New York, NY – November 11, 2025 – While the broader S&P 500 index largely celebrated a day of gains fueled by optimism surrounding a tentative bipartisan agreement to end a prolonged U.S. government shutdown, the Communication Services sector found itself wrestling with a complex array of challenges. On November 11, 2025, the sector presented a mixed picture, with some segments experiencing headwinds stemming from concerns over AI stock valuations, specific company-level setbacks, and a general rotation away from "pure growth" equities. This divergence highlights a critical juncture for an industry central to the digital economy, demanding strategic adaptation amidst rapid technological evolution.

The immediate implications for the market were twofold: a surge in overall investor confidence as the government shutdown loomed closer to resolution, leading to a rally across major indices, particularly in technology and discretionary stocks. However, beneath this surface of broad market cheer, the Communication Services sector, especially its growth-oriented constituents, faced a more nuanced reality, signaling that not all boats were lifted equally by the rising tide of optimism.

Sector Performance Under Scrutiny: AI Valuations and Shifting Sentiments

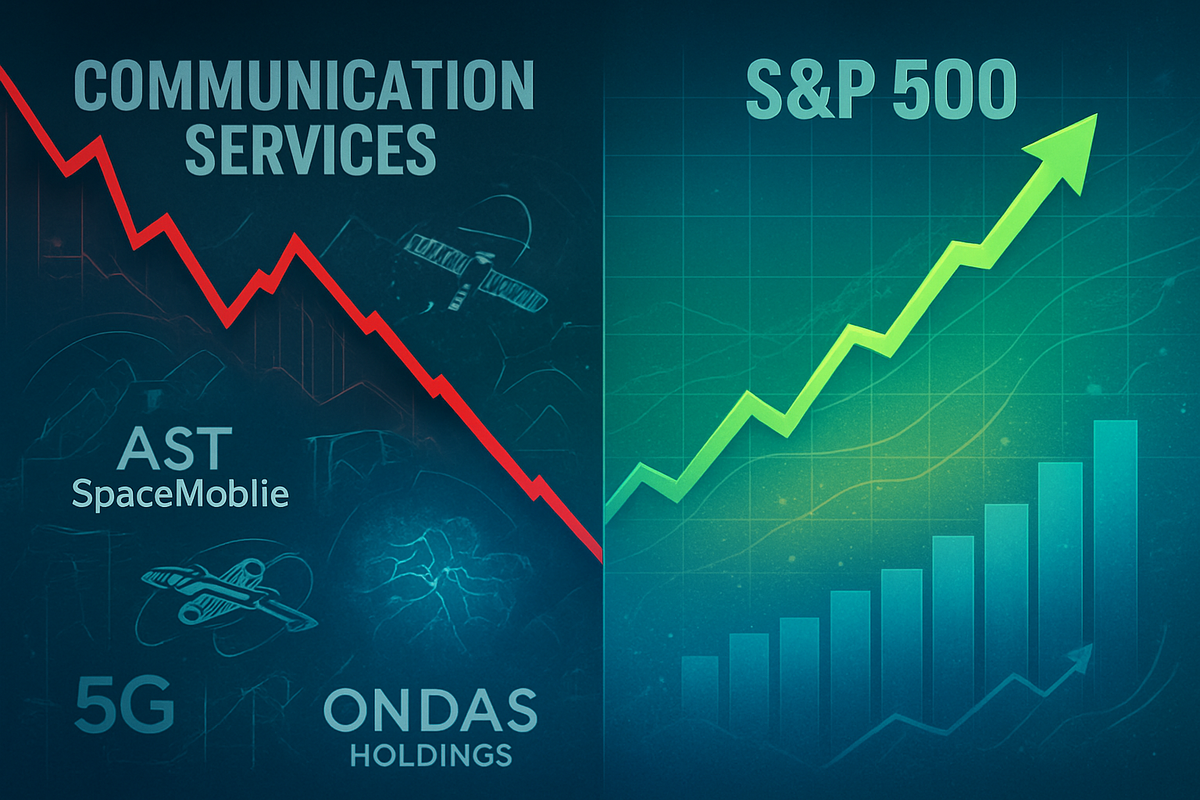

The S&P 500 Communication Services sector's performance on November 11, 2025, was characterized by underlying pressures despite an overall positive market close. While the Communication Services Select Sector SPDR (XLC) had advanced by 1% on the preceding trading day, the sector's constituents faced renewed scrutiny. The S&P 500 index itself opened lower, "primarily affected by drops in the technology and communication services sectors," a direct result of declines in major AI-related stocks and new data pointing to a weakening U.S. labor market. This continued a trend observed in October, where the Communication Services sector lagged other sectors, declining by 3.0%. Furthermore, FactSet data indicated that the sector was among those reporting a year-over-year decline in earnings for Q3 2025, even as it experienced revenue growth. The massive capital expenditure required for AI infrastructure also appeared to weigh on investor sentiment, raising questions about the sustainability of current valuations.

A significant driver of this sector-specific downturn was the volatile sentiment surrounding AI-related stocks. While AI enthusiasm had resurfaced earlier in the week, leading to gains in semiconductor stocks, November 11 saw a shift. Concerns mounted that many AI stocks had become "too expensive," drawing parallels to the 2000 dot-com bubble. This led to a "growing tug of war between conviction and caution" regarding AI valuations. Prominent AI chipmaker Nvidia (NASDAQ: NVDA) notably sank 2.4% following news that SoftBank had sold its entire stake in the company for $5.83 billion. Another AI cloud platform, CoreWeave, saw its shares fall by 14.8% due to supply-chain issues. These movements contributed to a broader bearish sentiment in technology and AI, evidenced by a net addition of $3.75 billion in short positions on the Nasdaq.

