Bloomin' Brands (NASDAQ:BLMN) Exceeds Q2 Expectations

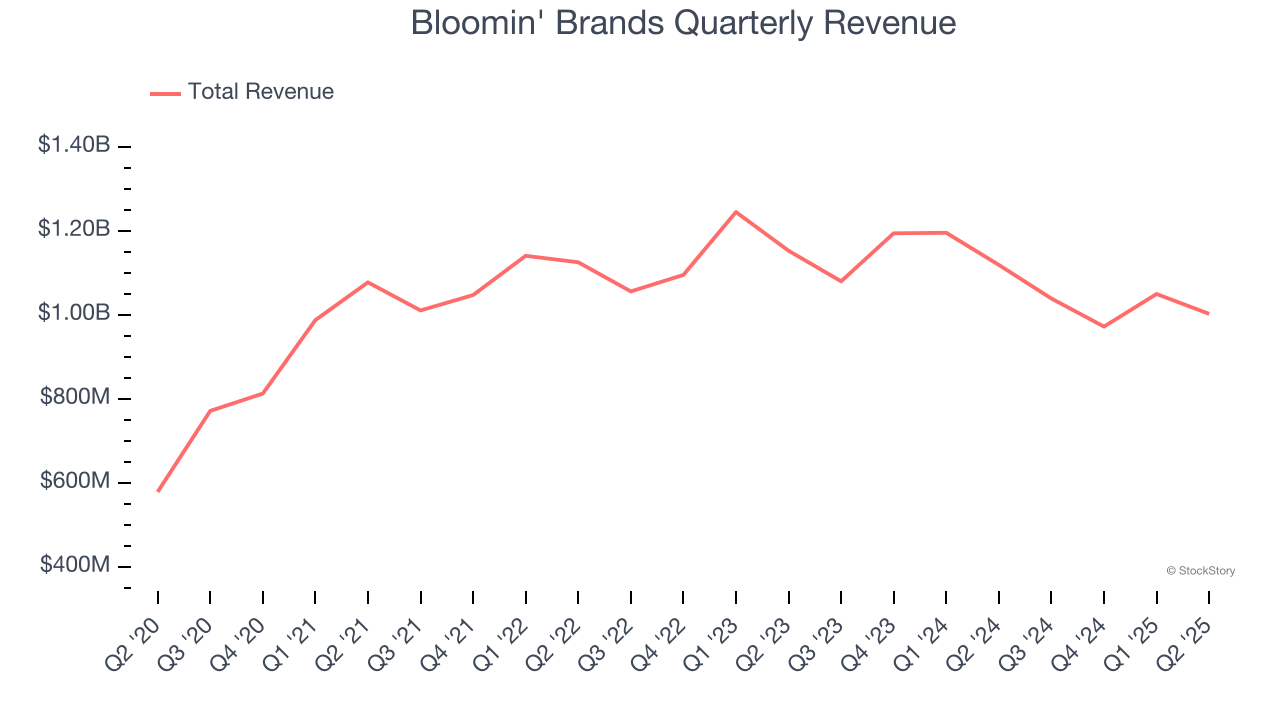

Restaurant company Bloomin’ Brands (NASDAQ: BLMN) beat Wall Street’s revenue expectations in Q2 CY2025, but sales fell by 10.4% year on year to $1.00 billion. Its non-GAAP profit of $0.32 per share was 9.7% above analysts’ consensus estimates.

Is now the time to buy Bloomin' Brands? Find out by accessing our full research report, it’s free.

Bloomin' Brands (BLMN) Q2 CY2025 Highlights:

- Revenue: $1.00 billion vs analyst estimates of $988.7 million (10.4% year-on-year decline, 1.4% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.29 (9.7% beat)

- Adjusted EPS guidance for the full year is $1.05 at the midpoint, missing analyst estimates by 14.8%

