Record GAAP and Adjusted Net Revenue for Second Quarter 2023

GAAP Net Revenue of $498 Million Up 37%; $489 Million Adjusted Net Revenue Up 37% Year-over-Year

Record Adjusted EBITDA of $77 Million Up 278% Year-over-Year

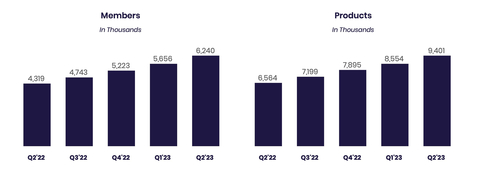

New Member Adds of Over 584,000; Quarter-End Total Members Up 44% Year-over-Year to Over 6.2 Million

New Product Adds of Nearly 847,000; Quarter-End Total Products Up 43% Year-over-Year to Over 9.4 Million Total Deposit Growth of $2.7 Billion, Up 26% During the Second Quarter to $12.7 Billion

Management Raises Full-Year 2023 Guidance

SoFi Technologies, Inc. (NASDAQ: SOFI), a member-centric, one-stop shop for digital financial services that helps members borrow, save, spend, invest and protect their money, reported financial results today for its second quarter ended June 30, 2023.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20230731284667/en/

Members (In Thousands), Products (In Thousands) (Graphic: Business Wire)

“We delivered another quarter of record financial results and generated our ninth consecutive quarter of record adjusted net revenue, which was up 37% year-over-year. Record revenue at the company level was driven by record revenue in both our Technology Platform business segment and our Financial Services business segment coupled with continued strong Lending business segment revenue growth. We also generated our fourth consecutive quarter of record adjusted EBITDA of $77 million, representing a 43% incremental adjusted EBITDA margin and a 16% margin overall, as well as a 36% incremental GAAP net income margin,” said Anthony Noto, CEO of SoFi Technologies, Inc.

Consolidated Results Summary |

|||||||||||

|

|

Three Months Ended June 30, |

|

|

|||||||

($ in thousands, except per share amounts) |

|

2023 |

|

2022 |

|

% Change | |||||

Consolidated – GAAP |

|

|

|

|

|

|

|||||

Total net revenue |

|

$ |

498,018 |

|

|

$ |

362,527 |

|

|

37 |

% |

Net loss |

|

|

(47,549 |

) |

|

|

(95,835 |

) |

|

(50 |

)% |

Net loss attributable to common stockholders – basic and diluted(1) |

|

|

(57,628 |

) |

|

|

(105,914 |

) |

|

(46 |

)% |

Loss per share attributable to common stockholders – basic and diluted |

|

|

(0.06 |

) |

|

|

(0.12 |

) |

|

(50 |

)% |

|

|

|

|

|

|

|

|||||

Consolidated – Non-GAAP |

|

|

|

|

|

|

|||||

Adjusted net revenue(2) |

|

$ |

488,815 |

|

|

$ |

356,091 |

|

|

37 |

% |

Adjusted EBITDA(2) |

|

|

76,819 |

|

|

|

20,304 |

|

|

278 |

% |

___________________

(1) |

Adjusted for the contractual amount of dividends payable to holders of Series 1 redeemable preferred stock, which are participating interests. |

|

(2) |

Adjusted net revenue and adjusted EBITDA are non-GAAP financial measures. For more information and reconciliations to the most comparable GAAP measures, see “Non-GAAP Financial Measures” and Table 2 to the “Financial Tables” herein. |

Noto continued: “Our record number of member additions and strong momentum in product and cross-buy adds, along with improving operating efficiency, reflects the benefits of our broad product suite and unique Financial Services Productivity Loop (FSPL) strategy. We added over 584,000 new members during the second quarter, and ended with over 6.2 million total members, up 44% year-over-year. We also added nearly 847,000 new products during the second quarter, and ended with over 9.4 million total products, a 43% annual increase.”

Noto concluded: “Total deposits grew by $2.7 billion, up 26% during the second quarter to $12.7 billion at quarter-end, and over 90% of SoFi Money deposits (inclusive of Checking and Savings and cash management accounts) are from direct deposit members. For new direct deposit accounts opened in the second quarter, the median FICO score was 747. More than half of newly funded SoFi Money accounts are setting up direct deposit by day 30, and this has had a significant impact on debit spending, with continued strong cross-buy trends from this attractive member base into Lending and other Financial Services products. With our launch of offering FDIC insurance of up to $2 million, nearly 98% of our deposits were insured at quarter end.

As a result of this growth in high quality deposits, we have benefited from a lower cost of funding for our loans. Our deposit funding also increases our flexibility to capture additional net interest margin (NIM) and optimize returns, a critical advantage in light of notable macro uncertainty. SoFi Bank, N.A. generated $63.1 million of GAAP net income at a 17% margin.”

Consolidated Results

Second quarter total GAAP net revenue increased 37% to $498.0 million from the prior-year period's $362.5 million. Second quarter adjusted net revenue of $488.8 million was up 37% from the same prior-year period's $356.1 million. Second quarter record adjusted EBITDA of $76.8 million increased 278% from the same prior year period's $20.3 million.

SoFi hit a number of key financial inflection points in the quarter, including adjusted EBITDA exceeding share-based compensation expense of $75.9 million for the second consecutive quarter. Additionally, SoFi improved contribution loss in the Financial Services segment to $4 million versus $24 million in the first quarter of 2023 and $54 million in the second quarter of 2022. The improvement in the Financial Services business segment contribution loss reinforces the company’s confidence in achieving positive contribution profit in all three business segments by year end, as well as overall GAAP profitability for the company for the fourth quarter of 2023. SoFi recorded a GAAP net loss of $47.5 million for the second quarter of 2023, an improvement from the prior-year period's net loss of $95.8 million.

Member and Product Growth

SoFi achieved strong year-over-year growth in both members and products in the second quarter of 2023. Record new member additions of over 584,000 brought total members to over 6.2 million by quarter-end, up over 1.9 million, or 44%, from the end of 2022's second quarter.

New product additions of nearly 847,000 in the second quarter brought total products to over 9.4 million at quarter-end, up 43% from 6.6 million at the same prior year quarter-end.

In the Financial Services segment, total products increased by 47% year-over-year, to 7.9 million from 5.4 million in the second quarter of 2022. SoFi Money (inclusive of Checking and Savings and cash management accounts) grew 47% year-over-year to 2.7 million products, SoFi Invest grew 18% year-over-year to 2.3 million products, and SoFi Relay grew 90% year-over-year to 2.6 million products.

Lending products increased 25% year-over-year to 1.5 million products, driven primarily by continued record growth in personal loans.

Technology Platform enabled accounts increased by 11% year-over-year to 129.4 million.

Lending Segment Results

Lending segment GAAP and adjusted net revenues were $331.4 million and $322.2 million, respectively, for the second quarter of 2023, both up 29% compared to the second quarter of 2022. Higher loan balances and net interest margin expansion drove strong growth in net interest income.

Lending segment second quarter contribution profit of $183.3 million increased 29% from $142.0 million in the same prior-year period. Contribution margin using Lending adjusted net revenue remained healthy at 57% in both the second quarter of 2023 and the same prior-year period. These advances reflect SoFi’s ability to capitalize on continued strong demand for its lending products.

