) | 0.3 | 0.0% | n.m. | (0.8) | (0.0%) | (48.7%) |

| Profit (loss) before income taxes | 651.7 | 20.3% | 484.0 | 15.7% | 34.6% | 422.3 | 14.3% | 54.3% |

| Income tax and social contribution | (153.4) | (4.8%) | (110.4) | (3.6%) | 38.9% | (115.1) | (3.9%) | 33.3% |

| Net income (loss) for the period | 498.3 | 15.5% | 373.6 | 12.1% | 33.4% | 307.2 | 10.4% | 62.2% |

________________________

3 CTPV means “Card Total Payments Volume” and considers only card volumes settled by the Company.

4 In 2Q23, credit revenues were recognized net of provision for expected credit losses in Financial Income. From 3Q23 onwards, provision for expected losses is allocated in Cost of services.

Total Revenue and Income

Net Revenue from Transaction Activities and Other Services

Net Revenue from Transaction Activities and Other Services was R$807.5 million in 2Q24, a 3.9% decrease year over year. This decrease can be explained by (i) the change in our internal accounting methodology of recognition of membership fee revenues, which since 1Q24 has been deferred through the expected lifetime of clients instead of upfront upon the signing of the service agreement contract, as well as (ii) lower transactional software revenues, which are mainly related to our software’s Enterprise clients, and are being deemphasized. These effects were partially offset by the growth of our acquiring and banking transactional revenues, with total TPV (including PIX QR Code) growing 21.6% year over year.

In 2Q24, considering our new internal accounting methodology, membership fees contributed with R$25.2 million to our transaction activities and other services revenue, compared with R$78.7 million in 2Q23, which considered our previous methodology.

Quarter over quarter, Net Revenue from Transaction Activities and Other Services increased 7.7% mainly due to (i) the growth in our acquiring and banking transactional revenues, with TPV (including PIX QR Code) growing 7.5% quarter over quarter, combined with (ii) higher membership fee revenues, which increased from R$10.3 million in 1Q24 to R$25.2 million in 2Q24, as a result of active client base growth and the new internal accounting methodology for membership fee revenue recognition.

Net Revenue from Subscription Services and Equipment Rental

Net Revenue from Subscription Services and Equipment Rental decreased 0.9% year over year to R$453.3 million in 2Q24. This can be primarily attributed to the divestment of assets, namely Creditinfo (4Q23) and PinPag (1Q24), which were in the “non-allocated” business segment. Disregarding this effect, net revenue from subscription services and equipment rental would have increased 2.6%, mainly as a result of higher subscription software revenues in the period. Quarter over quarter, this revenue line decreased 0.8%, mainly attributed to the same items aforementioned for the year over year variation.

Financial Income

Financial Income was R$1,826.7 million in the quarter, a 24.9% year over year growth, explained by (i) higher prepayment revenues, mostly due to an increase in prepaid volumes, (ii) higher credit revenues, which grew from R$3.9 million in 2Q23 to R$50.6 million in 2Q24 and (iii) higher floating revenues from our banking solution.

Quarter over quarter, financial income increased 4.9% as a result of items (i) and (ii) from the aforementioned explanation for the year over year comparison. Credit revenues increased from R$33.9 million in 1Q24 to R$50.6 million in 2Q24.

Other Financial Income

Other Financial Income was R$118.4 million in 2Q24 compared with R$194.8 million in 2Q23 primarily due to a (i) lower average cash balance, combined with (ii) a reduction in the Brazilian base rate in the period. Compared with the previous quarter, Other Financial Income decreased 13.7% due to item (ii) from the aforementioned explanation for the year over year comparison.

Costs and Expenses

Cost of Services

Cost of Services were R$841.4 million in 2Q24, 22.8% higher year over year. This increase can be primarily attributed to (i) higher provisions for losses, including R$18.1 million of provisions for loan losses related to our credit product in the quarter, which were inexistent in 2Q23, (ii) higher investments in technology, and (iii) higher transaction, logistics and D&A costs as we continue to expand our business. As a percentage of revenues, Cost of Services was 26.2%, up from 23.2% in 2Q23.

Compared with 1Q24, Cost of Services were 3.9% higher, mainly as a result of higher provisions for losses in acquiring and banking, which more than compensated lower provisions for loan losses related to our credit product, as well as item (iii) abovementioned for the year over year explanation.

Provisions for loan losses from our credit product contributed with R$18.1 million to our Cost of Services in the quarter, compared with R$44.8 million in 1Q24. This decrease is a result of the convergence of our working capital provision levels to our expected loss levels as the portfolio matures, with working capital provisions now representing 18% of the respective portfolio, down from 20% in previous quarters. As a percentage of revenues, Cost of Services decreased slightly from 26.3% in 1Q24 to 26.2% in 2Q24.

Administrative Expenses

Administrative Expenses were R$255.5 million, representing a 15.9% decrease year over year, mainly explained by (i) more normalized levels of provisions for variable compensation, as in 2Q23 we went through changes in the allocation of these provisions between our costs and expenses lines, which increased Administrative Expenses in that quarter, (ii) lower amortization of fair value adjustments from acquisitions, (iii) lower personnel expenses in Software after a reduction in headcount executed in 2Q23, and (iv) changes in the allocation between costs and expenses lines from the Software segment in 3Q23, affecting year over year comparability. As a percentage of revenues, Administrative Expenses decreased from 10.3% in 2Q23 to 8.0% in 2Q24.