Adding to the complexity was new data revealing a "weakening U.S. labor market." ADP reports indicated a decrease in U.S. private sector jobs in the weeks leading up to October 25. While this "soft labor-market data" typically signals economic slowdown, some investors interpreted it as increasing the likelihood of further Federal Reserve interest rate cuts, which could be a positive for the broader market in the long run. However, its immediate impact on the Communication Services and Tech sectors appeared secondary to the more pressing concerns surrounding AI valuations and a broader market rotation out of "pure growth" technology and communication services stocks and into "pure value" sectors like healthcare, energy, and consumer staples.

AST SpaceMobile and Ondas Holdings Face Individual Headwinds and Opportunities

Amidst the sector's mixed performance, individual companies like AST SpaceMobile (NASDAQ: ASTS) and Ondas Holdings (NASDAQ: ONDS) presented distinct narratives, each grappling with specific operational challenges and strategic developments.

AST SpaceMobile (NASDAQ: ASTS) faced a challenging period following the release of its third-quarter 2025 financial results on November 10, 2025. The satellite-to-cellular company reported revenue and profit figures that fell below analysts' estimates, with a net loss of $122.9 million (or $0.45 per share) and revenue of $14.7 million, missing consensus by 27.5%. This weaker performance was primarily attributed to delays in U.S. government contract milestones and gateway deliveries, coupled with elevated operating costs. Despite these setbacks, AST SpaceMobile reiterated its full-year 2025 revenue projection of $50 million to $75 million, banking on crucial fourth-quarter events like gateway equipment shipments and initial commercial service revenue. Operationally, the company announced the planned launch of its BlueBird 6 satellite (FM1) in early December and the shipment of BlueBird 7 (FM2) in November, aiming for 45 to 60 satellites by the end of 2026. Furthermore, on November 7, 2025, AST SpaceMobile and Vodafone announced a new European satellite operations center in Germany, signaling strong commercial momentum despite execution risks. However, the stock reflected investor apprehension, falling 14.51% over the previous week and 23.50% over the last month, trading at $67.89 as of November 11, 2025.

