Jamf (JAMF): Buy, Sell, or Hold Post Q4 Earnings?

Jamf’s stock price has taken a beating over the past six months, shedding 31.9% of its value and falling to $11.55 per share. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Jamf, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why you should be careful with JAMF and a stock we'd rather own.

Why Is Jamf Not Exciting?

Founded in 2002 by Zach Halmstad and Chip Pearson, right around the time when Apple began to dominate the personal computing market, Jamf (NASDAQ: JAMF) provides software for companies to manage Apple devices such as Macs, iPads, and iPhones.

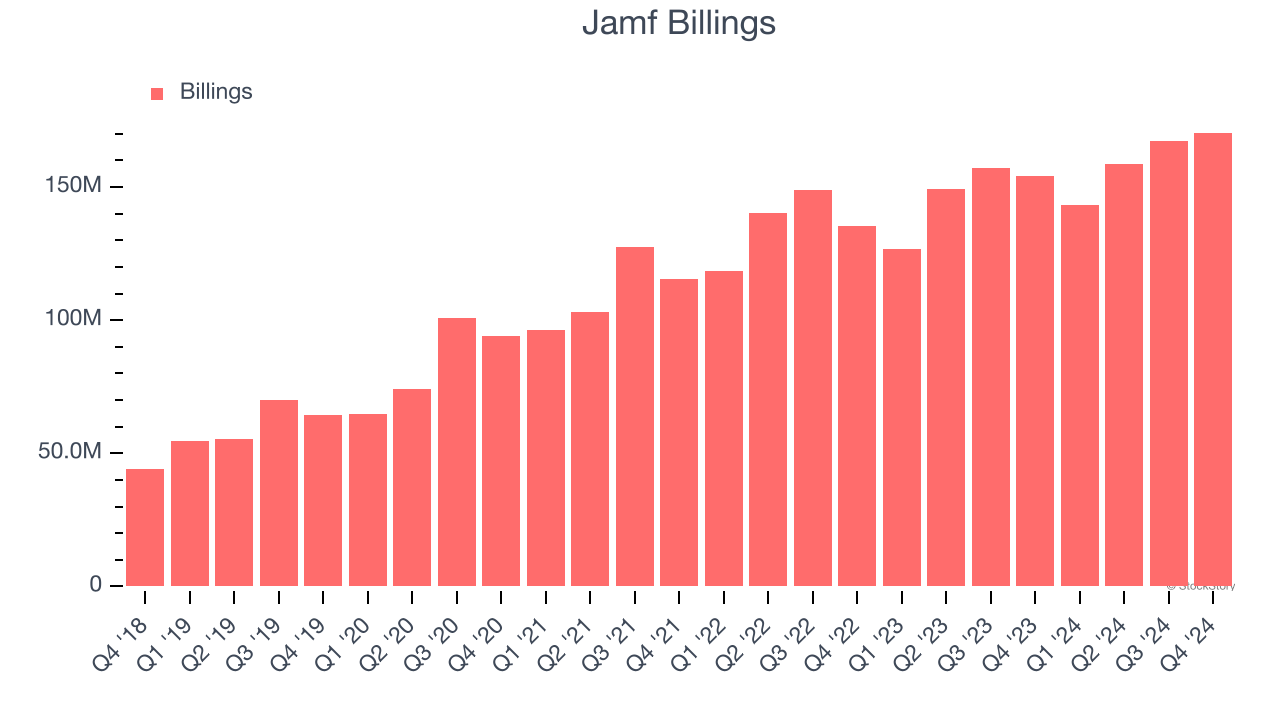

1. Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Jamf’s billings came in at $170.5 million in Q4, and over the last four quarters, its year-on-year growth averaged 9%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

