Maintenance and Repair Distributors Stocks Q4 In Review: WESCO (NYSE:WCC) Vs Peers

Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at WESCO (NYSE: WCC) and its peers.

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Maintenance and repair distributors that boast reliable selection and quickly deliver products to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to serve customers everywhere. Additionally, maintenance and repair distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

The 9 maintenance and repair distributors stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 0.8%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.5% since the latest earnings results.

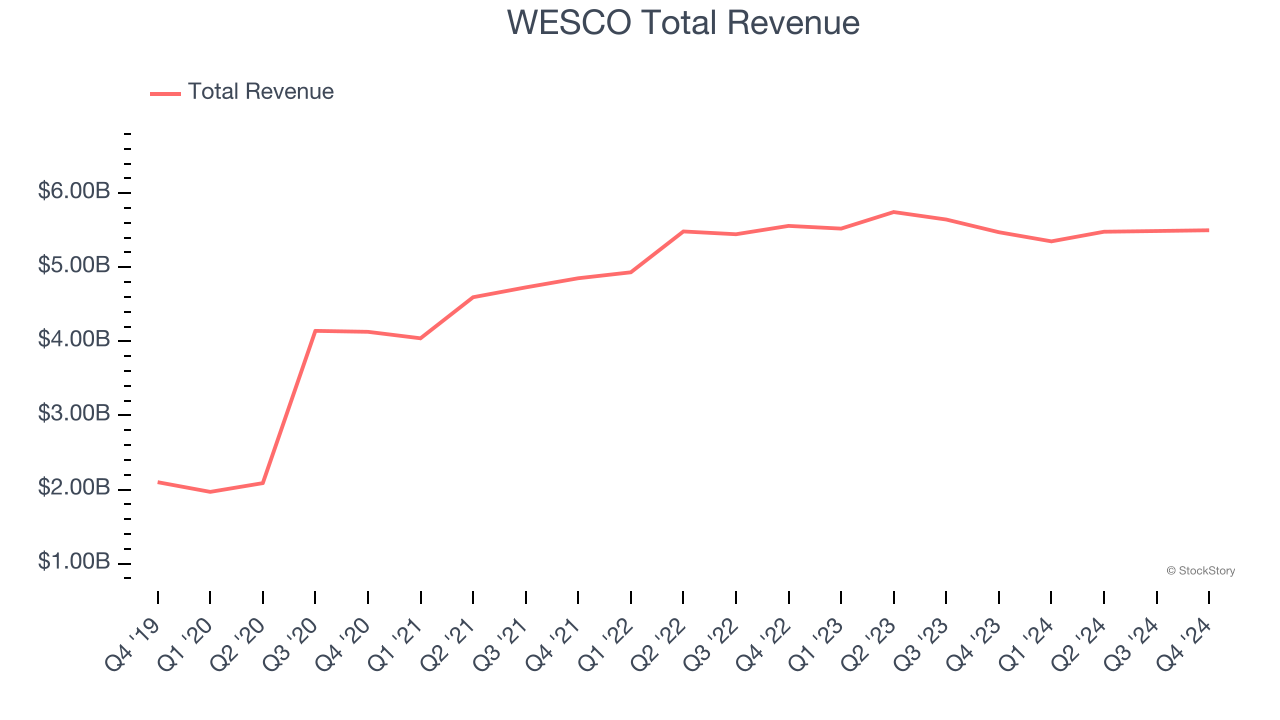

WESCO (NYSE: WCC)

Based in Pittsburgh, WESCO (NYSE: WCC) provides electrical, industrial, and communications products and augments them with services such as supply chain management.

WESCO reported revenues of $5.5 billion, flat year on year. This print exceeded analysts’ expectations by 1.5%. Despite the top-line beat, it was still a slower quarter for the company with a miss of analysts’ adjusted operating income estimates.

"We are pleased with our return to sales growth in the fourth quarter sparked by more than 70% growth year-over-year in our global Data Center business, 20% growth in Broadband Solutions, and renewed positive sales momentum in Electrical and Electronic Solutions. This was partially offset by a slowdown with industrial customers and the expected continued weakness in our utility business in the fourth quarter. With that said, our positive momentum has carried into January with preliminary sales per workday, adjusted for M&A, up 5% versus prior year. Our opportunity pipeline remains at a record level, backlog remains healthy and bid activity levels remain very strong. Gross margin was stable on a full-year basis although we experienced some pressure in Communication and Security Solutions as sales ramped to customers on project deployments. Consistent with past practice, we expect to improve margins as we move through the project deployment life cycle in this segment," said John Engel, Chairman, President, and CEO.

The stock is down 12.3% since reporting and currently trades at $162.54.

Read our full report on WESCO here, it’s free.