Lending – Segment Results of Operations |

|||||||||||

|

|

Three Months Ended June 30, |

|

|

|||||||

($ in thousands) |

|

2023 |

|

2022 |

|

% Change |

|||||

Net interest income |

|

$ |

231,885 |

|

|

$ |

114,003 |

|

|

103 |

% |

Noninterest income |

|

|

99,556 |

|

|

|

143,114 |

|

|

(30 |

)% |

Total net revenue – Lending |

|

|

331,441 |

|

|

|

257,117 |

|

|

29 |

% |

Servicing rights – change in valuation inputs or assumptions |

|

|

(8,601 |

) |

|

|

(9,098 |

) |

|

(5 |

)% |

Residual interests classified as debt – change in valuation inputs or assumptions |

|

|

(602 |

) |

|

|

2,662 |

|

|

n/m |

|

Directly attributable expenses |

|

|

(138,929 |

) |

|

|

(108,690 |

) |

|

28 |

% |

Contribution Profit |

|

$ |

183,309 |

|

|

$ |

141,991 |

|

|

29 |

% |

|

|

|

|

|

|

|

|||||

Adjusted net revenue – Lending(1) |

|

$ |

322,238 |

|

|

$ |

250,681 |

|

|

29 |

% |

___________________

(1) |

Adjusted net revenue – Lending represents a non-GAAP financial measure. For more information and a reconciliation to the most comparable GAAP measure, see “Non-GAAP Financial Measures” and Table 2 to the “Financial Tables” herein. |

Lending – Loans Held for Sale |

|||||||||||||

|

Personal Loans |

|

Student Loans |

|

Home Loans |

|

Total |

||||||

June 30, 2023 |

|

|

|

|

|

|

|

||||||

Unpaid principal |

$ |

12,171,935 |

|

$ |

5,262,975 |

|

$ |

87,928 |

|

|

$ |

17,522,838 |

|

Accumulated interest |

|

82,868 |

|

|

21,164 |

|

|

150 |

|

|

|

104,182 |

|

Cumulative fair value adjustments(1) |

|

496,360 |

|

|

99,782 |

|

|

(9,495 |

) |

|

|

586,647 |

|

Total fair value of loans(2) |

$ |

12,751,163 |

|

$ |

5,383,921 |

|

$ |

78,583 |

|

|

$ |

18,213,667 |

|

March 31, 2023 |

|

|

|

|

|

|

|

||||||

Unpaid principal |

$ |

10,039,769 |

|

$ |

5,086,953 |

|

$ |

89,782 |

|

|

$ |

15,216,504 |

|

Accumulated interest |

|

69,049 |

|

|

20,787 |

|

|

162 |

|

|

|

89,998 |

|

Cumulative fair value adjustments(1) |

|

428,181 |

|

|

132,319 |

|

|

(8,897 |

) |

|

|

551,603 |

|

Total fair value of loans(2) |

$ |

10,536,999 |

|

$ |

5,240,059 |

|

$ |

81,047 |

|

|

$ |

15,858,105 |

|

___________________

(1) |

The cumulative fair value adjustments for personal loans during the three months ended June 30, 2023 were primarily impacted by higher origination volume, partially offset by lower fair value marks driven primarily by a higher discount rate, while the cumulative fair value adjustments for student loans were primarily impacted by a higher weighted average discount rate and higher prepayment rate assumption, which also resulted in lower fair value marks. |

|

(2) |

Each component of the fair value of loans is impacted by charge-offs during the period. Our fair value assumption for annual default rate incorporates fair value markdowns on loans beginning when they are 10 days or more delinquent, with additional markdowns at 30, 60 and 90 days past due. |

The following table summarizes the significant inputs to the fair value model for personal and student loans:

|

Personal Loans |

|

Student Loans |

|||||||||

|

June 30, 2023 |

|

March 31, 2023 |

|

June 30, 2023 |

|

March 31, 2023 |

|||||

Weighted average coupon rate(1) |

13.6 |

% |

|

13.2 |

% |

|

5.0 |

% |

|

4.9 |

% |

|

Weighted average annual default rate |

4.6 |

|

|

4.6 |

|

|

0.5 |

|

|

0.4 |

|

|

Weighted average conditional prepayment rate |

19.0 |

|

|

19.1 |

|

|

10.6 |

|

|

10.4 |

|

|

Weighted average discount rate |

6.1 |

|

|

5.5 |

|

|

4.4 |

|

|

4.1 |

|

|

___________________

(1) |

Represents the average coupon rate on loans held on balance sheet, weighted by unpaid principal balance outstanding at the balance sheet date. |

Second quarter Lending segment total origination volume increased 37% year-over-year, as a result of continued strong demand for personal loans.

Record personal loan originations of over $3.7 billion in the second quarter of 2023 were up $1.3 billion, or 51%, year-over-year, and rose 27% sequentially. This strong performance was aided by years of investment in technology to automate and accelerate the application-to-approval process for qualified borrowers and constant testing of risk controls and underwriting models to maintain high credit quality and strong returns. Second quarter student loan volume of over $395 million continued to reflect the uncertainty around federal student loan payments. Second quarter home loan volume of over $243 million was down 27% year-over-year, but nearly tripled sequentially, as we began to benefit from the technology platform and overall loan capacity from our acquisition at the beginning of the quarter.

Lending – Originations and Average Balances |

|||||||||

|

|

Three Months Ended June 30, |

|

||||||

|

|

2023 |

|

2022 |

|

% Change |

|||

Origination volume ($ in thousands, during period) |

|

|

|

|

|

|

|||

Personal loans |

|

$ |

3,740,981 |

|

$ |

2,471,849 |

|

51 |

% |

Student loans |

|

|

395,367 |

|

|

398,722 |

|

(1 |

)% |

Home loans |

|

|

243,123 |

|

|

332,047 |

|

(27 |

)% |

Total |

|

$ |

4,379,471 |

|

$ |

3,202,618 |

|

37 |

% |

|

|

|

|

|

|

|

|||

Average loan balance ($, as of period end)(1) |

|

|

|

|

|

|

|||

Personal loans |

|

$ |

23,767 |

|

$ |

24,421 |

|

(3 |

)% |

Student loans |

|

|

45,523 |

|

|

48,474 |

|

(6 |

)% |

Home loans |

|

|

277,077 |

|

|

287,205 |

|

(4 |

)% |

_________________

(1) |

Within each loan product category, average loan balance is defined as the total unpaid principal balance of the loans divided by the number of loans that have a balance greater than zero dollars as of the reporting date. Average loan balance includes loans on the balance sheet and transferred loans with which SoFi has a continuing involvement through its servicing agreements. |

Lending – Products |

|

June 30, |

|

|

|||

|

|

2023 |

|

2022 |

|

% Change |

|

Personal loans |

|

985,396 |

|

714,735 |

|

38 |

% |

Student loans |

|

491,499 |

|

462,164 |

|

6 |

% |

Home loans |

|

26,997 |

|

25,128 |

|

7 |

% |

Total lending products |

|

1,503,892 |

|

1,202,027 |

|

25 |

% |

Technology Platform Segment Results

Technology Platform segment record net revenue of $87.6 million for the second quarter of 2023 increased 4% year-over-year and 13% sequentially, and includes strong contribution from Galileo, which had 9% sequential revenue growth, and continued strong contribution from Technisys, which had 21% sequential revenue growth. Contribution profit of $17.2 million decreased 21% year-over-year, for a margin of 20%, which improved modestly from the prior quarter. We are seeing strong adoption of new products, including Konecta, our AI natural language customer service bot, and our Payments Risk Platform (PRP), a platform which leverages transactional data to reduce transaction fraud.