Compared with the previous quarter, Administrative Expenses were slightly lower. The 0.6% reduction can be explained mostly by (i) lower amortization of fair value adjustments from acquisitions, (ii) efficiency gains in personnel expenses in the Software segment, and (iii) the divestment of PinPag in 1Q24, which was in the “non-allocated” business segment. These effects were partially offset by higher overall third party services expenses. As a percentage of revenues, Administrative Expenses decreased from 8.3% in 1Q24 to 8.0% in 2Q24.

Selling Expenses

Selling Expenses were R$524.9 million in 2Q24, up 27.4% year over year, primarily explained by higher investments in (i) our salespeople, (ii) marketing, and (iii) partner commissions. As a percentage of revenues, Selling Expenses were 16.4% compared with 13.9% in 2Q23.

Compared with 1Q24, Selling Expenses decreased 0.9%. This slight reduction was due to lower marketing expenses, mainly as a result of reduced expenses with the sponsorship of a reality television show, which contributed R$30.2 million to our Selling Expenses in the quarter, compared with R$56.7 million in 1Q24. This decrease was partially offset by higher investments in sales teams. As a percentage of revenues, Selling Expenses decreased sequentially from 17.2% in 1Q24 to 16.4% in 2Q24.

Financial Expenses, Net

Financial Expenses, Net were R$851.1 million in 2Q24, a 20.7% decrease compared with the prior-year period. This decrease can be mainly attributed to (i) a reduction in average CDI, from 13.65% in 2Q23 to 10.51% in 2Q24, combined with (ii) our decision to reinvest our cash generation towards the funding of our operation. These effects were partially offset by higher funding needs for our prepayment and credit operations in the period. As a percentage of Total Revenue and Income, Financial Expenses, Net decreased from 36.3% in 2Q23 to 26.5% in 2Q24.

Compared with 1Q24, Financial Expenses, Net were 5.1% lower. This decrease was driven by (i) lower average CDI in the period, which reduced from 11.29% in 1Q24 to 10.51% in 2Q24, (ii) reduction in our average funding spreads, and (iii) our decision to reinvest our cash generation towards the funding of our operation. These effects were partially offset by (iv) higher funding needs in our prepayment and credit operations and (v) a higher number of working days in the quarter. As a percentage of revenues, Financial Expenses, net decreased from 29.1% in the previous quarter to 26.5% in 2Q24.

Other Income (Expenses), Net

Other Expenses, Net were R$80.9 million in the quarter, representing an increase of R$24.2 million on a year over year basis. This increase is mainly explained by (i) higher share-based compensation expenses, as in 2Q23 we had lower tax provisions, combined with (ii) higher contingencies expenses in the period.

Compared with the previous quarter, Other Expenses, net were R$27.1 million lower. This decrease is mostly attributed to (i) the divestment of PinPag in 1Q24 in the amount of R$52.9 million, which did not impact again this quarter, and (ii) lower contingencies expenses, being partially offset by (iii) normalized levels of share based compensation expenses, as 1Q24 included a non-recurring positive impact of R$40.5 million from the net effect of the cancellation and new grants of incentive plans.

Income Tax and Social Contribution

The Company recognized R$153.4 million of income tax and social contribution expenses during 2Q24 over a profit before income taxes of R$651.7 million, implying an effective tax rate of 23.5% in the quarter. The difference to the statutory rate is mainly explained by gains from subsidiaries abroad subject to different statutory tax rates.

Net Income (Loss) and EPS

In 2Q24 Net Income was R$498.3 million, representing a 62.2% year over year growth compared with R$307.2 million in 2Q23. This was mostly a result of higher Total Revenue and Income combined with lower Financial Expenses. These effects were partially offset by higher Cost of Services and Selling Expenses.

IFRS basic EPS was R$1.61 per share in 2Q24, compared with R$0.98 in 2Q23.

Adjustments to Net Income by P&L Line

Table 8: Adjustments to Net Income by P&L Line

| Adjustments to Net Income by P&L line (R$mn) | 2Q24 | 1Q24 | 2Q23 |

| Cost of services | 0.0 | 0.0 | 0.0 |

| Administrative expenses | 20.3 | 25.0 | 34.8 |

| Selling expenses | 0.0 | 0.0 | 0.0 |

| Financial expenses, net | 1.5 | 7.3 | 14.2 |

| Other operating income (expense), net | (21.3) | 51.3 | (24.2) |

| Gain (loss) on investment in associates | 0.0 | 0.0 | 0.0 |

| Profit (loss) before income taxes | 0.5 | 83.6 | 24.7 |

| Income tax and social contribution | (1.6) | (6.8) | (10.0) |

| Net income (loss) for the period | (1.2) | 76.8 | 14.8 |

Below we comment the adjustments in our P&L in the quarter:

- Administrative Expenses include -R$20.3 million related to amortization of fair value adjustments on acquisitions, mostly related to the Linx and other software companies’ acquisitions.

- Financial Expenses include -R$1.5 million of expenses related to effects from (i) earn out interests on business combinations, and (ii) financial expenses from fair value adjustments on acquisitions.

- Other Expenses, net include R$21.3 million from fair value of call options related to acquisitions, earn-out interests, divestment of assets and fair value adjustments on acquisitions.

- Income Tax and Social Contribution includes R$1.6 million related to taxes from the adjusted items. Adjusting for those effects, our Income Tax and Social Contribution was R$155.0 million with an effective tax rate in 2Q24 of 23.8%.

