Is G-III Apparel Group, Ltd. A Value Trap?

G-III Apparel (NASDAQ: GIII) is a well-established company with solid results for the Q2 period but it may also be a value trap. The company’s brands are not as strong as some others in the sector and it lacks a dividend which is a prominent feature of other stocks in the group. Trading at 4.5X its earnings it is a value compared to the 6.7X to 13X range the market will pay for names like PVH Corporation (NYSE: PVH), Levi Strauss (NYSE: LEVI), Ralph Lauren (NYSE: RL), or V.F. Corporation (NYSE: VFC), and it is a deep value compared to the broader market, but it is unlikely to see a multiple expansion any time soon and the outlook for revenue and earnings is not supportive of the price action now.

G-III Has Mixed Quarter, Guides Weak

G-III had a decent quarter in Q2 and even led the group with YOY growth of 25.3% but there is an offsetting factor in the 2 and 3-year comparisons. The company has only just regained the pre-pandemic business levels while its competitors grew beyond those levels a few quarters ago. Among the reasons are the company’s brands which aren’t as strong as the top-tier names and the company’s outsized exposure to licensed products specifically sporting-related items. Regardless, the results were as mixed as any in the group and came with the same weakened guidance. The $605.2 million in revenue is up 25.3% from last year but it’s down 5.5% from 2019 and only beat the consensus by 200 basis points.

Moving down to the income, the news is even more tepid with margin narrowing at both the gross and operating levels. The gross margin contracted 210 basis points and the operating margin by 300 to leave the earnings down on a YOY basis. The GAAP earnings are up but include $0.35 in gains associated with the value of the Karl Lagerfeld investment and acquisition of the remaining outstanding shares of the company but the adjusted EPS is down substantially. The worst news is the $0.36 in adjusted EPS is not only down from last year’s $0.41 in adjusted EPS but missed by $0.07 and the outlook for earnings is deteriorating.

The company’s guidance for Q3 and the full year was lowered for both the top and bottom lines. The revenue is now expected in a range slightly below the Marketbeat.com consensus while the outlook for earnings was reduced more drastically. The company is expecting adjusted EPS in the range of $3.60 to $3.70 compared to the consensus fo $4.28 which is a difference of 1500 basis points. Based on the outlook for the industry at large, it is possible this guidance is overly optimistic as well. One point of note is that inventory more than doubled over the past year which may have the company set up for a round of discounts, promotions, and clearance that will dig deeper into the bottom line.

G-III Apparel Group’s Capital Returns Are Not Attractive

G-III Apparel Group has a buyback plan in place and there were 10 million shares left to be repurchased at the end of the 1st quarter but no mention was made of buybacks in the Q2 release. That along with the 0.0% dividend makes it a much less attractive stock than its competitors that pay at least 0.28% in yield (PVH Corporation) and as much as 4.9% (V.F. Corporation), and most of these companies also buy back shares.

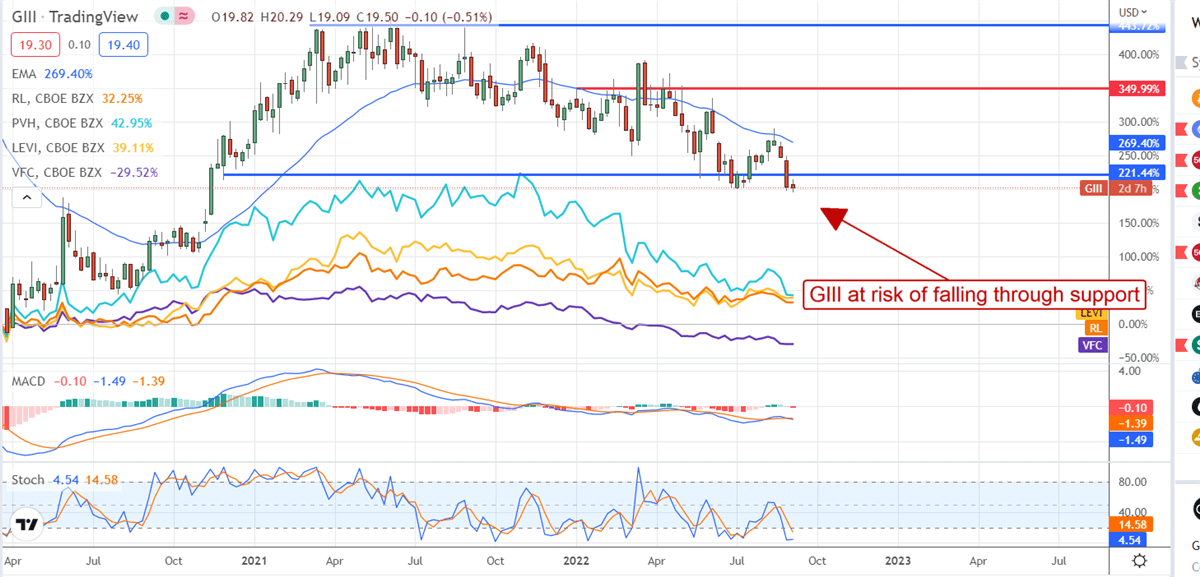

The Technical Outlook: G-III Apparel Outperforms The Group?

Oddly enough, G-III Apparel has been outperforming its peers since the pandemic bottom but take that with a grain of salt. Not only is the stage set for this stock to underperform over the next few quarters but the post-pandemic outperformance disappears and turns into underperformance as you expand the comparison. The takeaway is that G-III Apparel Group is not the best choice for long-term investors, especially if income and dividends are an important part of the investment outlook and plan.

If you believe this article contains misleading, harmful, or spam content, please let us know.

Report this articleMore News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.