Technology Platform – Segment Results of Operations |

|||||||||||

|

|

Three Months Ended June 30, |

|

|

|||||||

($ in thousands) |

|

2023 |

|

2022 |

|

% Change |

|||||

Total net revenue – Technology Platform |

|

$ |

87,623 |

|

|

$ |

83,899 |

|

|

4 |

% |

Directly attributable expenses |

|

|

(70,469 |

) |

|

|

(62,058 |

) |

|

14 |

% |

Contribution Profit |

|

$ |

17,154 |

|

|

$ |

21,841 |

|

|

(21 |

)% |

Technology Platform total enabled client accounts increased 11% year-over-year, to 129.4 million from 116.6 million. We have made great progress on our strategy to sign larger, more durable clients. Galileo signed 5 new clients in the second quarter of 2023, all of which have existing installed bases, and Technisys went live with 4 new clients. Additionally, we have a robust pipeline of ongoing discussions with potential partners with large existing customer bases across both the U.S. and Latin America spanning both the financial services and non-financial services segments.

Technology Platform |

|

June 30, |

|

|

|||

|

|

2023 |

|

2022 |

|

% Change |

|

Total accounts |

|

129,356,203 |

|

116,570,038 |

|

11 |

% |

Financial Services Segment Results

Financial Services segment record net revenue increased 223% in the second quarter of 2023 to $98.1 million from the prior year period's total of $30.4 million, helped by 188% growth in segment interchange revenue and 477% growth in net interest income. Strength in the segment results was driven by SoFi Money along with contributions from SoFi Invest, SoFi Protect, SoFi Credit Card, and lending-as-a-service.

Importantly, Financial Services segment contribution loss was $4.3 million, reflecting a $49.4 million improvement over the prior-year quarter's $53.7 million loss, as well as our second consecutive quarter of positive variable profit in the segment. This came as a result of continued improvement in monetization for the segment, along with increasing operating leverage as we efficiently scale the business. Annualized revenue per product of $50 more than doubled year-over-year and grew 9% sequentially.

Financial Services – Segment Results of Operations |

|||||||||||

|

|

Three Months Ended June 30, |

|

|

|||||||

($ in thousands) |

|

2023 |

|

2022 |

|

% Change |

|||||

Net interest income |

|

$ |

74,637 |

|

|

$ |

12,925 |

|

|

477 |

% |

Noninterest income |

|

|

23,415 |

|

|

|

17,438 |

|

|

34 |

% |

Total net revenue – Financial Services |

|

|

98,052 |

|

|

|

30,363 |

|

|

223 |

% |

Directly attributable expenses |

|

|

(102,399 |

) |

|

|

(84,063 |

) |

|

22 |

% |

Contribution loss |

|

$ |

(4,347 |

) |

|

$ |

(53,700 |

) |

|

(92 |

)% |

By continuously innovating with new and relevant offerings, features and rewards for members, SoFi grew total Financial Services products by 2.5 million, or 47%, year-over-year in the second quarter of 2023, bringing the total to 7.9 million at quarter-end. In the second quarter of 2023, SoFi Money products increased by over 280,000, SoFi Invest products increased by nearly 105,000 and Relay products increased by over 347,000.

Most notably, our Checking and Savings offering has an APY of up to 4.40% as of July 31, 2023, no minimum balance requirement nor balance limits, a host of free features and a unique rewards program. Total deposits grew 26% during the second quarter to $12.7 billion at quarter-end, and over 90% of SoFi Money deposits (inclusive of Checking and Savings and cash management accounts) are from direct deposit members. More than half of newly funded SoFi Money accounts were setting up direct deposit by day 30 in the second quarter of 2023.

Financial Services – Products |

|

June 30, |

|

|

|||

|

|

2023 |

|

2022 |

|

% Change |

|

Money(1) |

|

2,693,148 |

|

1,837,138 |

|

47 |

% |

Invest |

|

2,315,777 |

|

1,961,425 |

|

18 |

% |

Credit Card |

|

213,395 |

|

139,781 |

|

53 |

% |

Referred loans(2) |

|

47,439 |

|

28,037 |

|

69 |

% |

Relay |

|

2,553,158 |

|

1,344,538 |

|

90 |

% |

At Work |

|

74,216 |

|

51,228 |

|

45 |

% |

Total financial services products |

|

7,897,133 |

|

5,362,147 |

|

47 |

% |

___________________

(1) |

Includes SoFi Checking and Savings accounts held at SoFi Bank, and cash management accounts. |

|

(2) |

Limited to loans wherein we provide third party fulfillment services. |

Guidance and Outlook

Management expects to generate $1.025 to $1.085 billion of adjusted net revenue in the second half of 2023, up 19% to 26% year-over-year, and $180 to $190 million of adjusted EBITDA.

For the full year 2023, management expects adjusted net revenue of $1.974 to $2.034 billion, up from its prior guidance of $1.955 to $2.02 billion, and full-year adjusted EBITDA of $333 to $343 million, up from its prior guidance of $268 to $288 million, representing a 40-44% incremental adjusted EBITDA margin. Management projects that a more significant portion of the second half adjusted net revenue and adjusted EBITDA results will be generated during the fourth quarter. As the company moves toward expected GAAP net income profitability in the fourth quarter, management expects share-based compensation and depreciation and amortization expenses to be slightly higher than reported second quarter 2023 levels in both the third and fourth quarters of the year.

Management will further address second half and full-year 2023 guidance on the quarterly earnings conference call. Management has not reconciled forward-looking non-GAAP measures to their most directly comparable GAAP measures of total net revenue, net income and gross margin. This is because the company cannot predict with reasonable certainty and without unreasonable efforts the ultimate outcome of certain GAAP components of such reconciliations due to market-related assumptions that are not within our control as well as certain legal or advisory costs, tax costs or other costs that may arise. For these reasons, management is unable to assess the probable significance of the unavailable information, which could materially impact the amount of the future directly comparable GAAP measures.

Earnings Webcast

SoFi’s executive management team will host a live audio webcast beginning at 8:00 a.m. Eastern Time (5:00 a.m. Pacific Time) today to discuss the quarter’s financial results and business highlights. All interested parties are invited to listen to the live webcast at https://investors.sofi.com. A replay of the webcast will be available on the SoFi Investor Relations website for 30 days. Investor information, including supplemental financial information, is available on SoFi’s Investor Relations website at https://investors.sofi.com.