Considering the adjustments to net income abovementioned, our Adjusted Profit and Loss Statement is presented below:

Table 9: Statement of Profit or Loss (Adjusted)

| Adjusted Statement of Profit or Loss (R$mn) | 2Q24 | % Rev. | 1Q24 | % Rev. | Δ q/q % | 2Q23 | % Rev. | Δ y/y% |

| Net revenue from transaction activities and other services | 807.5 | 25.2% | 749.8 | 24.3% | 7.7% | 840.1 | 28.4% | (3.9%) |

| Net revenue from subscription services and equipment rental | 453.3 | 14.1% | 456.7 | 14.8% | (0.8%) | 457.3 | 15.5% | (0.9%) |

| Financial income | 1,826.7 | 57.0% | 1,741.1 | 56.4% | 4.9% | 1,462.6 | 49.5% | 24.9% |

| Other financial income | 118.4 | 3.7% | 137.3 | 4.4% | (13.7%) | 194.8 | 6.6% | (39.2%) |

| Total revenue and income | 3,205.9 | 100.0% | 3,084.9 | 100.0% | 3.9% | 2,954.8 | 100.0% | 8.5% |

| Cost of services | (841.4) | (26.2%) | (809.9) | (26.3%) | 3.9% | (685.3) | (23.2%) | 22.8% |

| Provision for expected credit losses4 | (18.1) | (0.6%) | (44.8) | (1.5%) | (59.7%) | 0.0 | 0.0% | n.a. |

| Administrative expenses | (235.2) | (7.3%) | (232.0) | (7.5%) | 1.4% | (269.1) | (9.1%) | (12.6%) |

| Selling expenses | (524.9) | (16.4%) | (529.7) | (17.2%) | (0.9%) | (411.9) | (13.9%) | 27.4% |

| Financial expenses, net | (849.5) | (26.5%) | (889.2) | (28.8%) | (4.5%) | (1,059.7) | (35.9%) | (19.8%) |

| Other income (expenses), net | (102.3) | (3.2%) | (56.7) | (1.8%) | 80.2% | (81.0) | (2.7%) | 26.3% |

| Loss on investment in associates | (0.4) | (0.0%) | 0.3 | 0.0% | n.m | (0.8) | (0.0%) | (48.7%) |

| Adj. Profit before income taxes | 652.2 | 20.3% | 567.6 | 18.4% | 14.9% | 447.0 | 15.1% | 45.9% |

| Income tax and social contribution | (155.0) | (4.8%) | (117.2) | (3.8%) | 32.3% | (125.0) | (4.2%) | 24.0% |

| Adjusted Net Income | 497.1 | 15.5% | 450.4 | 14.6% | 10.4% | 322.0 | 10.9% | 54.4% |

For the P&L lines that are adjusted, the variations can be explained by the same factors as in the IFRS statement apart from the ones mentioned below.

Adjusted Administrative expenses decreased 12.6% year over year, mainly due to (i) more normalized levels of provisions for variable compensation, as in 2Q23 we went through changes in the allocation of provisions for variable compensation between our costs and expenses lines, which increased Administrative Expenses in that quarter, (ii) lower personnel expenses in Software after a reduction in headcount executed in 2Q23, and (iii) changes in the allocation between costs and expenses lines from the Software segment in 3Q23, affecting year over year comparability. The quarter over quarter variation can be explained by (i) efficiency gains in personnel expenses in the Software segment, and (ii) the divestment of PinPag in 1Q24, which was in the “non-allocated” business segment. These effects were partially offset by higher overall third party services expenses.

Adjusted other expenses, net increased 26.3% year over year. This increase can be mainly explained by higher share-based compensation expenses, as in 2Q23 we had lower tax provisions, as well as higher contingencies expenses in the period. Quarter over quarter, other expenses, net increased 80.2% mainly as a result of a non-recurring positive effect of R$40.5 million in our share-based compensation expenses in 1Q24.

Adjusted Net Income (Loss) and EPS

Table 10: Adjusted Net Income Reconciliation

| Net Income Bridge (R$mn) | 2Q24 | % Rev. | 1Q24 | % Rev. | Δ q/q% | 2Q23 | % Rev. | Δ y/y% |

| Net income (loss) for the period | 498.3 | 15.5% | 373.6 | 12.1% | 33.4% | 307.2 | 10.4% | 62.2% |

| Amortization of fair value adjustment (a) | 13.4 | 0.4% | 12.3 | 0.4% | 9.1% | 35.7 | 1.2% | (62.5%) |

| Other expenses (b) | (12.9) | (0.4%) | 71.3 | 2.3% | n.m | (11.0) | (0.4%) | 17.8% |

| Tax effect on adjustments | (1.6) | (0.1%) | (6.8) | (0.2%) | (76.0%) | (10.0) | (0.3%) | (83.7%) |

| Adjusted net income (as reported) | 497.1 | 15.5% | 450.4 | 14.6% | 10.4% | 322.0 | 10.9% | 54.4% |

| Basic Number of shares | 307.8 | n.a. | 309.1 | n.a. | (0.4%) | 313.1 | n.a. | (1.7%) |

| Diluted Number of shares | 314.8 | n.a. | 316.1 | n.a. | (0.4%) | 318.7 | n.a. | (1.2%) |

| Adjusted basic EPS (R$) (c) | 1.61 | n.a. | 1.46 | n.a. | 10.5% | 1.02 | n.a. | 57.2% |

(a) Related to acquisitions. Consists of expenses resulting from the changes of the fair value adjustments as a result of the application of the acquisition method.

