The Cheesecake Factory (CAKE): Buy, Sell, or Hold Post Q2 Earnings?

The Cheesecake Factory trades at $56.90 per share and has stayed right on track with the overall market, gaining 20.4% over the last six months. At the same time, the S&P 500 has returned 15.9%.

Is now the time to buy The Cheesecake Factory, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is The Cheesecake Factory Not Exciting?

We're sitting this one out for now. Here are three reasons you should be careful with CAKE and a stock we'd rather own.

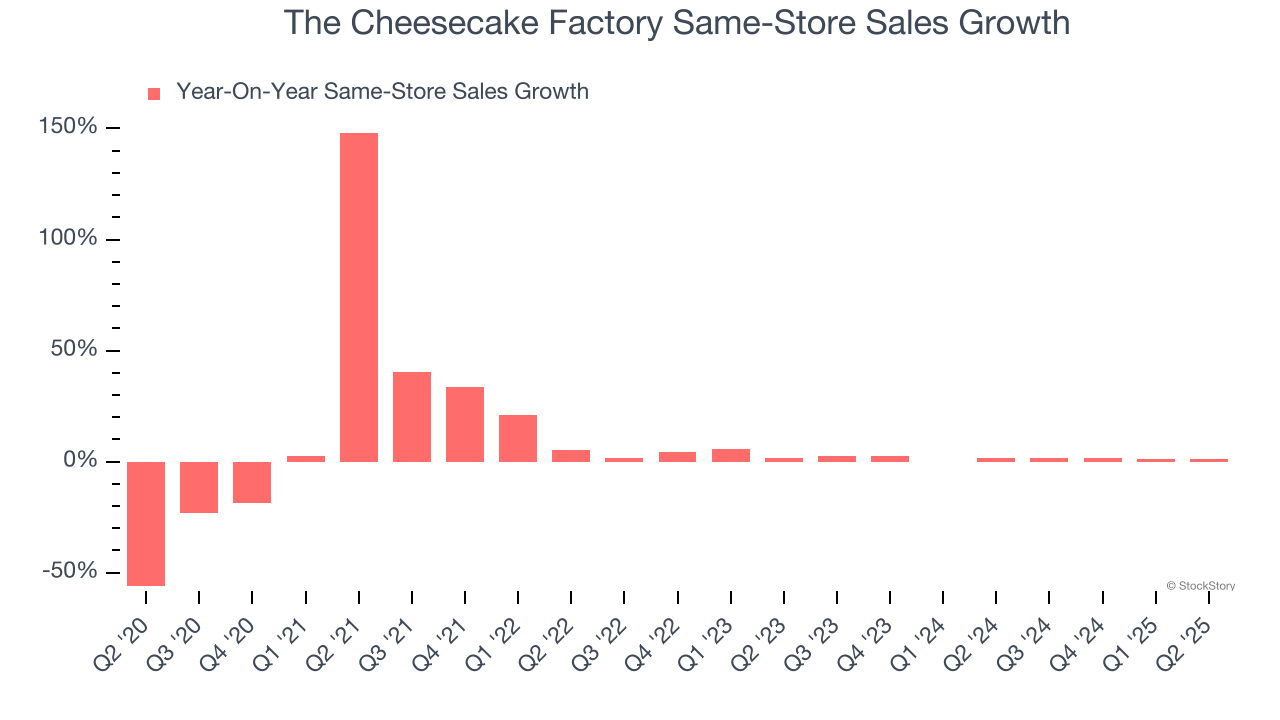

1. Same-Store Sales Falling Behind Peers

Same-store sales is a key performance indicator used to measure organic growth at restaurants open for at least a year.

The Cheesecake Factory’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.5% per year.