Cautionary Statement Regarding Forward-Looking Statements

Certain of the statements above are forward-looking and as such are not historical facts. This includes, without limitation, statements regarding our expectations for the second half of 2023 and full year adjusted net revenue and adjusted EBITDA, our expectations regarding the profitability of our three business segments, our expectations regarding our ability to continue to grow our business, improve our financials and increase our member, product and total accounts count, our ability to navigate the macroeconomic environment and the financial position, business strategy and plans and objectives of management for our future operations. These forward-looking statements are not guarantees of performance. Such statements can be identified by the fact that they do not relate strictly to historical or current facts. Words such as “continue”, “expect”, “may”, “strategy”, “will be”, “will continue”, and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Factors that could cause actual results to differ materially from those contemplated by these forward-looking statements include: (i) the effect of and uncertainties related to macroeconomic factors such as fluctuating inflation and interest rates; (ii) our ability to achieve profitability, operating efficiencies and continued growth across our three businesses in the future, as well as our ability to achieve GAAP net income profitability in the fourth quarter of 2023 and expected GAAP net income margins; (iii) the impact on our business of the regulatory environment and complexities with compliance related to such environment, including any impact on our Lending segment of the ending of the federal student loan payment moratorium or loan forgiveness; (iv) our ability to realize the benefits of being a bank holding company and operating SoFi Bank, including continuing to grow high quality deposits and our rewards program for members; (v) our ability to respond and adapt to changing market and economic conditions, including recessionary pressures, inflationary pressures and interest rates; (vi) our ability to continue to drive brand awareness and realize the benefits or our integrated multi-media marketing and advertising campaigns; (vii) our ability to vertically integrate our businesses and accelerate the pace of innovation of our financial products; (viii) our ability to manage our growth effectively and our expectations regarding the development and expansion of our business; (ix) our ability to access sources of capital on acceptable terms or at all, including debt financing and other sources of capital to finance operations and growth; (x) the success of our continued investments in our Financial Services segment and in our business generally; (xi) the success of our marketing efforts and our ability to expand our member base and increase our product adds; (xii) our ability to maintain our leadership position in certain categories of our business and to grow market share in existing markets or any new markets we may enter; (xiii) our ability to develop new products, features and functionality that are competitive and meet market needs; (xiv) our ability to realize the benefits of our strategy, including what we refer to as our FSPL; (xv) our ability to make accurate credit and pricing decisions or effectively forecast our loss rates; (xvi) our ability to establish and maintain an effective system of internal controls over financial reporting; and (xvii) the outcome of any legal or governmental proceedings that may be instituted against us. The foregoing list of factors is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties set forth in the section titled “Risk Factors” in our last quarterly report on Form 10-Q, as filed with the Securities and Exchange Commission, and those that are included in any of our future filings with the Securities and Exchange Commission, including our annual report on Form 10-K, under the Exchange Act.

These forward-looking statements are based on information available as of the date hereof and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date, and we do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements. You should not place undue reliance on these forward-looking statements.

Non-GAAP Financial Measures

This press release presents information about our adjusted net revenue and adjusted EBITDA, which are non-GAAP financial measures provided as supplements to the results provided in accordance with accounting principles generally accepted in the United States (GAAP). We use adjusted net revenue and adjusted EBITDA to evaluate our operating performance, formulate business plans, help better assess our overall liquidity position, and make strategic decisions, including those relating to operating expenses and the allocation of internal resources. Accordingly, we believe that adjusted net revenue and adjusted EBITDA provide useful information to investors and others in understanding and evaluating our operating results in the same manner as our management. These non-GAAP measures are presented for supplemental informational purposes only, have limitations as analytical tools, and should not be considered in isolation from, or as a substitute for, the analysis of other GAAP financial measures, such as total net revenue and net income (loss). Other companies may not use these non-GAAP measures or may use similar measures that are defined in a different manner. Therefore, SoFi's non-GAAP measures may not be directly comparable to similarly titled measures of other companies. Reconciliations of these non-GAAP measures to the most directly comparable GAAP financial measures are provided in Table 2 to the “Financial Tables” herein.

Forward-looking non-GAAP financial measures are presented without reconciliations of such forward-looking non-GAAP measures because the GAAP financial measures are not accessible on a forward-looking basis and reconciling information is not available without unreasonable effort due to the inherent difficulty in forecasting and quantifying certain amounts that are necessary for such reconciliations, including adjustments reflected in our reconciliation of historic non-GAAP financial measures, the amounts of which, based on historical experience, could be material.

About SoFi

SoFi (NASDAQ: SOFI) is a member-centric, one-stop shop for digital financial services on a mission to help people achieve financial independence to realize their ambitions. The company’s full suite of financial products and services helps its over 6.2 million SoFi members borrow, save, spend, invest, and protect their money better by giving them fast access to the tools they need to get their money right, all in one app. SoFi also equips members with the resources they need to get ahead – like career advisors, Credentialed Financial Planners (CFP), exclusive experiences and events, and a thriving community – on their path to financial independence.

SoFi innovates across three business segments: Lending, Financial Services – which includes SoFi Checking and Savings, SoFi Invest, SoFi Credit Card, SoFi Protect, and SoFi Insights – and Technology Platform, which offers the only end-to-end vertically integrated financial technology stack. SoFi Bank, N.A., an affiliate of SoFi, is a nationally chartered bank, regulated by the Federal Reserve, OCC, and FDIC. The company is also the naming rights partner of SoFi Stadium, home of the Los Angeles Chargers and the Los Angeles Rams. For more information, visit https://www.sofi.com or download our iOS and Android apps.

Availability of Other Information About SoFi

Investors and others should note that we communicate with our investors and the public using our website (https://www.sofi.com), the investor relations website (https://investors.sofi.com), and on social media (Twitter and LinkedIn), including but not limited to investor presentations and investor fact sheets, Securities and Exchange Commission filings, press releases, public conference calls and webcasts. The information that SoFi posts on these channels and websites could be deemed to be material information. As a result, SoFi encourages investors, the media, and others interested in SoFi to review the information that is posted on these channels, including the investor relations website, on a regular basis. This list of channels may be updated from time to time on SoFi’s investor relations website and may include additional social media channels. The contents of SoFi’s website or these channels, or any other website that may be accessed from its website or these channels, shall not be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended.

