OSI Systems (NASDAQ:OSIS) Exceeds Q1 Expectations

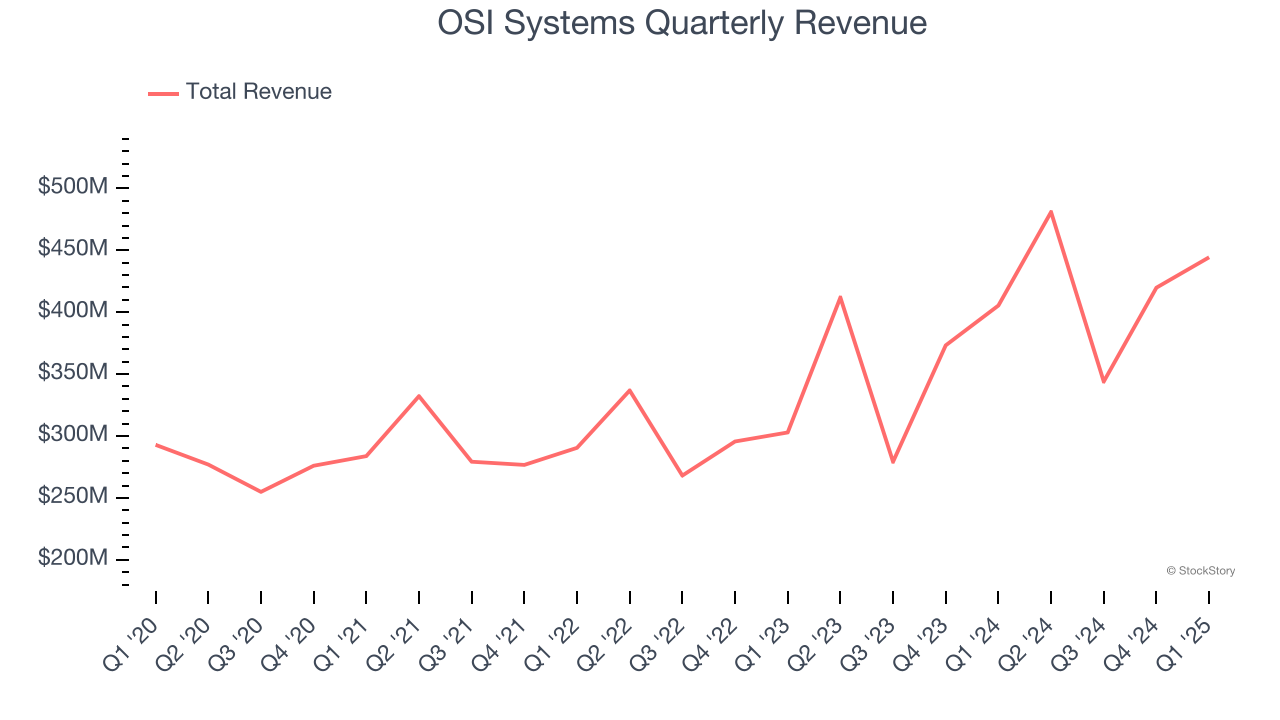

Security and healthcare technology company OSI Systems (NASDAQ: OSIS) announced better-than-expected revenue in Q1 CY2025, with sales up 9.6% year on year to $444.4 million. The company expects the full year’s revenue to be around $1.70 billion, close to analysts’ estimates. Its non-GAAP profit of $2.44 per share was 1.5% above analysts’ consensus estimates.

Is now the time to buy OSI Systems? Find out by accessing our full research report, it’s free.