(b) Consists of the fair value adjustment related to associates call option, earn-out and earn-out interests related to acquisitions, loss of control of subsidiary and divestment of assets.

(c) Calculated as Adjusted Net income attributable to owners of the parent (Adjusted Net Income reduced by Adjusted Net Income attributable to Non-Controlling interest) divided by basic number of shares.

Adjusted Net Income was R$497.1 million in the quarter with a margin of 15.5%, compared with R$322.0 million in 2Q23 and a margin of 10.9%. The year-over-year increase in Adjusted Net Income margin can be primarily attributed to (i) a 24.3% year over year growth in total revenue and income net of adjusted Financial Expenses, combined with (ii) lower adjusted Administrative Expenses, net (down 12.6% year over year). These effects were partially offset by higher Cost of Services (up 22.8% year over year) and higher Selling Expenses (up 27.4% year over year).

Adjusted Net Income was 10.4% higher compared with the previous quarter and Adjusted Net Margin increased 0.9 percentage point from 14.6% in 1Q24 to 15.5% in 2Q24, mainly due to (i) consolidated revenue growth, combined with (ii) lower Financial and Selling Expenses as a percentage of revenues. These effects were partially offset by higher Other Operating Expenses as a percentage of revenues and a higher effective tax rate in the period.

Adjusted basic EPS was R$1.61 per share in 2Q24 compared with R$1.02 per share in 2Q23 and R$1.46 per share in 1Q24, on a comparable basis.

EBITDA

EBITDA was R$1,608.5 million in 2Q24, 5.6% higher than R$1,523.0 million in 2Q23, mostly as a result of the increase in Total Revenue and Income, excluding Other Financial Income. These effects were partially offset by higher Cost of Services and Selling Expenses, excluding D&A.

Table 11: Adjusted EBITDA Reconciliation

| EBITDA Bridge (R$mn) | 2Q24 | % Rev. | 1Q24 | % Rev. | Δ q/q % | 2Q23 | % Rev. | Δ y/y% |

| Profit (Loss) before income taxes | 651.7 | 20.3% | 484.0 | 15.7% | 34.6% | 422.3 | 14.3% | 54.3% |

| (+) Financial expenses, net | 851.1 | 26.5% | 896.5 | 29.1% | (5.1%) | 1,073.8 | 36.3% | (20.7%) |

| (-) Other financial income | (118.4) | (3.7%) | (137.3) | (4.4%) | (13.7%) | (194.8) | (6.6%) | (39.2%) |

| (+) Depreciation and amortization | 224.2 | 7.0% | 217.3 | 7.0% | 3.2% | 221.7 | 7.5% | 1.1% |

| EBITDA | 1,608.5 | 50.2% | 1,460.6 | 47.3% | 10.1% | 1,523.0 | 51.5% | 5.6% |

| (+) Other Expenses (a) | (21.3) | (0.7%) | 51.3 | 1.7% | n.m | (24.2) | (0.8%) | (12.0%) |

| Adjusted EBITDA | 1,587.2 | 49.5% | 1,512.0 | 49.0% | 5.0% | 1,498.8 | 50.7% | 5.9% |

(a) Consists of the fair value adjustment related to associates call option, earn-out and earn-out interests related to acquisitions, loss of control of subsidiaries and divestment of assets.

Adjusted EBITDA was R$1,587.2 million in the quarter, compared with R$1,498.8 million in 2Q23. This growth is mostly explained by higher Total Revenue and Income, excluding Other Financial Income, due to the growth of our business. Adjusted EBITDA Margin was 49.5% in the quarter, compared with 50.7% in 2Q23 and 49.0% in 1Q24. The sequential increase in Adjusted EBITDA margin is mainly explained by higher revenues in the period, combined with lower Selling Expenses as percentage of revenues. These effects were partially compensated by higher Other Operating Expenses as a percentage of revenues.

SEGMENT REPORTING

Below, we provide our main financial metrics broken down into our two reportable segments and non-allocated activities.

Table 12: Financial metrics by segment

| Segment Reporting (R$mn Adjusted) | 2Q24 | % Rev | 1Q24 | % Rev | Δ q/q % | 2Q23 | % Rev | Δ y/y % |

| Total Revenue and Income | 3,205.9 | 100.0% | 3,084.9 | 100.0% | 3.9% | 2,954.8 | 100.0% | 8.5% |

| Financial Services | 2,822.2 | 100.0% | 2,710.3 | 100.0% | 4.1% | 2,551.2 | 100.0% | 10.6% |

| Software | 383.7 | 100.0% | 369.1 | 100.0% | 4.0% | 382.9 | 100.0% | 0.2% |

| Non-Allocated | 0.0 | n.a. | 5.5 | 100.0% | (100.0%) | 20.7 | 100.0% | (100.0%) |

| Adjusted EBITDA | 1,587.2 | 49.5% | 1,512.0 | 49.0% | 5.0% | 1,498.8 | 50.7% | 5.9% |

| Financial Services | 1,523.5 | 54.0% | 1,444.0 | 53.3% | 5.5% | 1,427.5 | 56.0% | 6.7% |

| Software | 63.9 | 16.7% | 65.8 | 17.8% | (2.8%) | 66.5 | 17.4% | (3.8%) |

| Non-Allocated | (0.2) | n.a. | 2.2 | 40.3% | n.m | 4.9 | 23.4% | (104.1%) |

| Adjusted EBT | 652.2 | 20.3% | 567.6 | 18.4% | 14.9% | 447.0 | 15.1% | 45.9% |

| Financial Services | 607.8 | 21.5% | 528.6 | 19.5% | 15.0% | 398.2 | 15.6% | 52.6% |