Ondas Holdings (NASDAQ: ONDS) also saw significant activity leading up to November 11, 2025. The company, which focuses on autonomous aerial and ground robot intelligence and defense technology, announced it would report its Q3 2025 financial results on November 13, 2025, with analysts projecting a loss of 5 cents per share on an anticipated 398% year-over-year revenue jump to $7.37 million. Ondas's stock had shown remarkable growth, skyrocketing 618.2% over the past six months and trending up by 4.44% on November 10, 2025. This surge was attributed to strategic expansions, including acquisitions in defense and drone technology, and the appointment of Maj. Gen. (Ret.) Yoav Har-Even to its Ondas Autonomous Systems (OAS) Advisory Board. These moves aim to accelerate the global deployment of unmanned and autonomous systems for defense and security markets, areas that could indirectly leverage AI advancements. However, concerns regarding potential share dilution persisted, with a shelf registration for approximately $5.59 million in common stock and a proposed amendment to double authorized common shares up for a vote on November 18, 2025. Despite its strategic moves, the company’s operating margin remained grim at -227.7%, reflecting heavy investment in future growth. As of November 11, 2025, ONDS was trading at $5.88, having fallen 36% in a month, indicating high volatility.

Wider Significance: 5G Monetization, Satellite Disruption, and Regulatory Crosscurrents

The challenging performance within the Communication Services sector on November 11, 2025, underscores several broader industry trends and has significant ripple effects. The sector continues to grapple with the 5G monetization conundrum. Despite massive capital expenditures (CapEx) on 5G infrastructure, telecom operators are struggling to translate these investments into proportional revenue growth, with average revenue per user (ARPU) often flat or declining. This delay in monetizing advanced 5G use cases beyond basic mobile broadband impacts innovation cycles in reliant industries and puts financial strain on telcos, potentially limiting future investments in 6G and critical infrastructure.

Simultaneously, the rise of satellite broadband, particularly from Low Earth Orbit (LEO) constellations, is proving to be a disruptive force. While offering a crucial solution for bridging the digital divide in remote areas, it intensifies competition for traditional fixed and mobile broadband providers. This necessitates an acceleration of hybrid connectivity solutions, integrating satellite internet with terrestrial 5G and fiber-optic networks. However, the proliferation of satellites also raises concerns about space debris and the long-term sustainability of orbital environments, potentially complicating efforts to fund and implement mitigation strategies.

The ripple effects extend to equipment vendors and infrastructure providers, who face reduced demand if telecom CapEx slows. Content and cloud providers, while potentially benefiting from telcos seeking to diversify revenue, also face limitations if the core telecom sector struggles. Enterprise and IoT markets might experience delays or higher costs for digital transformation initiatives if 5G enterprise solutions are not effectively delivered. These pressures could also accelerate consolidation and M&A activity within the sector as companies seek scale and efficiency.

From a regulatory and policy standpoint, a challenging sector performance could intensify calls for "fair share" contributions from large content and tech companies towards network investments. Regulators may also reconsider spectrum allocation mechanisms and face increased pressure to develop stringent international coordination for space governance and debris mitigation. Consumer protection measures and digital inclusion initiatives would also gain urgency. Historically, this period bears resemblances to the dot-com bubble and telecom bust of the early 2000s, where massive overinvestment outpaced real revenue generation, leading to widespread bankruptcies. While today's demand for connectivity is more established, the echoes of speculative bubbles and overcapacity concerns, particularly in areas like AI and 5G, remain relevant.

What Comes Next: Strategic Pivots and Emerging Opportunities

The path forward for the Communication Services sector, following the challenges observed on November 11, 2025, will be defined by strategic adaptation and a relentless pursuit of innovation. In the short term, companies are likely to prioritize cost optimization, leveraging AI-driven automation to streamline operations and enhance network performance. There will be an accelerated push to monetize existing 5G infrastructure through enhanced mobile experiences and premium business services, alongside a focus on improving customer experience through AI-powered support and personalized offerings. Strategic partnerships and service bundling will also be key to retaining subscribers in a competitive market.