OSI Systems (OSIS) Q1 CY2025 Highlights:

- Revenue: $444.4 million vs analyst estimates of $438.3 million (9.6% year-on-year growth, 1.4% beat)

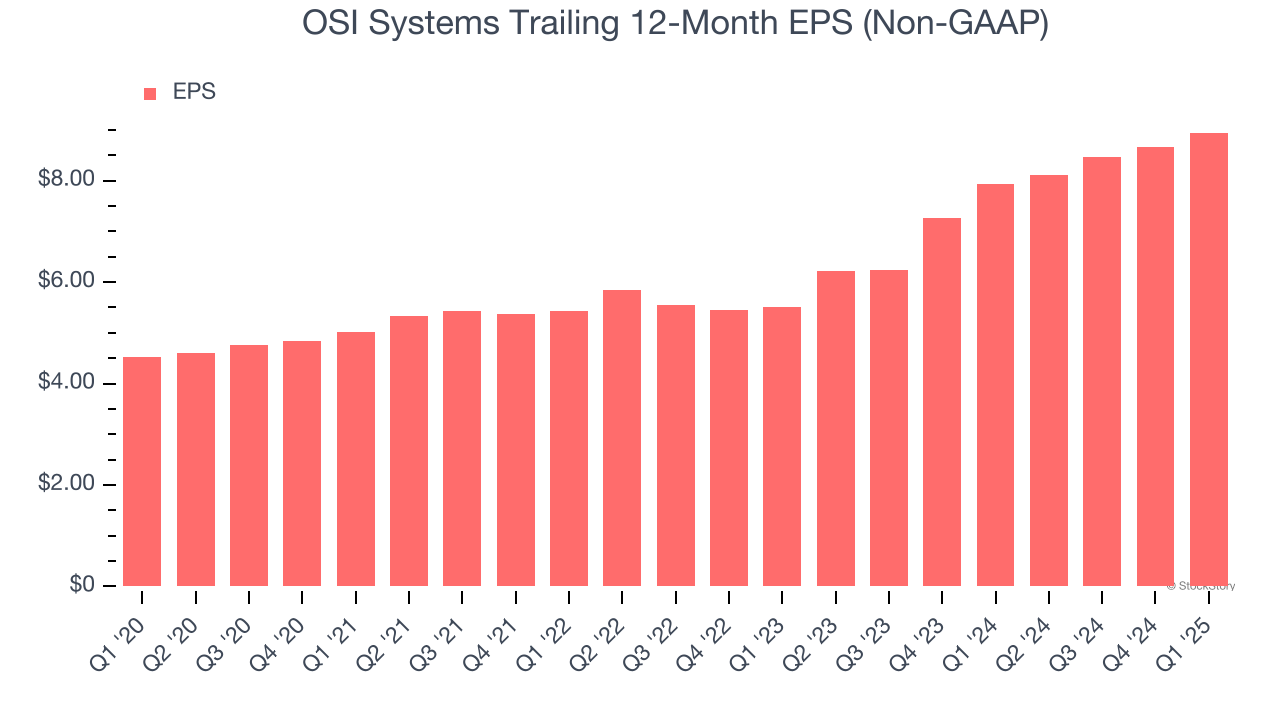

- Adjusted EPS: $2.44 vs analyst estimates of $2.40 (1.5% beat)

- The company slightly lifted its revenue guidance for the full year to $1.70 billion at the midpoint from $1.70 billion

- Management slightly raised its full-year Adjusted EPS guidance to $9.30 at the midpoint

