ZoomInfo (NASDAQ:ZI) Beats Q1 Sales Targets, Quarterly Revenue Guidance Slightly Exceeds Expectations

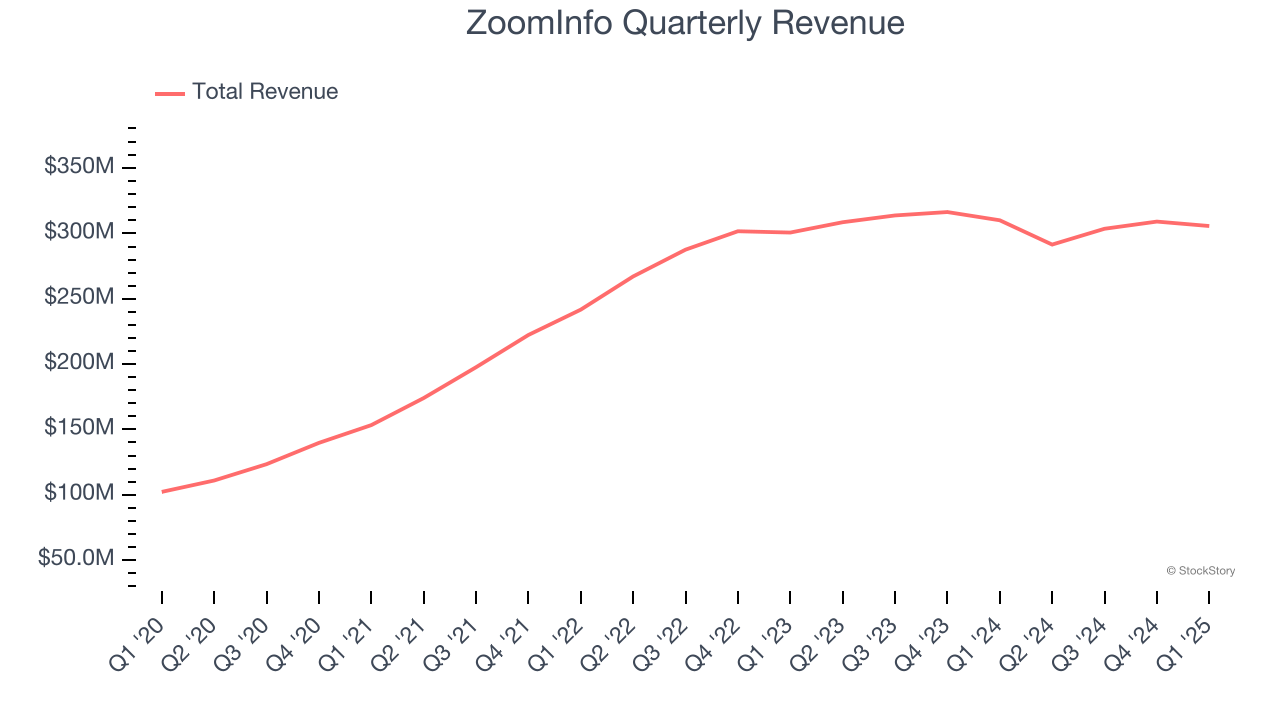

Sales intelligence platform ZoomInfo reported revenue ahead of Wall Street’s expectations in Q1 CY2025, but sales fell by 1.4% year on year to $305.7 million. Guidance for next quarter’s revenue was better than expected at $296.5 million at the midpoint, 1.5% above analysts’ estimates. Its non-GAAP profit of $0.23 per share was in line with analysts’ consensus estimates.

Is now the time to buy ZoomInfo? Find out by accessing our full research report, it’s free.

ZoomInfo (ZI) Q1 CY2025 Highlights:

- Revenue: $305.7 million vs analyst estimates of $295.5 million (1.4% year-on-year decline, 3.5% beat)

- Adjusted EPS: $0.23 vs analyst estimates of $0.22 (in line)

- Adjusted Operating Income: $100.9 million vs analyst estimates of $97.73 million (33% margin, 3.2% beat)

- The company slightly lifted its revenue guidance for the full year to $1.2 billion at the midpoint from $1.20 billion

- Management raised its full-year Adjusted EPS guidance to $0.97 at the midpoint, a 1% increase