- Operating Margin: 3%, down from 4.1% in the same quarter last year

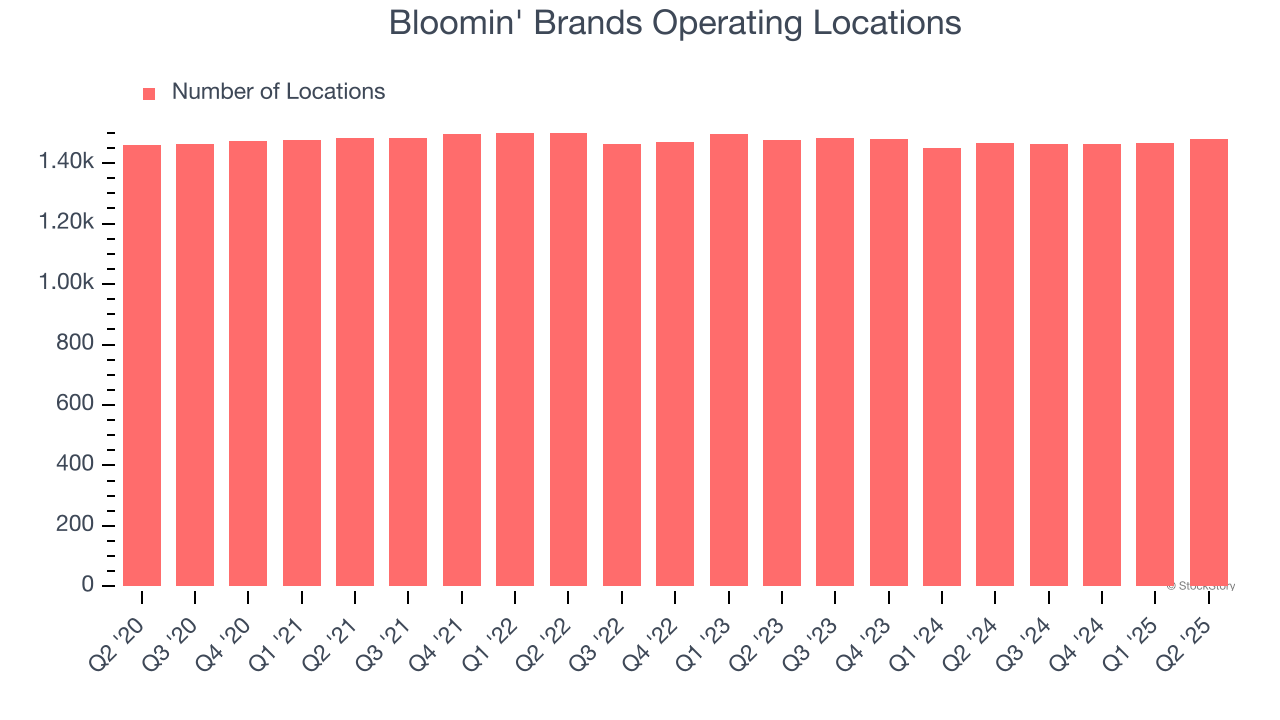

- Locations: 1,479 at quarter end, up from 1,465 in the same quarter last year

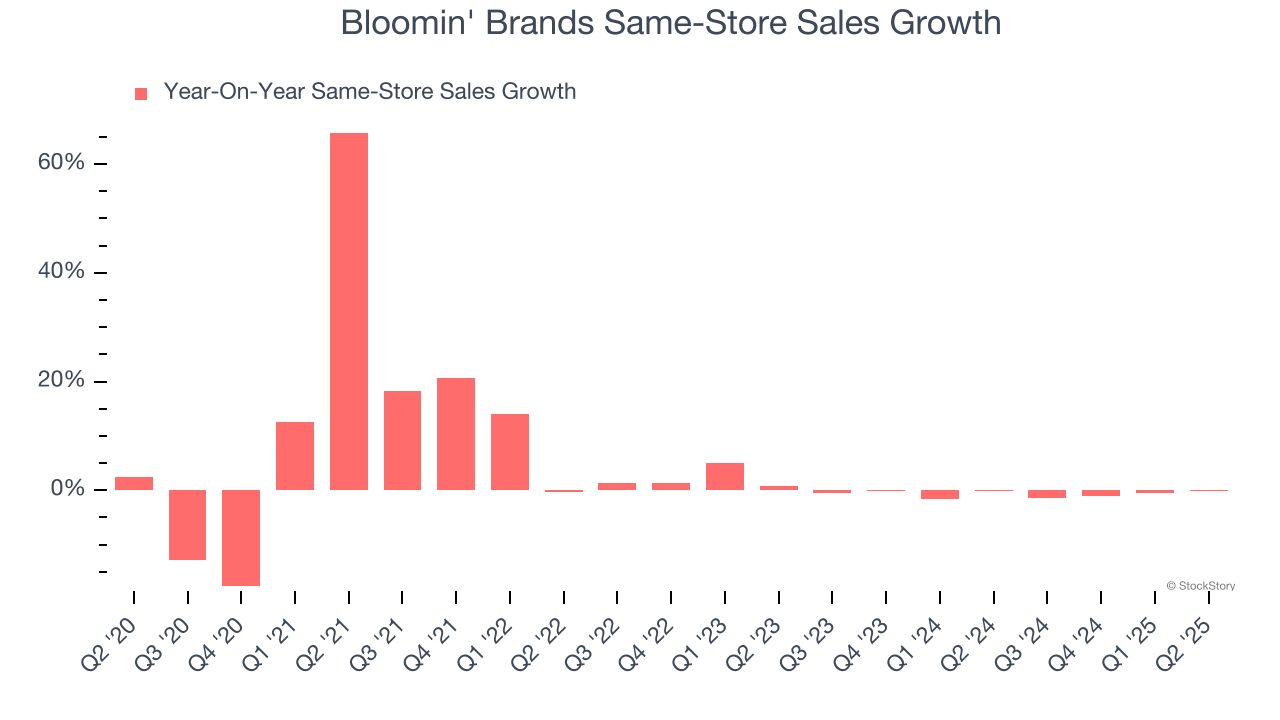

- Same-Store Sales were flat year on year, in line with the same quarter last year

- Market Capitalization: $761.3 million

TAMPA, Fla.--(BUSINESS WIRE)--Bloomin’ Brands, Inc. (Nasdaq: BLMN) announced the appointment of Rafael Sanchez as Senior Vice President & Chief Information Officer. Sanchez joins the company from Davidson Hospitality Group where he served as Senior Vice President of Information Technology. His appointment is effective June 30, 2025. “Rafael has a strong history in out-of-home entertainment and restaurants,” said Mike Spanos, CEO of Bloomin’ Brands,

Company Overview

Owner of the iconic Australian-themed Outback Steakhouse, Bloomin’ Brands (NASDAQ: BLMN) is a leading American restaurant company that owns and operates a portfolio of popular restaurant brands.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $4.06 billion in revenue over the past 12 months, Bloomin' Brands is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions. However, its scale is a double-edged sword because there are only a finite of number places to build restaurants, making it harder to find incremental growth. For Bloomin' Brands to boost its sales, it likely needs to adjust its prices, launch new chains, or lean into foreign markets.

As you can see below, Bloomin' Brands struggled to increase demand as its $4.06 billion of sales for the trailing 12 months was close to its revenue six years ago (we compare to 2019 to normalize for COVID-19 impacts). This was mainly because it didn’t open many new restaurants.

This quarter, Bloomin' Brands’s revenue fell by 10.4% year on year to $1.00 billion but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to decline by 2.4% over the next 12 months, a slight deceleration versus the last six years. This projection is underwhelming and implies its menu offerings will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations often determines how much revenue it can generate.

Bloomin' Brands operated 1,479 locations in the latest quarter, and over the last two years, has kept its restaurant count flat while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Bloomin' Brands’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Bloomin' Brands starts opening new restaurants to artificially boost revenue growth.

In the latest quarter, Bloomin' Brands’s year on year same-store sales were flat. This performance was more or less in line with its historical levels.

Key Takeaways from Bloomin' Brands’s Q2 Results

It was good to see Bloomin' Brands narrowly top analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.6% to $8.84 immediately after reporting.

Bloomin' Brands may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

If you believe this article contains misleading, harmful, or spam content, please let us know.

Report this articleMore News

View More

Recent Quotes

View MoreQuotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.