FINANCIAL TABLES

1. Condensed Consolidated Statements of Operations and Comprehensive Loss (Unaudited)

2. Reconciliation of GAAP to Non-GAAP Financial Measures

3. Condensed Consolidated Balance Sheets (Unaudited)

4. Average Balances and Net Interest Earnings Analysis

5. Condensed Consolidated Cash Flow Data (Unaudited)

6. Company Metrics

7. Segment Financials (Unaudited)

Table 1 |

||||||||||||||||

SoFi Technologies, Inc. |

||||||||||||||||

Condensed Consolidated Statements of Operations and Comprehensive Loss |

||||||||||||||||

(Unaudited) |

||||||||||||||||

(In Thousands, Except for Share and Per Share Data) |

||||||||||||||||

|

Three Months Ended June 30, |

|

Six Months Ended June 30, |

|||||||||||||

|

2023 |

|

2022 |

|

2023 |

|

2022 |

|||||||||

Interest income |

|

|

|

|

|

|

|

|||||||||

Loans |

$ |

442,187 |

|

|

$ |

145,337 |

|

|

$ |

799,529 |

|

|

$ |

259,722 |

|

|

Securitizations |

|

2,659 |

|

|

|

2,567 |

|

|

|

5,713 |

|

|

|

5,325 |

|

|

Other |

|

25,150 |

|

|

|

1,608 |

|

|

|

36,318 |

|

|

|

2,877 |

|

|

Total interest income |

|

469,996 |

|

|

|

149,512 |

|

|

|

841,560 |

|

|

|

267,924 |

|

|

Interest expense |

|

|

|

|

|

|

|

|||||||||

Securitizations and warehouses |

|

63,060 |

|

|

|

18,599 |

|

|

|

117,384 |

|

|

|

38,505 |

|

|

Deposits |

|

106,529 |

|

|

|

4,543 |

|

|

|

179,645 |

|

|

|

4,974 |

|

|

Corporate borrowings |

|

9,167 |

|

|

|

3,450 |

|

|

|

17,167 |

|

|

|

6,099 |

|

|

Other |

|

114 |

|

|

|

191 |

|

|

|

228 |

|

|

|

684 |

|

|

Total interest expense |

|

178,870 |

|

|

|

26,783 |

|

|

|

314,424 |

|

|

|

50,262 |

|

|

Net interest income |

|

291,126 |

|

|

|

122,729 |

|

|

|

527,136 |

|

|

|

217,662 |

|

|

Noninterest income |

|

|

|

|

|

|

|

|||||||||

Loan origination and sales |

|

103,064 |

|

|

|

144,414 |

|

|

|

229,575 |

|

|

|

302,118 |

|

|

Securitizations |

|

(12,900 |

) |

|

|

(11,737 |

) |

|

|

(16,077 |

) |

|

|

(23,018 |

) |

|

Servicing |

|

9,052 |

|

|

|

10,471 |

|

|

|

21,794 |

|

|

|

22,707 |

|

|

Technology products and solutions |

|

82,289 |

|

|

|

81,670 |

|

|

|

155,090 |

|

|

|

141,527 |

|

|

Other |

|

25,387 |

|

|

|

14,980 |

|

|

|

52,658 |

|

|

|

31,875 |

|

|

Total noninterest income |

|

206,892 |

|

|

|

239,798 |

|

|

|

443,040 |

|

|

|

475,209 |

|

|

Total net revenue |

|

498,018 |

|

|

|

362,527 |

|

|

|

970,176 |

|

|

|

692,871 |

|

|

Noninterest expense |

|

|

|

|

|

|

|

|||||||||

Technology and product development |

|

126,845 |

|

|

|

99,366 |

|

|

|

243,904 |

|

|

|

181,274 |

|

|

Sales and marketing |

|

182,822 |

|

|

|

143,854 |

|

|

|

357,976 |

|

|

|

281,992 |

|

|

Cost of operations |

|

93,885 |

|

|

|

79,091 |

|

|

|

177,793 |

|

|

|

149,528 |

|

|

General and administrative |

|

131,180 |

|

|

|

125,829 |

|

|

|

254,869 |

|

|

|

262,334 |

|

|

Provision for credit losses |

|

12,615 |

|

|

|

10,103 |

|

|

|

21,022 |

|

|

|

23,064 |

|

|

Total noninterest expense |

|

547,347 |

|

|

|

458,243 |

|

|

|

1,055,564 |

|

|

|

898,192 |

|

|

Loss before income taxes |

|

(49,329 |

) |

|

|

(95,716 |

) |

|

|

(85,388 |

) |

|

|

(205,321 |

) |

|

Income tax benefit (expense) |

|

1,780 |

|

|

|

(119 |

) |

|

|

3,417 |

|

|

|

(871 |

) |

|

Net loss |

$ |

(47,549 |

) |

|

$ |

(95,835 |

) |

|

$ |

(81,971 |

) |

|

$ |

(206,192 |

) |

|

|

|

|

|

|

|

|

|

|||||||||

Loss per share |

|

|

|

|

|

|

|

|||||||||

Loss per share – basic |

$ |

(0.06 |

) |

|

$ |

(0.12 |

) |

|

$ |

(0.11 |

) |

|

$ |

(0.26 |

) |

|

Loss per share – diluted |

$ |

(0.06 |

) |

|

$ |

(0.12 |

) |

|

$ |

(0.11 |

) |

|

$ |

(0.26 |

) |

|

Weighted average common stock outstanding – basic |

|

936,569,420 |

|

|

|

910,046,750 |

|

|

|

932,926,222 |

|

|

|

881,608,165 |

|

|

Weighted average common stock outstanding – diluted |

|

936,569,420 |

|

|

|

910,046,750 |

|

|

|

932,926,222 |

|

|

|

881,608,165 |

|

|

Table 2

Non-GAAP Financial Measures

Reconciliation of Adjusted Net Revenue

Adjusted net revenue is defined as total net revenue, adjusted to exclude the fair value changes in servicing rights and residual interests classified as debt due to valuation inputs and assumptions changes, which relate only to our Lending segment. For our consolidated results and for the Lending segment, we reconcile adjusted net revenue to total net revenue, the most directly comparable GAAP measure, as presented for the periods indicated below:

|

|

Three Months Ended June 30, |

|

Six Months Ended June 30, |

||||||||||||

($ in thousands) |

|

2023 |

|

2022 |

|

2023 |

|

2022 |

||||||||

Total net revenue |

|

$ |

498,018 |

|

|

$ |

362,527 |

|

|

$ |

970,176 |

|

|

$ |

692,871 |

|

Servicing rights – change in valuation inputs or assumptions(1) |

|

|

(8,601 |

) |

|

|

(9,098 |

) |

|

|

(20,685 |

) |

|

|

(20,678 |

) |

Residual interests classified as debt – change in valuation inputs or assumptions(2) |

|

|

(602 |

) |

|

|

2,662 |

|

|

|

(513 |

) |

|

|

5,625 |

|

Adjusted net revenue |

|

$ |

488,815 |

|

|

$ |

356,091 |

|

|

$ |

948,978 |

|

|

$ |

677,818 |

|

|

|

Three Months Ended June 30, |

|

Six Months Ended June 30, |

||||||||||||

($ in thousands) |

|

2023 |

|

2022 |

|

2023 |

|

2022 |

||||||||

Total net revenue – Lending |

|

$ |

331,441 |

|

|

$ |

257,117 |

|

|

$ |

668,522 |

|

|

$ |

510,106 |

|

Servicing rights – change in valuation inputs or assumptions(1) |

|

|

(8,601 |

) |

|

|

(9,098 |

) |

|

|

(20,685 |

) |

|

|

(20,678 |

) |

Residual interests classified as debt – change in valuation inputs or assumptions(2) |

|

|

(602 |

) |

|

|

2,662 |

|

|

|

(513 |

) |

|

|

5,625 |

|

Adjusted net revenue – Lending |

|

$ |

322,238 |

|

|

$ |

250,681 |

|

|

$ |

647,324 |

|

|

$ |

495,053 |

|

___________________

(1) |

|

Reflects changes in fair value inputs and assumptions on servicing rights, including conditional prepayment, default rates and discount rates. These assumptions are highly sensitive to market interest rate changes and are not indicative of our performance or results of operations. Moreover, these non-cash charges are unrealized during the period and, therefore, have no impact on our cash flows from operations. As such, these positive and negative changes are adjusted out of total net revenue to provide management and financial users with better visibility into the net revenue available to finance our operations and our overall performance. |

(2) |

|

Reflects changes in fair value inputs and assumptions on residual interests classified as debt, including conditional prepayment, default rates and discount rates. When third parties finance our consolidated securitization VIEs by purchasing residual interests, we receive proceeds at the time of the closing of the securitization and, thereafter, pass along contractual cash flows to the residual interest owner. These residual debt obligations are measured at fair value on a recurring basis, but they have no impact on our initial financing proceeds, our future obligations to the residual interest owner (because future residual interest claims are limited to contractual securitization collateral cash flows), or the general operations of our business. As such, these positive and negative non-cash changes in fair value attributable to assumption changes are adjusted out of total net evenue to provide management and financial users with better visibility into the net revenue available to finance our operations. |