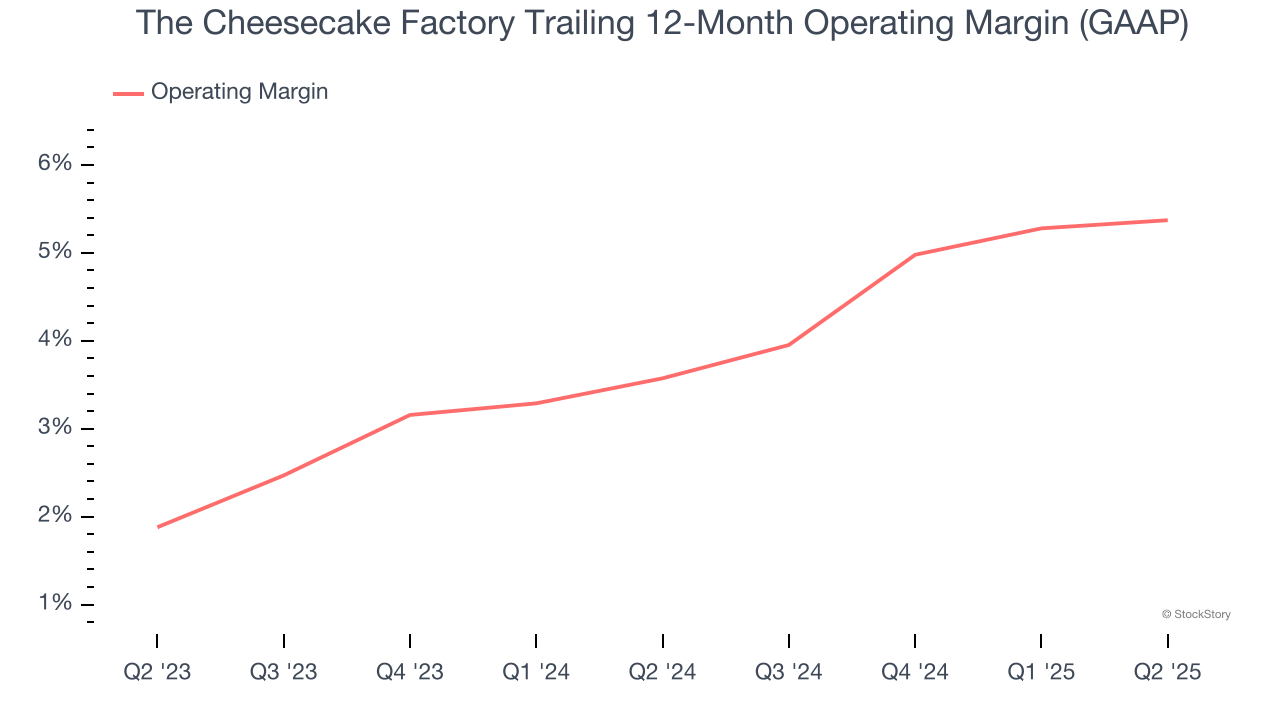

2. Weak Operating Margin Could Cause Trouble

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

The Cheesecake Factory was profitable over the last two years but held back by its large cost base. Its average operating margin of 4.5% was weak for a restaurant business. This result is surprising given its high gross margin as a starting point.

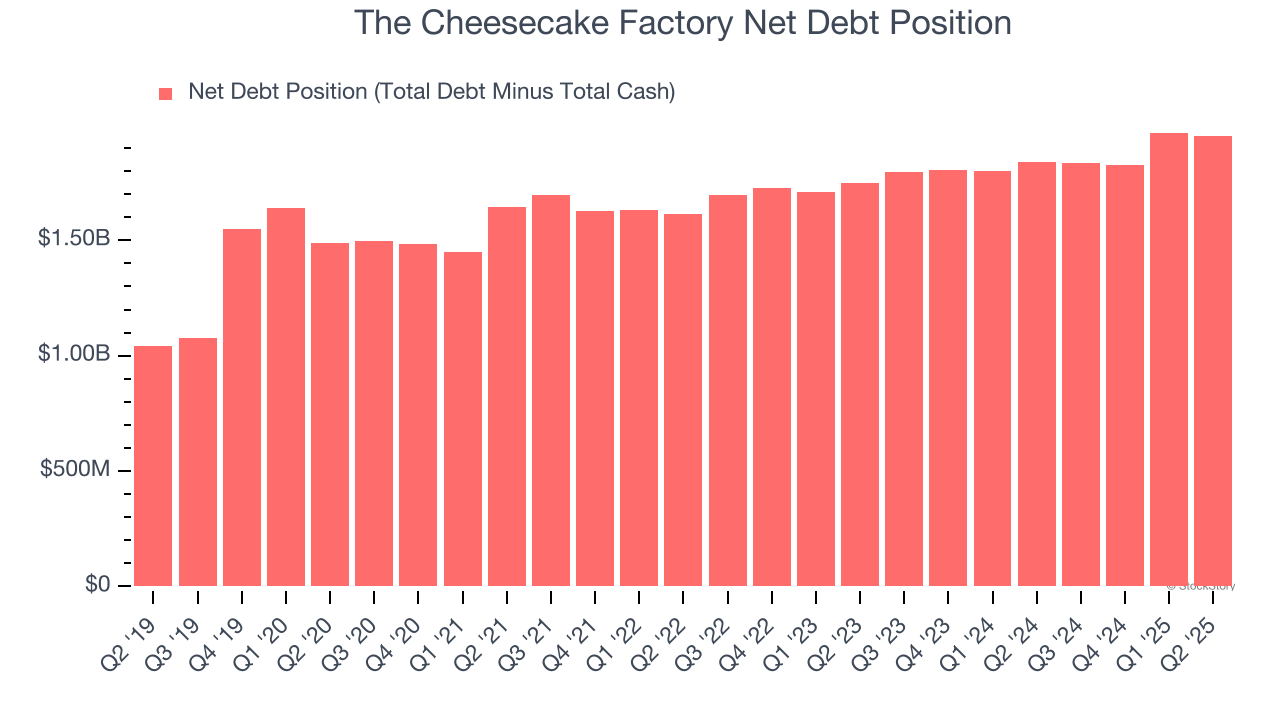

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

The Cheesecake Factory’s $2.10 billion of debt exceeds the $148.8 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $316.3 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. The Cheesecake Factory could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope The Cheesecake Factory can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

The Cheesecake Factory isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 14.4× forward P/E (or $56.90 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of The Cheesecake Factory

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.