| Software | 44.6 | 11.6% | 37.2 | 10.1% | 20.0% | 45.5 | 11.9% | (1.9%) |

| Non-Allocated | (0.2) | n.a. | 1.9 | 34.2% | n.m | 3.4 | 16.2% | n.m |

- Financial Services segment Adjusted EBT was R$607.8 million in the quarter, representing a 52.6% year over year increase and 15.0% on a quarter over quarter basis. Adjusted EBT margin was 21.5%, an increase of 5.9 percentage points from 15.6% in 2Q23. This year over year increase was driven by higher revenues from the segment, combined with lower Financial and Administrative Expenses as a percentage of revenues. These effects were partially offset by higher Cost of Services and Selling Expenses as a percentage of revenues.

- Software Segment Adjusted EBITDA was R$63.9 million in 2Q24, with a margin of 16.7%, compared with R$66.5 million and a margin of 17.4% in the prior-year period. The year over year decrease in Adjusted EBITDA is mainly explained by a non-recurring severance expense of R$3.2 million and by our decision to focus on growing recurring versus non recurring revenues, which has a negative impact on the short term, but should be accretive for the business long-term.

Adjusted Net Cash

Our Adjusted Net Cash, a non-IFRS metric, consists of the items detailed in Table 13 below:

Table 13: Adjusted Net Cash

| Adjusted Net Cash (R$mn) | 2Q24 | 1Q24 | 2Q23 |

| Cash and cash equivalents | 4,743.2 | 4,988.3 | 2,202.7 |

| Short-term investments | 106.6 | 463.7 | 3,493.4 |

| Accounts receivable from card issuers (a) | 27,556.2 | 26,552.2 | 18,573.4 |

| Financial assets from banking solution | 6,967.8 | 6,620.3 | 4,099.3 |

| Derivative financial instrument (b) | 69.1 | 0.2 | 7.6 |

| Adjusted Cash | 39,443.0 | 38,624.6 | 28,376.5 |

| Retail deposits (c) | (6,472.0) | (5,985.0) | (3,918.6) |

| Accounts payable to clients | (18,512.9) | (19,044.4) | (15,555.8) |

| Institutional deposits and marketable debt securities | (5,301.9) | (4,162.6) | (2,390.1) |

| Other debt instruments | (3,787.2) | (3,942.4) | (1,844.5) |

| Derivative financial instrument (b) | (112.2) | (350.5) | (340.2) |

| Adjusted Debt | (34,186.1) | (33,484.9) | (24,049.2) |

| Adjusted Net Cash | 5,256.9 | 5,139.8 | 4,327.2 |

(a) Accounts Receivable from Card Issuers are accounted for at their fair value in our balance sheet.

(b) Refers to economic hedge.

(c) Includes deposits from banking customers and time deposits from retail clients. For more information of retail deposits, please refer to note 5.6.1 in our Financial Statements.

As of June 30, 2024, the Company’s Adjusted Net Cash was R$5,256.9 million, R$117.1 million higher compared with 1Q24, mostly explained by:

- R$731.6 million of cash net income, which is our net income plus non-cash income and expenses as reported in our statement of cash flows;

- R$84.6 million from labor and social security liabilities;

- -R$344.6 million of capex;

- -R$236.5 million from buyback of shares;

- -R$121.3 million from loans operations portfolio which is net of provision expenses and interest;

- R$3.4 million from other effects.

Cash Flow

Table 14: Cash Flow

| Cash Flow (R$mn) | 2Q24 | 2Q23 |

| Net income (loss) for the period | 498.3 | 307.2 |

| Adjustments on Net Income: | ||

| Depreciation and amortization | 224.2 | 221.7 |

| Deferred income tax expenses | 2.0 | 40.9 |

| Gain (loss) on investment in associates | 0.4 | 0.8 |

| Accrued interest, monetary and exchange variations, net | 59.2 | (44.3) |

| Provision (reversal) for contingencies | 23.9 | 7.5 |

| Share-based payment expense | 64.4 | 50.4 |

| Allowance for expected credit losses | 48.3 | 21.6 |

| Loss on disposal of property, equipment and intangible assets | 8.2 | 30.1 |

| Effect of applying hyperinflation accounting | 1.5 | (0.0) |

| Loss on sale of subsidiary | 0.0 | 0.0 |

| Fair value adjustments in financial instruments at FVPL | (189.8) | 8.2 |

| Fair value adjustment to derivatives | (3.4) | 4.0 |

| Remeasurement of previously held interest in subsidiary acquired acquired | (5.7) | 1.2 |

| Working capital adjustments: | ||

| Accounts receivable from card issuers | (395.9) | 1,284.8 |

| Receivables from related parties | (2.6) | 9.7 |

| Recoverable taxes | 54.6 | (9.4) |

| Prepaid expenses | 82.4 | 19.8 |

| Trade Accounts Receivable, banking solution and other assets | 169.3 | 7.9 |

| Loans operations portfolio | (121.3) | 0.0 |

| Accounts payable to clients | (2,237.9) | (1,427.1) |

| Taxes payable | 54.2 | 18.5 |

| Labor and social security liabilities | 84.6 | 67.3 |

| Payment of contingencies | (22.2) | (1.3) |

| Trade accounts payable and other liabilities | 80.4 | (3.3) |

| Interest paid | (262.3) | (303.7) |

| Interest income received, net of costs | 1,080.7 | 538.9 |

| Income tax paid | (11.5) | (18.9) |

| Net cash used in (provided by) operating activity | (716.1) | 832.5 |

| Investing activities | ||

| Purchases of property and equipment | (210.3) | (196.2) |

| Purchases and development of intangible assets | (134.3) | (136.0) |

| Proceeds from (acquisition of ) short-term investments, net | 359.1 | (147.2) |