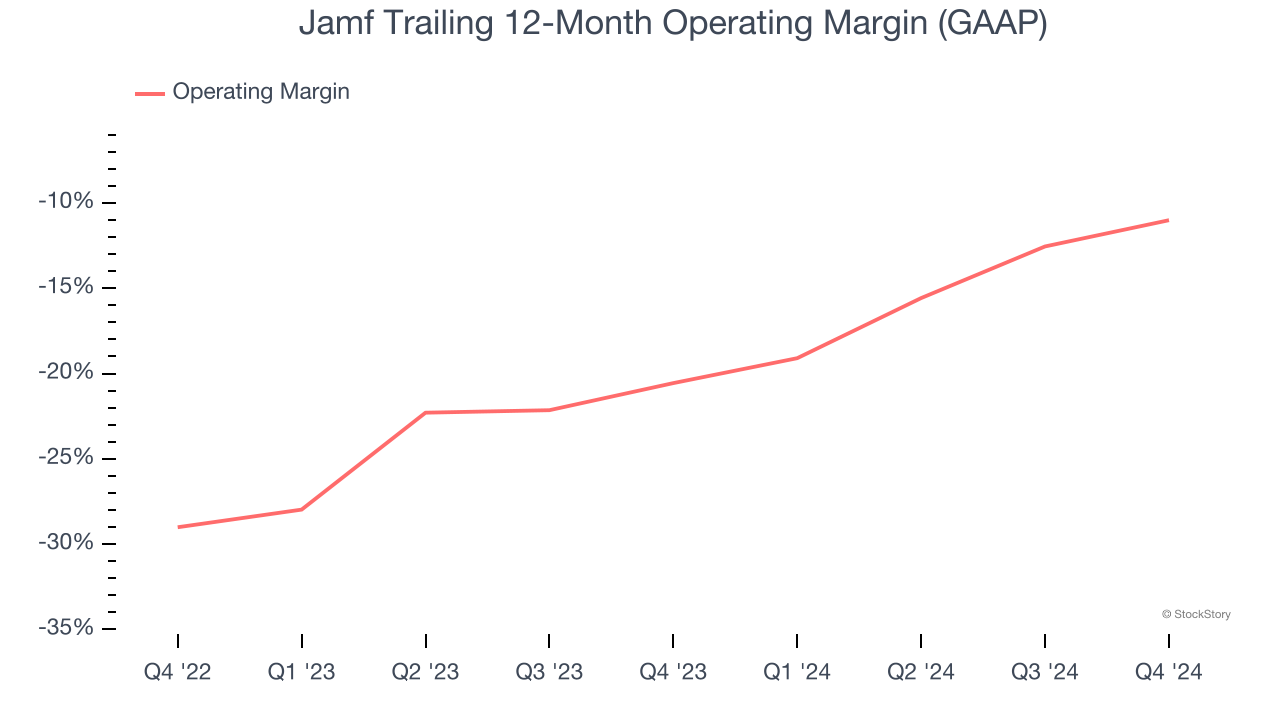

2. Operating Losses Sound the Alarms

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Jamf’s expensive cost structure has contributed to an average operating margin of negative 11% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Jamf reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

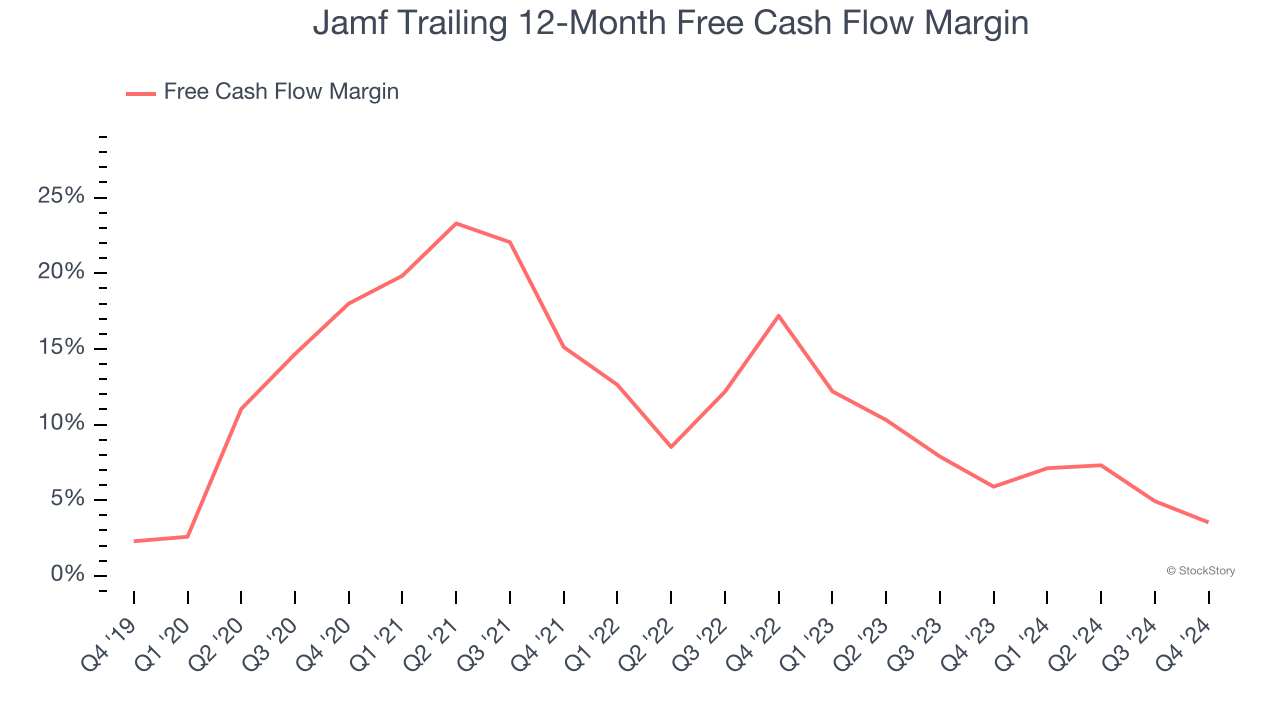

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Jamf has shown weak cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.5%, subpar for a software business.

Final Judgment

Jamf isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 2.1× forward price-to-sales (or $11.55 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of our top digital advertising picks.

Stocks We Like More Than Jamf

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.