WesBanco’s (NASDAQ:WSBC) Q2 Sales Top Estimates

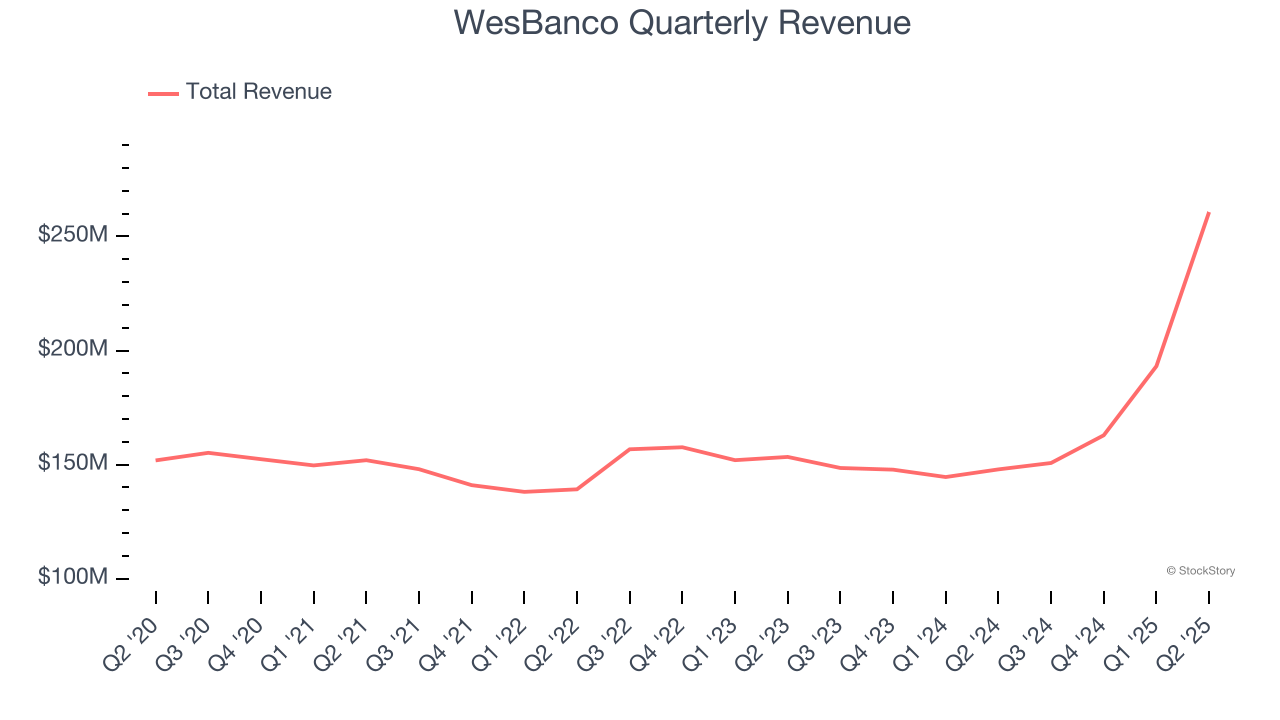

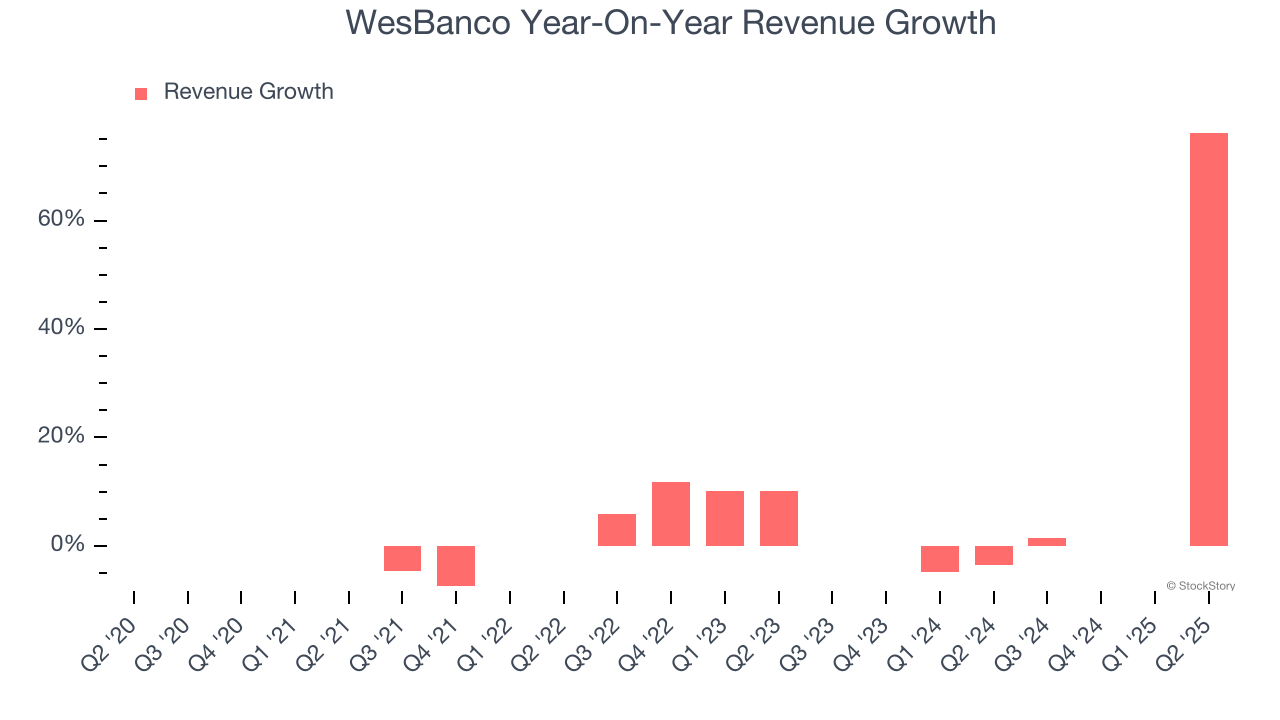

Regional banking company WesBanco (NASDAQ: WSBC) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 76.2% year on year to $260.7 million. Its non-GAAP profit of $0.91 per share was 6.5% above analysts’ consensus estimates.

Is now the time to buy WesBanco? Find out by accessing our full research report, it’s free.

WesBanco (WSBC) Q2 CY2025 Highlights:

- Net Interest Income: $216.8 million vs analyst estimates of $215.4 million (85.9% year-on-year growth, 0.6% beat)

- Net Interest Margin: 3.6% vs analyst estimates of 3.6% (64 basis point year-on-year increase, in line)

- Revenue: $260.7 million vs analyst estimates of $256.6 million (76.2% year-on-year growth, 1.6% beat)

- Efficiency Ratio: 55.5% vs analyst estimates of 55.5% (in line)

- Adjusted EPS: $0.91 vs analyst estimates of $0.85 (6.5% beat)

- Market Capitalization: $3.04 billion

"Our second quarter results demonstrate the success of our acquisition of Premier and strong operational performance. Our larger organization delivered solid sequential quarter loan growth while driving positive operating leverage. We also meaningfully improved both our net interest margin and efficiency ratio, further demonstrating our focus on operational excellence for our shareholders," said Jeff Jackson, President and Chief Executive Officer, WesBanco.

Company Overview

Tracing its roots back to 1870 in West Virginia, WesBanco (NASDAQ: WSBC) is a bank holding company that provides retail and commercial banking, trust services, insurance, and investment products through its subsidiaries across several Midwestern and Mid-Atlantic states.

Sales Growth

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

Luckily, WesBanco’s revenue grew at a decent 6.5% compounded annual growth rate over the last five years. Its growth was slightly above the average bank company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. WesBanco’s annualized revenue growth of 11.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, WesBanco reported magnificent year-on-year revenue growth of 76.2%, and its $260.7 million of revenue beat Wall Street’s estimates by 1.6%.

Net interest income made up 79.4% of the company’s total revenue during the last five years, meaning lending operations are WesBanco’s largest source of revenue.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Tangible Book Value Per Share (TBVPS)

Banks operate as balance sheet businesses, with profits generated through borrowing and lending activities. Valuations reflect this reality, emphasizing balance sheet strength and long-term book value compounding ability.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

WesBanco’s TBVPS was flat over the last five years. However, TBVPS growth has accelerated recently, growing by 1.3% annually over the last two years from $19.94 to $20.48 per share.

Over the next 12 months, Consensus estimates call for WesBanco’s TBVPS to grow by 11.1% to $22.75, solid growth rate.

Key Takeaways from WesBanco’s Q2 Results

It was encouraging to see WesBanco beat analysts’ revenue expectations this quarter. We were also happy its net interest income narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $31.82 immediately following the results.

So do we think WesBanco is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.