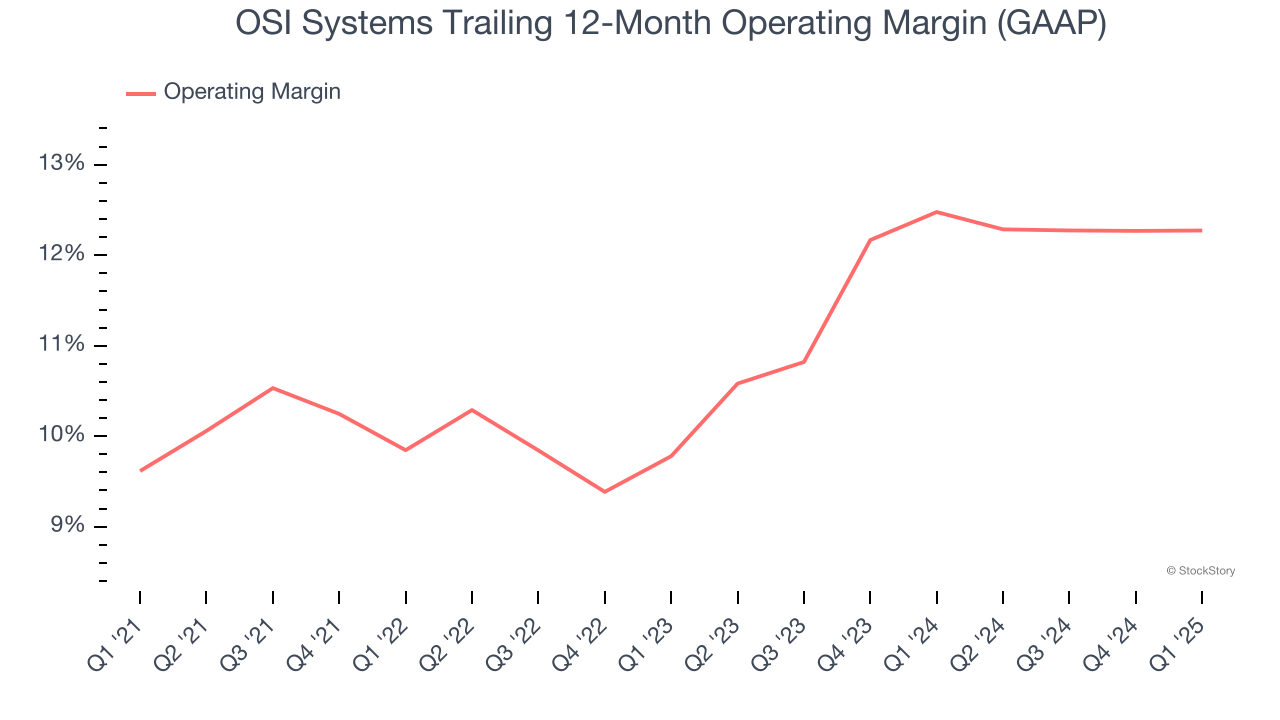

- Operating Margin: 12.7%, in line with the same quarter last year

- Backlog: $1.8 billion at quarter end

- Market Capitalization: $3.44 billion

Ajay Mehra, OSI Systems’ President and Chief Executive Officer, stated, “We are pleased to report a record-breaking third quarter for revenues, non-GAAP earnings and operating cash flow, led by excellent performance in the Security division and growth in the Optoelectronics and Manufacturing division. With record backlog and high visibility into our opportunity pipeline, we anticipate a strong finish to fiscal 2025.”

Company Overview

With security scanners deployed at airports and borders worldwide and patient monitors used in hospitals across the globe, OSI Systems (NASDAQ: OSIS) designs and manufactures specialized electronic systems for security screening, patient monitoring, and optoelectronic applications.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $1.69 billion in revenue over the past 12 months, OSI Systems is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