| Proceeds from disposal long-term investments - equity securities | 57.5 | 0.0 |

| Proceeds from the disposal of non-current assets | 4.2 | 0.0 |

| Acquisition of subsidiary, net of cash acquired | (9.1) | 0.0 |

| Payment for interest in subsidiaries acquired | (134.0) | (28.7) |

| Net cash used in investing activities | (66.8) | (508.1) |

| Financing activities | ||

| Proceeds from institutional deposits and marketable debt securities | 891.1 | 0.0 |

| Payment of institutional deposits and marketable debt securities | (5.4) | 0.0 |

| Payment to other debt instruments | (780.1) | (1,713.1) |

| Proceeds from other debt instruments | 663.4 | 1,748.2 |

| Payment of principal portion of leases liabilities | (14.6) | (18.9) |

| Repurchase of own shares | (236.5) | 0.0 |

| Acquisition of non-controlling interests | 0.1 | (0.3) |

| Dividends paid to non-controlling interests | (0.3) | (0.5) |

| Net cash provided by financing activities | 517.7 | 15.4 |

| Effect of foreign exchange on cash and cash equivalents | 20.1 | 7.3 |

| Change in cash and cash equivalents | (245.1) | 347.1 |

| Cash and cash equivalents at beginning of period | 4,987.1 | 1,855.6 |

| Cash and cash equivalents at end of period | 4,742.0 | 2,202.7 |

Our cash flow in the quarter was explained by:

Net cash used in operating activities was R$716.1 million in 2Q24, explained by R$731.6 million of Net Income after non-cash adjustments and R$1,447.6 million outflow from working capital variation. Working capital is composed of (i) R$1,553.1 million outflow from changes related to accounts receivable from card issuers, accounts payable to clients and interest income received, net of costs; (ii) R$273.8 million outflow from interest paid and income tax paid; (iii) R$121.3 million outflow from our credit product; (iv) R$80.4 million inflow from trade accounts payable and other liabilities; (v) R$82.4 million inflow from prepaid expenses; (vi) R$84.6 million inflow from labor and social security liabilities; (vii) R$ 108.8 million inflow from recoverable taxes and taxes payable; (viii) R$169.3 million inflow from trade accounts receivable, banking solution and other assets; and (ix) R$24.8 million outflow from other working capital changes.

Net cash used in investing activities was R$66.8 million in 1Q24, explained by (i) R$344.6 million in capex, of which R$210.3 million related to property and equipment and R$134.3 million related to purchases and development of intangible assets and (ii) R$143.1 million from M&A. These effects were partially offset by (iii) R$359.1 million from proceeds from short-term investments; (iv) R$57.5 million from proceeds from the disposal of long-term investments; and (v) R$ 4.2 million from the disposal of non-current assets.

Net cash provided by financing activities was R$517.7 million, explained by (i) R$885.7 million from proceeds from institutional deposits and marketable debt securities, net of payments which were partially offset by (ii) R$116.7 million from payment of other debt instruments, net of proceeds; (iii) R$236.5 million in repurchase of our own shares; (iv) R$14.6 million of payment of leases liabilities; and (v) R$0.2 million cash outflow from capital events related to non-controlling interests. For more information on institutional deposits and marketable debt securities please refer to note 5.6.1 from our Financial Statements.