Reconciliation of Adjusted EBITDA

Adjusted EBITDA is defined as net income (loss), adjusted to exclude, as applicable: (i) corporate borrowing-based interest expense (our adjusted EBITDA measure is not adjusted for warehouse or securitization-based interest expense, nor deposit interest expense and finance lease liability interest expense, as these are not direct operating expenses), (ii) income tax expense (benefit), (iii) depreciation and amortization, (iv) share-based expense (inclusive of equity-based payments to non-employees), (v) impairment expense (inclusive of goodwill impairment and property, equipment and software abandonments), (vi) transaction-related expenses, (vii) fair value changes in warrant liabilities, (viii) fair value changes in each of servicing rights and residual interests classified as debt due to valuation assumptions, and (ix) other charges, as appropriate, that are not expected to recur and are not indicative of our core operating performance. We reconcile adjusted EBITDA to net loss, the most directly comparable GAAP measure, for the periods indicated below:

|

|

Three Months Ended June 30, |

|

Six Months Ended June 30, |

||||||||||||

($ in thousands) |

|

2023 |

|

2022 |

|

2023 |

|

2022 |

||||||||

Net loss |

|

$ |

(47,549 |

) |

|

$ |

(95,835 |

) |

|

$ |

(81,971 |

) |

|

$ |

(206,192 |

) |

Non-GAAP adjustments: |

|

|

|

|

|

|

|

|

||||||||

Interest expense – corporate borrowings(1) |

|

|

9,167 |

|

|

|

3,450 |

|

|

|

17,167 |

|

|

|

6,099 |

|

Income tax (benefit) expense(2) |

|

|

(1,780 |

) |

|

|

119 |

|

|

|

(3,417 |

) |

|

|

871 |

|

Depreciation and amortization(3) |

|

|

50,130 |

|

|

|

38,056 |

|

|

|

95,451 |

|

|

|

68,754 |

|

Share-based expense |

|

|

75,878 |

|

|

|

80,142 |

|

|

|

140,104 |

|

|

|

157,163 |

|

Restructuring charges(4) |

|

|

— |

|

|

|

— |

|

|

|

4,953 |

|

|

|

— |

|

Impairment expense(5) |

|

|

— |

|

|

|

— |

|

|

|

1,243 |

|

|

|

— |

|

Transaction-related expense(6) |

|

|

176 |

|

|

|

808 |

|

|

|

176 |

|

|

|

17,346 |

|

Servicing rights – change in valuation inputs or assumptions(7) |

|

|

(8,601 |

) |

|

|

(9,098 |

) |

|

|

(20,685 |

) |

|

|

(20,678 |

) |

Residual interests classified as debt – change in valuation inputs or assumptions(8) |

|

|

(602 |

) |

|

|

2,662 |

|

|

|

(513 |

) |

|

|

5,625 |

|

Total adjustments |

|

|

124,368 |

|

|

|

116,139 |

|

|

|

234,479 |

|

|

|

235,180 |

|

Adjusted EBITDA |

|

$ |

76,819 |

|

|

$ |

20,304 |

|

|

$ |

152,508 |

|

|

$ |

28,988 |

|

___________________

(1) |

|

Our adjusted EBITDA measure adjusts for corporate borrowing-based interest expense, as these expenses are a function of our capital structure. Corporate borrowing-based interest expense includes interest on our revolving credit facility and the amortization of debt discount and debt issuance costs on our convertible notes. Revolving credit facility interest expense in the 2023 periods increased due to higher interest rates relative to the prior year periods on identical outstanding debt. |

(2) |

|

Income taxes were primarily attributable to tax expense associated with the profitability of SoFi Bank in state jurisdictions where separate filings are required. For the three and six month 2023 periods, this expense was more than offset by income tax benefits from foreign losses in jurisdictions with net deferred tax liabilities related to Technisys. |

(3) |

Depreciation and amortization expense for the 2023 periods increased compared to the 2022 periods primarily in connection with acquisitions and growth in our internally-developed software balance. | |

(4) |

Restructuring charges in the six-month 2023 period primarily included employee-related wages, benefits and severance associated with a small reduction in headcount in our Technology Platform segment in the first quarter of 2023, which do not reflect expected future operating expenses and are not indicative of our core operating performance. |

|

(5) |

Impairment expense in the six-month 2023 period relates to a sublease arrangement, which is not indicative of our core operating performance. |

|

(6) |

Transaction-related expenses in the 2023 and 2022 periods included financial advisory and professional services costs associated with our acquisition of Wyndham and Technisys, respectively. |

|

(7) |

Reflects changes in fair value inputs and assumptions, including market servicing costs, conditional prepayment, default rates and discount rates. This non-cash change is unrealized during the period and, therefore, has no impact on our cash flows from operations. As such, these positive and negative changes in fair value attributable to assumption changes are adjusted out of net loss to provide management and financial users with better visibility into the earnings available to finance our operations. | |

(8) |

Reflects changes in fair value inputs and assumptions, including conditional prepayment, default rates and discount rates. When third parties finance our consolidated VIEs through purchasing residual interests, we receive proceeds at the time of the securitization close and, thereafter, pass along contractual cash flows to the residual interest owner. These obligations are measured at fair value on a recurring basis, which has no impact on our initial financing proceeds, our future obligations to the residual interest owner (because future residual interest claims are limited to contractual securitization collateral cash flows), or the general operations of our business. As such, these positive and negative non-cash changes in fair value attributable to assumption changes are adjusted out of net loss to provide management and financial users with better visibility into the earnings available to finance our operations. |

Table 3 |

||||||||

SoFi Technologies, Inc. |

||||||||

Condensed Consolidated Balance Sheets |

||||||||

(Unaudited) |

||||||||

(In Thousands, Except for Share Data) |

||||||||

|

June 30,

|

|

December 31,

|

|||||

Assets |

|

|

|

|||||

Cash and cash equivalents |

$ |

3,015,652 |

|

|

$ |

1,421,907 |

|

|

Restricted cash and restricted cash equivalents |

|

485,476 |

|

|

|

424,395 |

|

|

Investment securities (includes available-for-sale securities of $382,782 and $195,438 at fair value with associated amortized cost of $387,815 and $203,418, as of June 30, 2023 and December 31, 2022, respectively) |

|

548,232 |

|

|

|

396,769 |

|

|

Loans held for sale, at fair value |

|

18,213,667 |

|

|

|

13,557,074 |

|

|

Loans held for investment (less allowance for credit losses on loans at amortized cost of $41,227 and $40,788, as of June 30, 2023 and December 31, 2022, respectively) |

|

347,551 |

|

|

|

307,957 |

|

|

Servicing rights |

|

145,663 |

|

|

|

149,854 |

|

|

Property, equipment and software |

|

191,352 |

|

|

|

170,104 |

|

|

Goodwill |

|

1,640,679 |

|

|

|

1,622,991 |

|

|

Intangible assets |

|

412,099 |

|

|

|

442,155 |

|

|

Operating lease right-of-use assets |

|

94,523 |

|

|

|

97,135 |

|

|

Other assets (less allowance for credit losses of $1,937 and $2,785, as of June 30, 2023 and December 31, 2022, respectively) |

