Since March 2025, ABM has been in a holding pattern, posting a small loss of 4.7% while floating around $45.31. The stock also fell short of the S&P 500’s 15.5% gain during that period.

Is now the time to buy ABM, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is ABM Not Exciting?

We're swiping left on ABM for now. Here are three reasons there are better opportunities than ABM and a stock we'd rather own.

1. Slow Organic Growth Suggests Waning Demand In Core Business

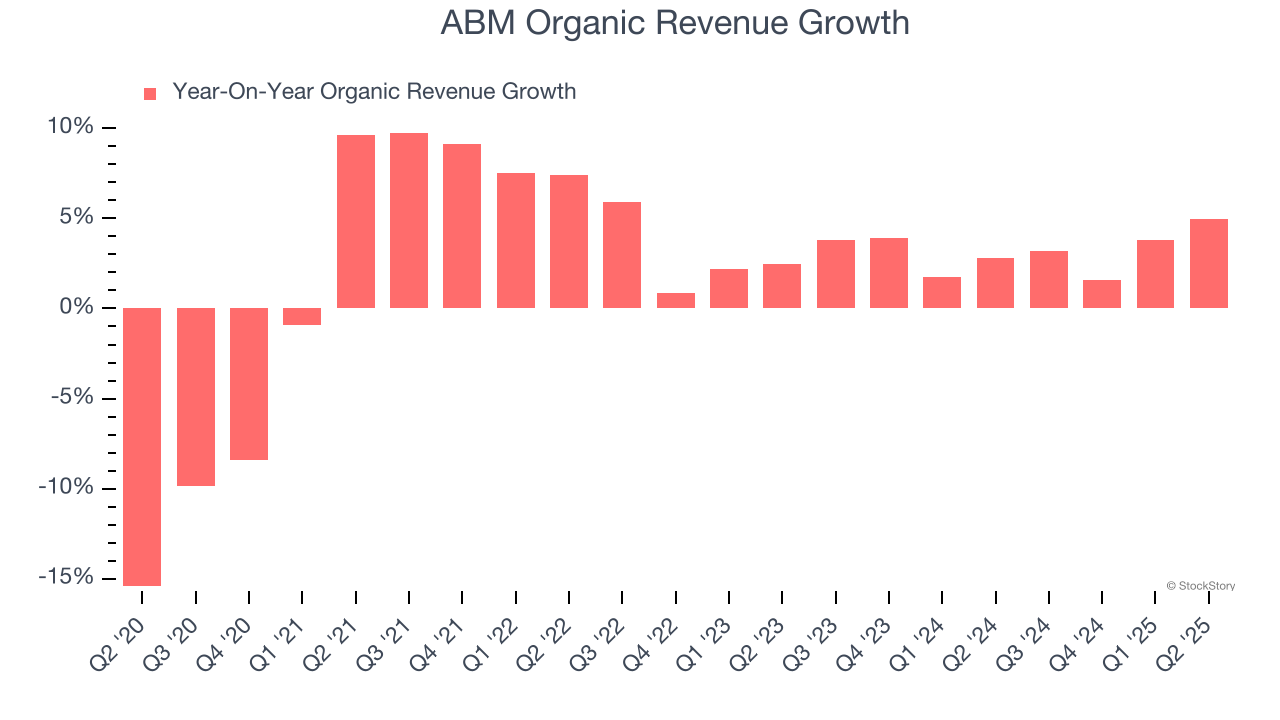

Investors interested in Industrial & Environmental Services companies should track organic revenue in addition to reported revenue. This metric gives visibility into ABM’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, ABM’s organic revenue averaged 3.2% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

2. Recent EPS Growth Below Our Standards

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

ABM’s EPS grew at a weak 1.2% compounded annual growth rate over the last two years, lower than its 3.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, ABM’s margin dropped by 6.4 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business. ABM’s free cash flow margin for the trailing 12 months was breakeven.

Final Judgment

ABM isn’t a terrible business, but it isn’t one of our picks. With its shares lagging the market recently, the stock trades at 11.2× forward P/E (or $45.31 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of ABM

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.