Consolidated Balance Sheet Statement

Table 15: Consolidated Balance Sheet Statement

| Balance Sheet (R$mn) | 2Q24 | 4Q23 |

| Assets | ||

| Current assets | 40,846.6 | 37,152.6 |

| Cash and cash equivalents | 4,743.2 | 2,176.4 |

| Short-term investments | 106.6 | 3,481.5 |

| Financial assets from banking solution | 6,967.8 | 6,397.9 |

| Accounts receivable from card issuers | 27,472.0 | 23,895.5 |

| Trade accounts receivable | 438.3 | 459.9 |

| Loans operations portfolio | 474.2 | 210.0 |

| Recoverable taxes | 182.7 | 146.3 |

| Derivative financial instruments | 71.3 | 4.2 |

| Other assets | 390.5 | 380.9 |

| Non-current assets | 11,853.1 | 11,541.0 |

| Long-term investments | 32.4 | 45.7 |

| Accounts receivable from card issuers | 84.3 | 81.6 |

| Trade accounts receivable | 22.0 | 28.5 |

| Loans operations portfolio | 112.6 | 40.8 |

| Receivables from related parties | 0.7 | 2.5 |

| Deferred tax assets | 755.6 | 664.5 |

| Other assets | 133.3 | 137.5 |

| Investment in associates | 79.2 | 83.0 |

| Property and equipment | 1,728.2 | 1,661.9 |

| Intangible assets | 8,905.0 | 8,794.9 |

| Total Assets | 52,699.7 | 48,693.6 |

| Liabilities and equity | ||

| Current liabilities | 30,048.2 | 29,142.7 |

| Retail deposits | 6,472.0 | 6,119.5 |

| Accounts payable to clients | 18,472.9 | 19,163.7 |

| Trade accounts payable | 525.7 | 513.9 |

| Institutional deposits and marketable debt securities | 1,443.9 | 475.3 |

| Other debt instruments | 1,594.0 | 1,404.7 |

| Labor and social security liabilities | 504.0 | 515.7 |

| Taxes payable | 676.3 | 514.3 |

| Derivative financial instruments | 112.2 | 316.2 |

| Other liabilities | 247.2 | 119.5 |

| Non-current liabilities | 7,432.7 | 4,874.9 |

| Accounts payable to clients | 40.0 | 35.5 |

| Institutional deposits and marketable debt securities | 3,858.0 | 3,495.8 |

| Other debt instruments | 2,370.7 | 143.5 |

| Deferred tax liabilities | 613.8 | 546.5 |

| Provision for contingencies | 233.2 | 208.9 |

| Labor and social security liabilities | 30.7 | 34.3 |

| Other liabilities | 286.3 | 410.5 |

| Total liabilities | 37,480.9 | 34,017.6 |

| Equity attributable to owners of the parent | 15,163.6 | 14,622.3 |

| Issued capital | 0.1 | 0.1 |

| Capital reserve | 14,084.4 | 14,056.5 |

| Treasury shares | (490.8) | (282.7) |

| Other comprehensive income (loss) | (468.0) | (320.4) |

| Retained earnings (accumulated losses) | 2,038.0 | 1,168.9 |

| Non-controlling interests | 55.2 | 53.7 |

| Total equity | 15,218.8 | 14,676.0 |

| Total liabilities and equity | 52,699.7 | 48,693.6 |

Other Information

Conference Call

Stone will discuss its 2Q24 financial results during a teleconference today, August 14, 2024, at 5:00 PM ET / 6:00 PM BRT.

The conference call can be accessed live over the Zoom webinar (ID: 854 5992 8852| Password: 819157). It can also be accessed over the phone by dialing +1 646 931 3860 or +1 669 444 9171 from the U.S. Callers from Brazil can dial +55 21 3958 7888. Callers from the UK can dial +44 330 088 5830.

The call will also be webcast live and a replay will be available a few hours after the call concludes. The live webcast and replay will be available on Stone’s investor relations website at https://investors.stone.co/.

About Stone Co.

Stone Co. is a leading provider of financial technology and software solutions that empower merchants to conduct commerce seamlessly across multiple channels and help them grow their businesses.

Investor Contact

Investor Relations

investors@stone.co

Glossary of Terms

- "ARPAC” (Average Revenue Per Active Client)”: Banking ARPAC considers banking revenues, such as floating from demand deposits, card interchange fees, insurance and transactional fees, as well as PIX QR Code revenues.

- Banking Active Clients: clients who have transacted at least R$1 in the past 30 days.

- Banking Deposits: demand deposits from banking customers, including MSMB and Key Account clients.

- "Consolidated Credit Metrics”: refer to our working capital loan and credit card portfolios.

- "Credit Clients”: consider merchants who have an active working capital loan contract with Stone at the end of the period.

- "Credit Revenues”: In 2Q23, credit revenues were recognized net of provision for expected credit losses in Financial Income. From 3Q23 onwards, credit revenues are recognized gross of provision for expected losses, which are allocated in Cost of Services.

- “CTPV”: Means Card Total Payment Volume and refers only to transactions settled through cards. Does not include PIX QR Code volumes.

- “Active Payments Client Base”: refers to MSMBs and Key Accounts. Considers clients that have transacted at least once over the preceding 90 days, except for Ton active clients which consider clients that have transacted once in the preceding 12 months. As from 3Q22, does not consider clients that use only TapTon.

- “Adjusted Net Cash”: is a non-IFRS financial metric and consists of the following items: (i) Adjusted Cash: Cash and cash equivalents, Short-term investments, Accounts receivable from card issuers, Financial assets from banking solution and Derivative financial instrument; minus (ii) Adjusted Debt: Retail deposits, Accounts payable to clients, Institutional deposits and marketable debt securities, Other debt instruments and Derivative financial instrument.

- “Banking”: refers to our digital banking solution and includes insurance products.

- “Financial Services” segment: this segment is comprised of our financial services solutions serving both MSMBs and Key Accounts. Includes mainly our payments, digital banking and credit solutions.

- “Key Accounts”: refers to operations in which Pagar.me acts as a fintech infrastructure provider for different types of clients, especially larger ones, such as mature e-commerce and digital platforms, commonly delivering financial services via APIs. It also includes clients that are onboarded through our integrated partners program, regardless of client size.

- “Membership fees”: refer to the upfront fee paid by merchants for all Ton offerings and specific ones for Stone when they join our client base. Until December 31, 2023, membership fees revenues were recognized fully at the time of acquisition. From January 1, 2024 onwards, the Group recognizes revenues from membership fees deferred through the expected lifetime of the client.

- “MSMB segment”: refer to SMBs – small and medium business (online and offline) and micro-merchants, from our Stone, Pagar.me and Ton products. Considers clients that have transacted at least once over the preceding 90 days, except for Ton active clients which consider clients that have transacted once in the preceding 12 months. As from 3Q22, does not consider clients that use only TapTon.

- “MSMB CTPV Overlap”: refers to the MSMB CTPV in Software installed base within the priority verticals - Gas Station, Retail, Drugstores, Food and horizontal software.