|

466,555 |

|

|

|

417,334 |

|

|

Total assets |

$ |

25,561,449 |

|

|

$ |

19,007,675 |

|

|

Liabilities, temporary equity and permanent equity |

|

|

|

|||||

Liabilities: |

|

|

|

|||||

Deposits: |

|

|

|

|||||

Interest-bearing deposits |

$ |

12,672,392 |

|

|

$ |

7,265,792 |

|

|

Noninterest-bearing deposits |

|

67,681 |

|

|

|

76,504 |

|

|

Total deposits |

|

12,740,073 |

|

|

|

7,342,296 |

|

|

Accounts payable, accruals and other liabilities |

|

632,459 |

|

|

|

516,215 |

|

|

Operating lease liabilities |

|

115,224 |

|

|

|

117,758 |

|

|

Debt |

|

6,484,326 |

|

|

|

5,485,882 |

|

|

Residual interests classified as debt |

|

11,332 |

|

|

|

17,048 |

|

|

Total liabilities |

|

19,983,414 |

|

|

|

13,479,199 |

|

|

Commitments, guarantees, concentrations and contingencies |

|

|

|

|||||

Temporary equity: |

|

|

|

|||||

Redeemable preferred stock, $0.00 par value: 100,000,000 and 100,000,000 shares authorized; 3,234,000 and 3,234,000 shares issued and outstanding as of June 30, 2023 and December 31, 2022, respectively |

|

320,374 |

|

|

|

320,374 |

|

|

Permanent equity: |

|

|

|

|||||

Common stock, $0.00 par value: 3,100,000,000 and 3,100,000,000 shares authorized; 948,912,761 and 933,896,120 shares issued and outstanding as of June 30, 2023 and December 31, 2022, respectively |

|

94 |

|

|

|

93 |

|

|

Additional paid-in capital |

|

6,848,178 |

|

|

|

6,719,826 |

|

|

Accumulated other comprehensive loss |

|

(5,119 |

) |

|

|

(8,296 |

) |

|

Accumulated deficit |

|

(1,585,492 |

) |

|

|

(1,503,521 |

) |

|

Total permanent equity |

|

5,257,661 |

|

|

|

5,208,102 |

|

|

Total liabilities, temporary equity and permanent equity |

$ |

25,561,449 |

|

|

$ |

19,007,675 |

||

Table 4 |

||||||||||||||||||

SoFi Technologies, Inc. |

||||||||||||||||||

Average Balances and Net Interest Earnings Analysis |

||||||||||||||||||

|

Three Months Ended June 30, 2023 |

|

Three Months Ended June 30, 2022 |

|||||||||||||||

($ in thousands) |

|

Average

|

|

Interest Income/Expense |

|

Average

|

|

Average

|

|

Interest

|

|

Average

|

||||||

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Interest-earning assets: |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Interest-bearing deposits with banks |

|

$ |

2,158,973 |

|

$ |

24,127 |

|

4.48 |

% |

|

$ |

1,064,672 |

|

$ |

943 |

|

0.35 |

% |

Investment securities |

|

|

387,453 |

|

|

3,682 |

|

3.81 |

|

|

|

505,840 |

|

|

3,004 |

|

2.38 |

|

Loans |

|

|

17,810,656 |

|

|

442,187 |

|

9.96 |

|

|

|

7,804,416 |

|

|

145,337 |

|

7.45 |

|

Total interest-earning assets |

|

|

20,357,082 |

|

|

469,996 |

|

9.26 |

% |

|

|

9,374,928 |

|

|

149,284 |

|

6.37 |

% |

Total noninterest-earning assets |

|

|

2,862,005 |

|

|

|

|

|

|

3,011,591 |

|

|

|

|

||||

Total assets |

|

$ |

23,219,087 |

|

|

|

|

|

$ |

12,386,519 |

|

|

|

|

||||

Liabilities, Temporary Equity and Permanent Equity |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Interest-bearing liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Demand deposits |

|

$ |

2,071,639 |

|

$ |

12,922 |

|

2.50 |

% |

|

$ |

1,137,097 |

|

$ |

2,654 |

|

0.93 |

% |

Savings deposits |

|

|

7,292,617 |

|

|

73,114 |

|

4.02 |

|

|

|

673,561 |

|

|

1,863 |

|

1.11 |

|

Time deposits |

|

|

1,708,576 |

|

|

20,493 |

|

4.81 |

|

|

|

17,660 |

|

|

26 |

|

0.59 |

|

Total interest-bearing deposits |

|

|

11,072,832 |

|

|

106,529 |

|

3.86 |

|

|

|

1,828,318 |

|

|

4,543 |

|

0.99 |

|

Warehouse facilities |

|

|

3,204,559 |

|

|

48,080 |

|

6.02 |

|

|

|

2,093,373 |

|

|

9,717 |

|

1.86 |

|

Securitization debt |

|

|

908,381 |

|

|

10,770 |

|

4.76 |

|

|

|

547,049 |

|

|

5,204 |

|

3.81 |

|

Other debt |

|

|

1,642,953 |

|

|

13,491 |

|

3.29 |

|

|

|

1,643,944 |

|

|

6,091 |

|

1.48 |

|

Total debt |

|

|

5,755,893 |

|

|

72,341 |

|

5.04 |

|

|

|

4,284,366 |

|

|

21,012 |

|

1.96 |

|

Residual interests classified as debt |

|

|

13,015 |

|

|

— |

|

— |

|

|

|

61,388 |

|

|

1,037 |

|

6.76 |

|

Total interest-bearing liabilities |

|

|

16,841,740 |

|

|

178,870 |

|

4.26 |

% |

|

|

6,174,072 |

|

|

26,592 |

|

1.72 |

% |

Total noninterest-bearing liabilities |

|

|

786,175 |

|

|

|

|

|

|

682,474 |

|

|

|

|

||||

Total liabilities |

|

|

17,627,915 |

|

|

|

|

|

|

6,856,546 |

|

|

|

|

||||

Total temporary equity |

|

|

320,374 |

|

|

|

|

|

|

320,374 |

|

|

|

|

||||

Total permanent equity |

|

|

5,270,798 |

|

|

|

|

|

|

5,209,599 |

|

|

|

|

||||

Total liabilities, temporary equity and permanent equity |

|

$ |

23,219,087 |

|

|

|

|

|

$ |

12,386,519 |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Net interest income |

|

|

|

$ |

291,126 |

|

|

|

|

|

$ |

122,692 |

|

|

||||

Net interest margin |

|

|

|

|

|

5.74 |

% |

|

|

|

|

|

5.23 |

% |

||||

Table 5 |

||||||||

SoFi Technologies, Inc. |

||||||||

Condensed Consolidated Cash Flow Data |

||||||||

(Unaudited) |

||||||||

(In Thousands) |

||||||||

|

Six Months Ended June 30, |

|||||||

|

2023 |

|

2022 |

|||||

Net cash used in operating activities |

$ |

(4,292,679 |

) |

|

$ |

(1,956,723 |

) |

|

Net cash used in investing activities |

|

(307,826 |

) |

|

|

(4,918 |

) |

|

Net cash provided by financing activities |

|

6,255,232 |

|

|

|

2,192,231 |

|

|

Effect of exchange rates on cash and cash equivalents |

|

99 |

|

|

|

(94 |

) |

|

Net increase in cash, cash equivalents, restricted cash and restricted cash equivalents |

$ |

1,654,826 |

|

|

$ |

230,496 |

|

|

Cash, cash equivalents, restricted cash and restricted cash equivalents at beginning of period |

|

1,846,302 |

|

|

|

768,437 |

|

|

Cash, cash equivalents, restricted cash and restricted cash equivalents at end of period |