- Operating Margin: 16.5%, up from 13.9% in the same quarter last year

- Free Cash Flow Margin: 40.7%, up from 30.3% in the previous quarter

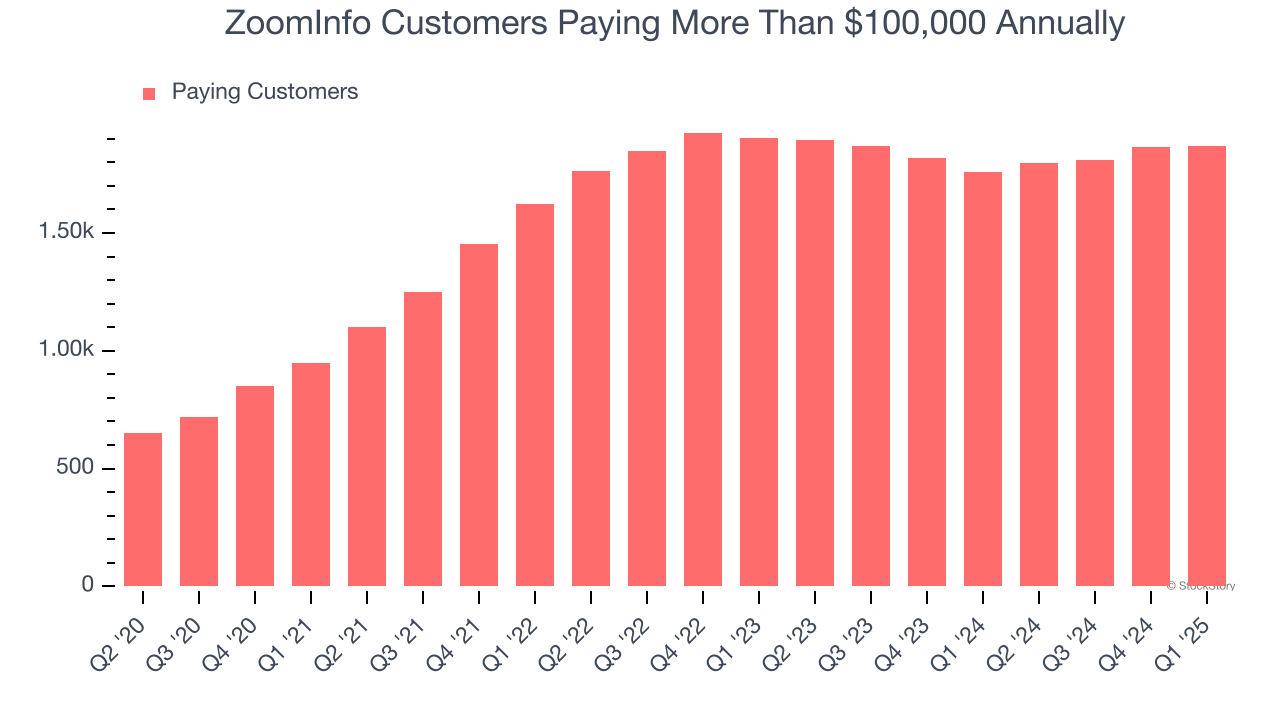

- Customers: 1,868 customers paying more than $100,000 annually

- Market Capitalization: $3.16 billion

“We delivered another quarter of better-than-expected financial results and Upmarket momentum,” said Henry Schuck, ZoomInfo Founder and CEO.

Company Overview

Founded in 2007 as DiscoveryOrg and renamed after a merger in 2019, ZoomInfo (NASDAQ: ZI) is a software as a service product that provides sales departments with access to a database of prospective clients.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, ZoomInfo grew its sales at a 13.1% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, ZoomInfo’s revenue fell by 1.4% year on year to $305.7 million but beat Wall Street’s estimates by 3.5%. Company management is currently guiding for a 1.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 1.2% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Enterprise Customer Base

This quarter, ZoomInfo reported 1,868 enterprise customers paying more than $100,000 annually, an increase of 1 from the previous quarter. That’s a bit fewer contract wins than last quarter and below what we’ve observed over the previous year, suggesting its sales momentum with new enterprise customers is slowing. It also implies that ZoomInfo will likely need to upsell its existing large customers or move down market to accelerate its top-line growth.

Key Takeaways from ZoomInfo’s Q1 Results

It was great to see ZoomInfo’s full-year EPS guidance top analysts’ expectations. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its new large contract wins slowed. Zooming out, we think this was a mixed quarter. The stock remained flat at $10.30 immediately after reporting.

So do we think ZoomInfo is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.