- “Non-allocated”: comprises other smaller businesses which are not allocated in our Financial Services or Software segments. From 2Q24 onwards, revenues in the non-allocated business segment are inexistent, since we divested assets within the segment.

- “NPL (Non-Performing Loans)”: is the total outstanding of the contract whenever the clients default on an installment. More information on the total overdue by aging considering only the individual installments can be found in Note 5.4.1 of the Financial Statements.

- “PIX QR Code”: includes the volume of PIX QR Code transactions from dynamic POS QR Code and static QR Code from MSMB and Key Accounts merchants, unless otherwise noted.

- “Provisions ratio”: calculated as accumulated provisions for expected credit losses divided by the total portfolio amount in the period.

- “Revenue”: refers to Total Revenue and Income net of taxes, interchange fees retained by card issuers and assessment fees paid to payment schemes.

- “Software” segment: composed of our Strategic Verticals (Retail, Gas Stations, Food, Drugstores and horizontal software), Enterprise and Other Verticals. The Software segment includes the following solutions: POS/ERP, TEF and QR Code gateways, reconciliation, CRM, OMS, e-commerce platform, engagement tool, ads solution, and marketplace hub.

- “Take Rate (Key Accounts)”: managerial metric that considers the sum of revenues from financial services solutions offered to Key Account clients, excluding non-allocated revenues, divided by Key Accounts CTPV.

- “Take Rate (MSMB)”: managerial metric that considers the sum of revenues from financial services solutions offered to MSMBs, excluding Ton’s membership fee, TAG revenues and other non-allocated revenues, divided by MSMB CTPV.

- “TPV”: Total Payment Volume. Reported TPV figures consider all card volumes settled by StoneCo, including PIX QR Code transactions from dynamic POS QR Code and static QR Code from MSMB and Key Accounts merchants, unless otherwise noted.

- “Working Capital Portfolio”: is gross of provisions for losses, but net of amortizations.

Forward-Looking Statements

This press release contains "forward-looking statements" within the meaning of the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made as of the date they were first issued and were based on current expectations, estimates, forecasts and projections as well as the beliefs and assumptions of management. These statements identify prospective information and may include words such as “believe”, “may”, “will”, “aim”, “estimate”, “continue”, “anticipate”, “intend”, “expect”, “forecast”, “plan”, “predict”, “project”, “potential”, “aspiration”, “objectives”, “should”, “purpose”, “belief”, and similar, or variations of, or the negative of such words and expressions, although not all forward-looking statements contain these identifying words.

Forward-looking statements are subject to a number of risks and uncertainties, many of which involve factors or circumstances that are beyond Stone’s control.

Stone’s actual results could differ materially from those stated or implied in forward-looking statements due to a number of factors, including but not limited to: more intense competition than expected, lower addition of new clients, regulatory measures, more investments in our business than expected, and our inability to execute successfully upon our strategic initiatives, among other factors.

About Non-IFRS Financial Measures

To supplement the financial measures presented in this press release and related conference call, presentation, or webcast in accordance with IFRS, Stone also presents non-IFRS measures of financial performance, including: Adjusted Net Income, Adjusted EPS (diluted), Adjusted Net Margin, Adjusted Net Cash / (Debt), Adjusted Profit (Loss) Before Income Taxes, Adjusted Pre-Tax Margin, EBITDA and Adjusted EBITDA.

A “non-IFRS financial measure” refers to a numerical measure of Stone’s historical or future financial performance or financial position that either excludes or includes amounts that are not normally excluded or included in the most directly comparable measure calculated and presented in accordance with IFRS in Stone’s financial statements. Stone provides certain non-IFRS measures as additional information relating to its operating results as a complement to results provided in accordance with IFRS. The non-IFRS financial information presented herein should be considered in conjunction with, and not as a substitute for or superior to, the financial information presented in accordance with IFRS. There are significant limitations associated with the use of non-IFRS financial measures. Further, these measures may differ from the non-IFRS information, even where similarly titled, used by other companies and therefore should not be used to compare Stone’s performance to that of other companies.

Stone has presented Adjusted Net Income to eliminate the effect of items from Net Income that it does not consider indicative of its continuing business performance within the period presented. Stone defines Adjusted Net Income as Net Income (Loss) for the Period, adjusted for (1) amortization of fair value adjustment on acquisitions, (2) unusual income and expenses. Adjusted EPS (diluted) is calculated as Adjusted Net income attributable to owners of the parent (Adjusted Net Income reduced by Net Income attributable to Non-Controlling interest) divided by diluted number of shares.

Stone has presented Adjusted Profit Before Income Taxes and Adjusted EBITDA to eliminate the effect of items that it does not consider indicative of its continuing business performance within the period presented. Stone adjusts these metrics for the same items as Adjusted Net Income, as applicable.

Stone has presented Adjusted Net Cash metric in order to adjust its Net Cash / (Debt) by the balances of Accounts Receivable from Card Issuers and Accounts Payable to Clients, since these lines vary according to the Company’s funding source together with the lines of (i) Cash and Cash Equivalents, (ii) Short-term Investments, (iii) Debt balances and (iv) Derivative Financial Instruments related to economic hedges of short term investments in assets, due to the nature of Stone’s business and its prepayment operations. In addition, it also adjusts by the balances of Financial Assets from Banking Solutions and Deposits from Banking Customers.

A PDF accompanying this announcement is available at

http://ml.globenewswire.com/Resource/Download/2fc36110-92f6-4c47-b360-e817faa0c6b3

![]()