In the long term, the sector's trajectory will be shaped by deeper technological integration. This includes the evolution to 5G-Advanced and early research into 6G networks, promising even faster speeds and ultra-reliable low-latency connections for future technologies like holographic communications and digital twins. The integration of satellite broadband will become a standard, complementing terrestrial networks to address coverage gaps and provide resilient connectivity for critical industries, leading to hybrid, multi-orbit network architectures. Artificial Intelligence will move beyond mere optimization to become a core business driver, enabling AI-driven content generation, personalized advertising, and the development of generative AI applications by telecom operators themselves. Companies will also continue to diversify into enterprise and cloud services, becoming "innovation-driven ecosystem builders" by offering specialized solutions in manufacturing, healthcare, and logistics. The sector will also power new immersive experiences and the metaverse through advanced 5G and AI capabilities.

Despite significant opportunities in digital advertising, the expanding IoT ecosystem, and new AI-driven revenue streams, persistent challenges remain. These include substantial ongoing infrastructure investments, intense competition, cybersecurity risks, and increased regulatory scrutiny around data privacy and AI ethics. The sector also faces a digital skills gap and growing concerns over space debris. Companies will likely fall into three categories: "Thrivers" (adaptive innovators like T-Mobile (NASDAQ: TMUS) or Alphabet (NASDAQ: GOOGL)), who successfully integrate new technologies; "Survivors" (steady adapters focusing on core profitability); and "Strugglers" (laggards vulnerable to disruption).

Comprehensive Wrap-up: Navigating a Transformative Era

The events of November 11, 2025, serve as a potent reminder of the dynamic and often unpredictable nature of the Communication Services sector. While broader market sentiment might rally on macro-economic news, the underlying currents of technological transformation, intense competition, and evolving regulatory landscapes continue to shape individual company and sector-wide performance. The immediate challenges, particularly concerning AI valuations and specific company setbacks, underscore a period of profound restructuring rather than outright decline.

Moving forward, the market will be characterized by greater integration of advanced technologies, increasingly personalized services, and an unrelenting drive for efficiency. Companies that can effectively adapt their business models, overcome implementation hurdles for new technologies like 5G and satellite broadband, and proactively address regulatory and ethical concerns surrounding AI will be the ones that thrive. The era of unchecked, hyper-growth for many internet and media companies is evolving into a more disciplined focus on profitability and sustainable strategies.

What Investors Should Watch For in the Coming Months:

- 5G Monetization Strategies: Beyond subscriber numbers, investors should scrutinize actual revenue generation from 5G, particularly in enterprise applications, private networks, and Fixed Wireless Access (FWA). The ability to translate substantial CapEx into tangible returns will be crucial.

- Satellite Broadband Deployment and Adoption: Monitor the progress of LEO constellations, their ability to reduce latency and costs, and their market penetration, especially in bridging the digital divide. Partnerships between satellite providers and traditional telcos will be key indicators.

- AI Integration and ROI: Look for tangible evidence of AI driving operational efficiencies, enhancing network management, and creating new revenue streams, rather than just hype. Regulatory developments concerning AI ethics, data privacy, and potential biases will significantly influence public trust and operational viability.

- Regulatory Landscape and Antitrust Actions: Keep a close eye on governmental policies and regulatory decisions, particularly regarding data privacy, content moderation, and antitrust enforcement against dominant tech and media platforms.

- M&A Activity and Consolidation: The drive for scale and efficiency is likely to fuel continued M&A in the telecom segment. Evaluate deals for their potential to create synergies and drive long-term value.

- Cybersecurity Resilience: With increasing digital connectivity and geopolitical tensions, companies demonstrating robust cybersecurity protocols and risk management will be better positioned to protect critical infrastructure and customer data.

The Communication Services sector on November 11, 2025, represents a landscape of persistent challenges intertwined with unparalleled innovation. Investors equipped with a keen understanding of these dynamics and the strategic implications of 5G, satellite broadband, and AI will be best prepared to identify opportunities in this critical and rapidly evolving industry.

This content is intended for informational purposes only and is not financial advice