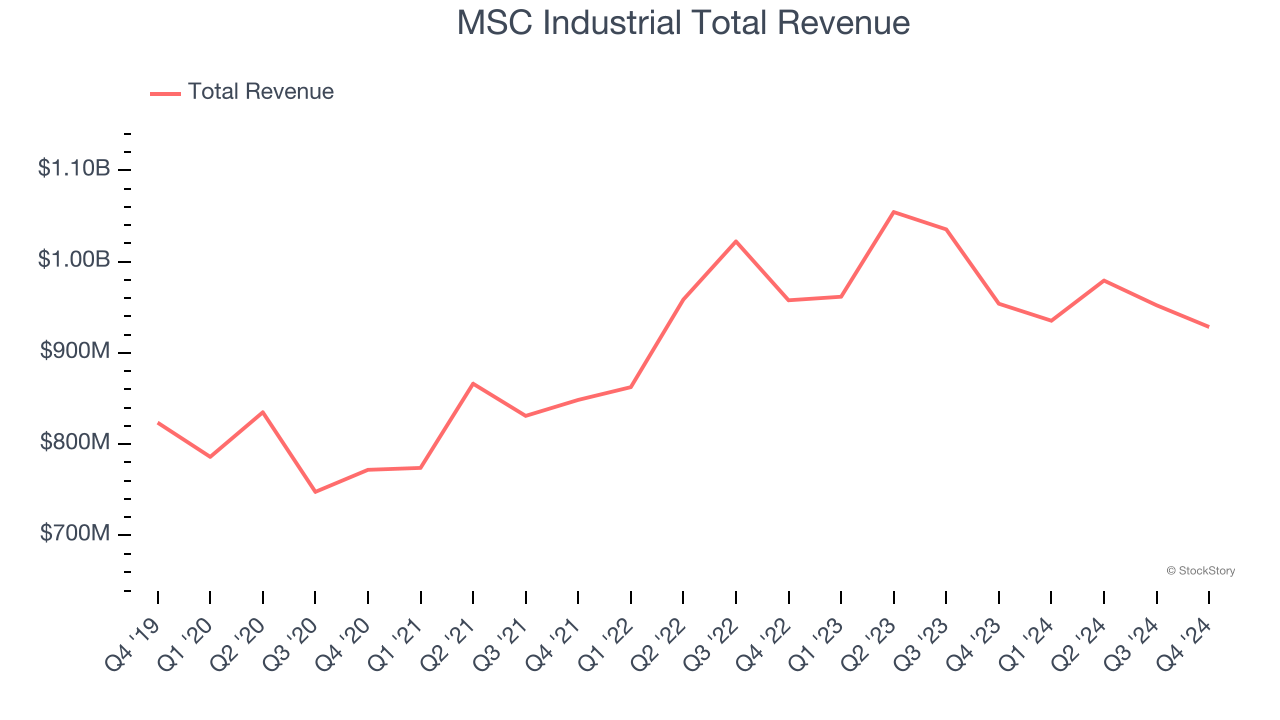

Best Q4: MSC Industrial (NYSE: MSM)

Founded in NYC’s Little Italy, MSC Industrial Direct (NYSE: MSM) provides industrial supplies and equipment, offering vast and reliable selection for customers such as contractors

MSC Industrial reported revenues of $928.5 million, down 2.7% year on year, outperforming analysts’ expectations by 2.7%. The business had a stunning quarter with a solid beat of analysts’ EBITDA estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 4.9% since reporting. It currently trades at $76.01.

Is now the time to buy MSC Industrial? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Transcat (NASDAQ: TRNS)

Serving the pharmaceutical, industrial manufacturing, energy, and chemical process industries, Transcat (NASDAQ: TRNS) provides measurement instruments and supplies.

Transcat reported revenues of $66.75 million, up 2.4% year on year, falling short of analysts’ expectations by 5%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

Transcat delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 27.9% since the results and currently trades at $71.71.

Read our full analysis of Transcat’s results here.

Fastenal (NASDAQ: FAST)

Founded in 1967, Fastenal (NASDAQ: FAST) provides industrial and construction supplies, including fasteners, tools, safety products, and many other product categories to businesses globally.

Fastenal reported revenues of $1.82 billion, up 3.7% year on year. This number came in 1% below analysts' expectations. Overall, it was a slower quarter as it also logged a significant miss of analysts’ adjusted operating income estimates.

The stock is flat since reporting and currently trades at $74.40.

Read our full, actionable report on Fastenal here, it’s free.

W.W. Grainger (NYSE: GWW)

Founded as a supplier of motors, W.W. Grainger (NYSE: GWW) provides maintenance, repair, and operating (MRO) supplies and services to businesses and institutions.

W.W. Grainger reported revenues of $4.23 billion, up 5.9% year on year. This result met analysts’ expectations. Zooming out, it was a slower quarter as it recorded full-year EPS and revenue guidance missing analysts’ expectations.

The stock is down 14.3% since reporting and currently trades at $965.

Read our full, actionable report on W.W. Grainger here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.