$ |

3,501,128 |

|

|

$ |

998,933 |

||

Table 6 |

||||||||||||||||||

| Company Metrics | ||||||||||||||||||

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

June 30,

|

|

Members |

6,240,091 |

|

5,655,711 |

|

5,222,533 |

|

4,742,673 |

|

4,318,705 |

|

3,868,334 |

|

3,460,298 |

|

2,937,379 |

|

2,560,492 |

|

Total Products |

9,401,025 |

|

8,554,363 |

|

7,894,636 |

|

7,199,298 |

|

6,564,174 |

|

5,862,137 |

|

5,173,197 |

|

4,267,665 |

|

3,667,121 |

|

Total Products — Lending segment |

1,503,892 |

|

1,416,122 |

|

1,340,597 |

|

1,280,493 |

|

1,202,027 |

|

1,138,566 |

|

1,078,952 |

|

1,030,882 |

|

981,440 |

|

Total Products — Financial Services segment |

7,897,133 |

|

7,138,241 |

|

6,554,039 |

|

5,918,805 |

|

5,362,147 |

|

4,723,571 |

|

4,094,245 |

|

3,236,783 |

|

2,685,681 |

|

Total Accounts — Technology Platform segment(1) |

129,356,203 |

|

126,326,916 |

|

130,704,351 |

|

124,332,810 |

|

116,570,038 |

|

109,687,014 |

|

99,660,657 |

|

88,811,022 |

|

78,902,156 |

|

___________________

(1) |

|

Beginning in the fourth quarter of 2021, the Company included SoFi accounts on the Galileo platform-as-a-service in its total Technology Platform accounts metric to better align with the presentation of Technology Platform segment revenue. Quarterly amounts for the earlier quarters in 2021 were determined to be immaterial, and as such were not recast. |

Members

We refer to our customers as “members”. We define a member as someone who has a lending relationship with us through origination and/or ongoing servicing, opened a financial services account, linked an external account to our platform, or signed up for our credit score monitoring service. Our members have continuous access to our certified financial planners, our career advice services, our member events, our content, educational material, news, and our tools and calculators, which are provided at no cost to the member. We view members as an indication not only of the size and a measurement of growth of our business, but also as a measure of the significant value of the data we have collected over time.

Once someone becomes a member, they are always considered a member unless they violate our terms of service. We adjust our total number of members in the event a member is removed in accordance with our terms of service. This could occur for a variety of reasons—including fraud or pursuant to certain legal processes—and, as our terms of service evolve together with our business practices, product offerings and applicable regulations, our grounds for removing members from our total member count could change. The determination that a member should be removed in accordance with our terms of service is subject to an evaluation process, following the completion, and based on the results, of which, relevant members and their associated products are removed from our total member count in the period in which such evaluation process concludes. However, depending on the length of the evaluation process, that removal may not take place in the same period in which the member was added to our member count or the same period in which the circumstances leading to their removal occurred. For this reason, our total member count may not yet reflect adjustments that may be made once ongoing evaluation processes, if any, conclude.

Total Products

Total products refers to the aggregate number of lending and financial services products that our members have selected on our platform since our inception through the reporting date, whether or not the members are still registered for such products. Total products is a primary indicator of the size and reach of our Lending and Financial Services segments. Management relies on total products metrics to understand the effectiveness of our member acquisition efforts and to gauge the propensity for members to use more than one product.

In our Lending segment, total products refers to the number of personal loans, student loans and home loans that have been originated through our platform through the reporting date, whether or not such loans have been paid off. If a member has multiple loan products of the same loan product type, such as two personal loans, that is counted as a single product. However, if a member has multiple loan products across loan product types, such as one personal loan and one home loan, that is counted as two products.

In our Financial Services segment, total products refers to the number of SoFi Money accounts (inclusive of checking and savings accounts held at SoFi Bank and cash management accounts), SoFi Invest accounts, SoFi Credit Card accounts (including accounts with a zero dollar balance at the reporting date), referred loans (which are originated by a third-party partner to which we provide pre-qualified borrower referrals), SoFi At Work accounts and SoFi Relay accounts (with either credit score monitoring enabled or external linked accounts) that have been opened through our platform through the reporting date. Checking and savings accounts are considered one account within our total products metric. Our SoFi Invest service is composed of three products: active investing accounts, robo-advisory accounts and digital assets accounts. Our members can select any one or combination of the three types of SoFi Invest products. If a member has multiple SoFi Invest products of the same account type, such as two active investing accounts, that is counted as a single product. However, if a member has multiple SoFi Invest products across account types, such as one active investing account and one robo-advisory account, those separate account types are considered separate products. In the event a member is removed in accordance with our terms of service, as discussed under “Members” above, the member’s associated products are also removed.

Technology Platform Total Accounts

In our Technology Platform segment, total accounts refers to the number of open accounts at Galileo as of the reporting date. Beginning in the fourth quarter of 2021, we included intercompany accounts on the Galileo platform-as-a-service in our total accounts metric to better align with the Technology Platform segment revenue, which includes intercompany revenue. We recast the accounts in the fourth quarter of 2021, but did not recast the accounts for the earlier quarters in 2021, as the impact was determined to be immaterial. Total accounts is a primary indicator of the accounts dependent upon our technology platform to use virtual card products, virtual wallets, make peer-to-peer and bank-to-bank transfers, receive early paychecks, separate savings from spending balances, make debit transactions and rely upon real-time authorizations, all of which result in revenues for the Technology Platform segment. We do not measure total accounts for the Technisys products and solutions, as the revenue model is not primarily dependent upon being a fully integrated, stand-ready service.

Table 7 |

||||||||||||||||||||||||||||||||||||

Segment Financials |

||||||||||||||||||||||||||||||||||||

(Unaudited) |

||||||||||||||||||||||||||||||||||||

|

|

Quarter Ended |

||||||||||||||||||||||||||||||||||

($ in thousands) |

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

June 30,

|

|

March 31,

|

|

December 31,

|

|

September 30,

|

|

June 30,

|

||||||||||||||||||

Lending |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

Net interest income |

|

$ |

231,885 |

|

|

$ |

201,047 |

|

|

$ |

183,607 |

|

|

$ |

139,516 |

|

|

$ |

114,003 |

|

|

$ |

94,354 |

|

|

$ |

77,246 |

|

|

$ |

72,257 |

|

|

$ |

56,822 |

|

Total noninterest income. |

|

|

99,556 |

|

|

|

136,034 |

|

|

|

144,584 |

|

|

|

162,178 |

|

|

|

143,114 |

|

|

|

158,635 |

|

|

|

136,518 |

|

|

|

138,034 |

|

|

|

109,469 |

|

Total net revenue |

|

|

331,441 |

|

|

|

337,081 |

|

|

|

328,191 |

|

|

|

301,694 |

|

|

|

257,117 |

|

|

|

252,989 |

|

|

|

213,764 |

|

|

|

210,291 |

|

|

|

166,291 |

|

Adjusted net revenue(1) |

|

|

322,238 |

|

|

|

325,086 |

|

|

|

314,930 |

|

|

|

296,965 |

|

|

|

250,681 |

|

|

|

244,372 |

|

|

|

208,032 |

|

|

|

215,475 |

|

|

|

172,232 |

|

Contribution profit |

|

|

183,309 |

|

|

|

209,898 |

|

|

|

208,799 |

|

|

|

180,562 |

|

|

|

141,991 |

|

|

|

132,651 |

|

|

|

105,065 |

|

|

|

117,668 |

|

|

|

89,188 |

|

Technology Platform |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

Net interest income (expense) |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

39 |

|

|

$ |

(32 |

) |

Total noninterest income |

|

|

87,623 |

|

|

|

77,887 |

|

|

|