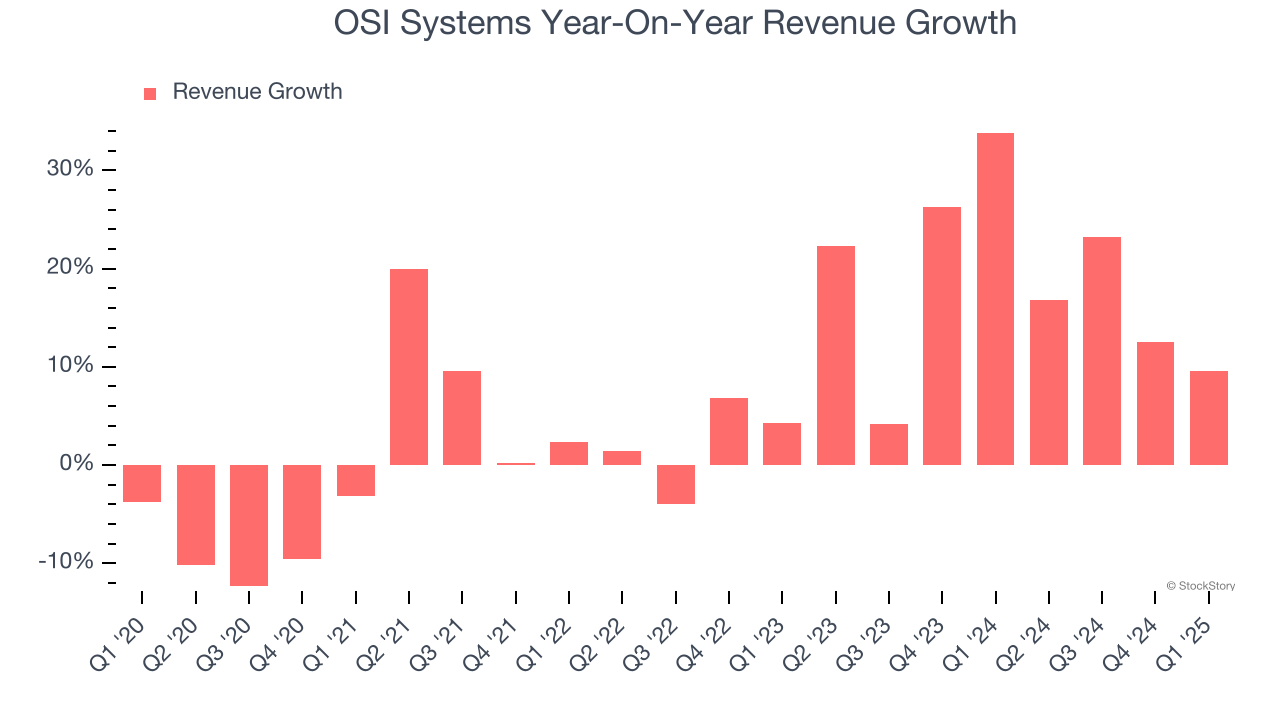

As you can see below, OSI Systems’s 7.1% annualized revenue growth over the last five years was solid. This is an encouraging starting point for our analysis because it shows OSI Systems’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. OSI Systems’s annualized revenue growth of 18.5% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

OSI Systems also breaks out the revenue for its most important segment, Security. Over the last two years, OSI Systems’s Security revenue (inspection systems) averaged 30.1% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, OSI Systems reported year-on-year revenue growth of 9.6%, and its $444.4 million of revenue exceeded Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

OSI Systems has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 11%, higher than the broader business services sector.

Analyzing the trend in its profitability, OSI Systems’s operating margin rose by 2.7 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, OSI Systems generated an operating profit margin of 12.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

OSI Systems’s EPS grew at a spectacular 14.6% compounded annual growth rate over the last five years, higher than its 7.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into OSI Systems’s earnings to better understand the drivers of its performance. As we mentioned earlier, OSI Systems’s operating margin was flat this quarter but expanded by 2.7 percentage points over the last five years. On top of that, its share count shrank by 7.3%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q1, OSI Systems reported EPS at $2.44, up from $2.16 in the same quarter last year. This print beat analysts’ estimates by 1.5%. Over the next 12 months, Wall Street expects OSI Systems’s full-year EPS of $8.95 to grow 12%.

Key Takeaways from OSI Systems’s Q1 Results

It was good to see OSI Systems narrowly top analysts’ revenue and EPS expectations this quarter. Overall, this print had some key positives. The stock traded up 3.9% to $212.72 immediately after reporting.

Should you buy the stock or not? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.