NetApp (NASDAQ:NTAP) Exceeds Q3 CY2025 Expectations

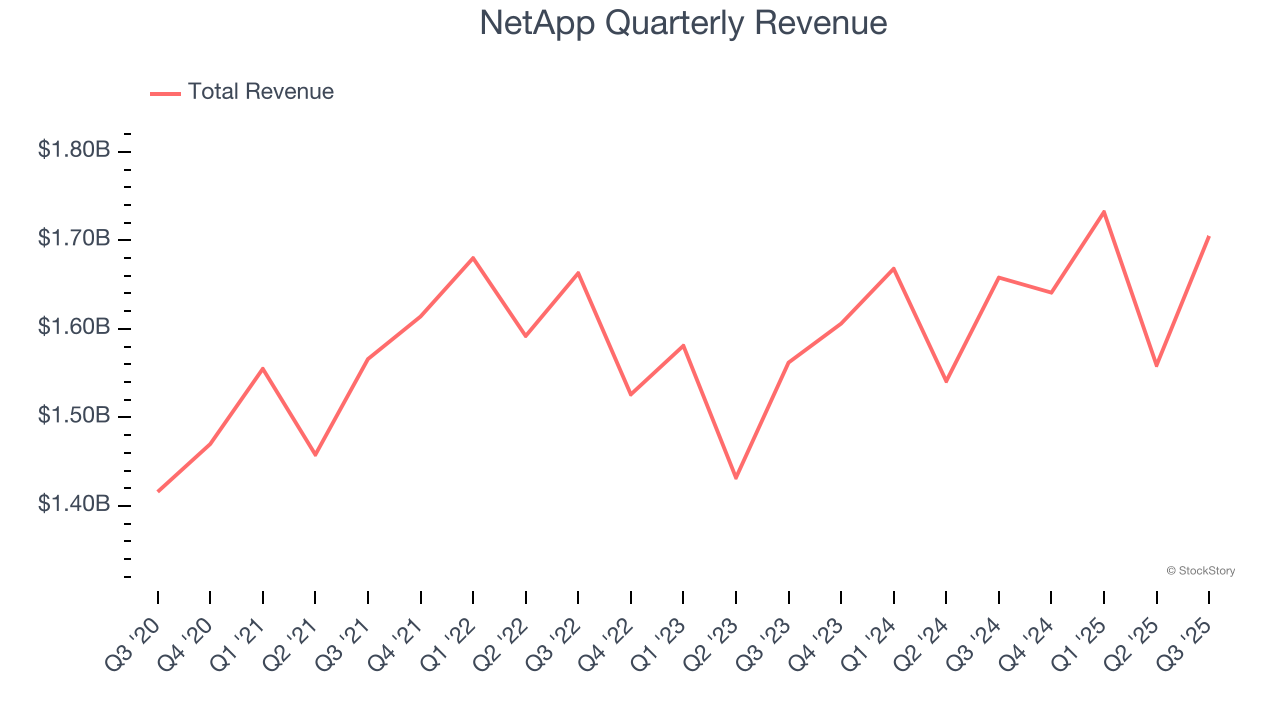

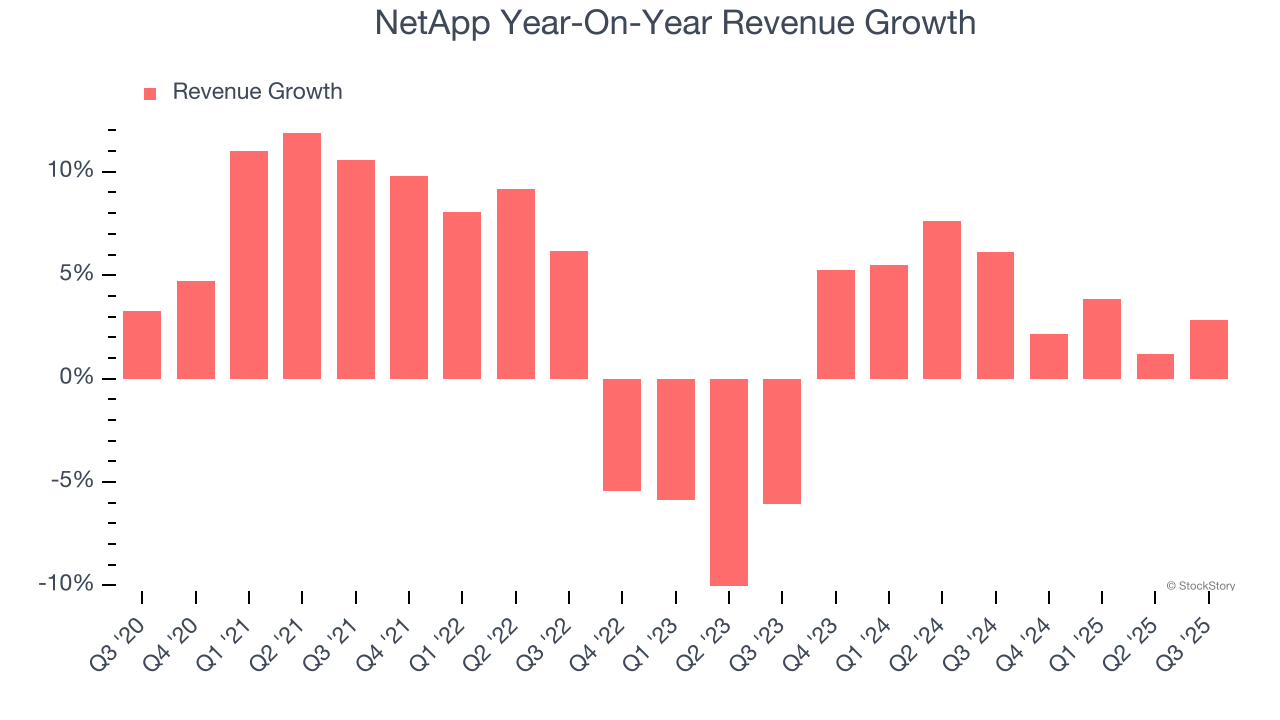

Data storage company NetApp (NASDAQ: NTAP) announced better-than-expected revenue in Q3 CY2025, with sales up 2.8% year on year to $1.71 billion. On the other hand, next quarter’s revenue guidance of $1.69 billion was less impressive, coming in 1.1% below analysts’ estimates. Its non-GAAP profit of $2.05 per share was 8.8% above analysts’ consensus estimates.

Is now the time to buy NetApp? Find out by accessing our full research report, it’s free for active Edge members.

NetApp (NTAP) Q3 CY2025 Highlights:

- Revenue: $1.71 billion vs analyst estimates of $1.69 billion (2.8% year-on-year growth, 1.1% beat)

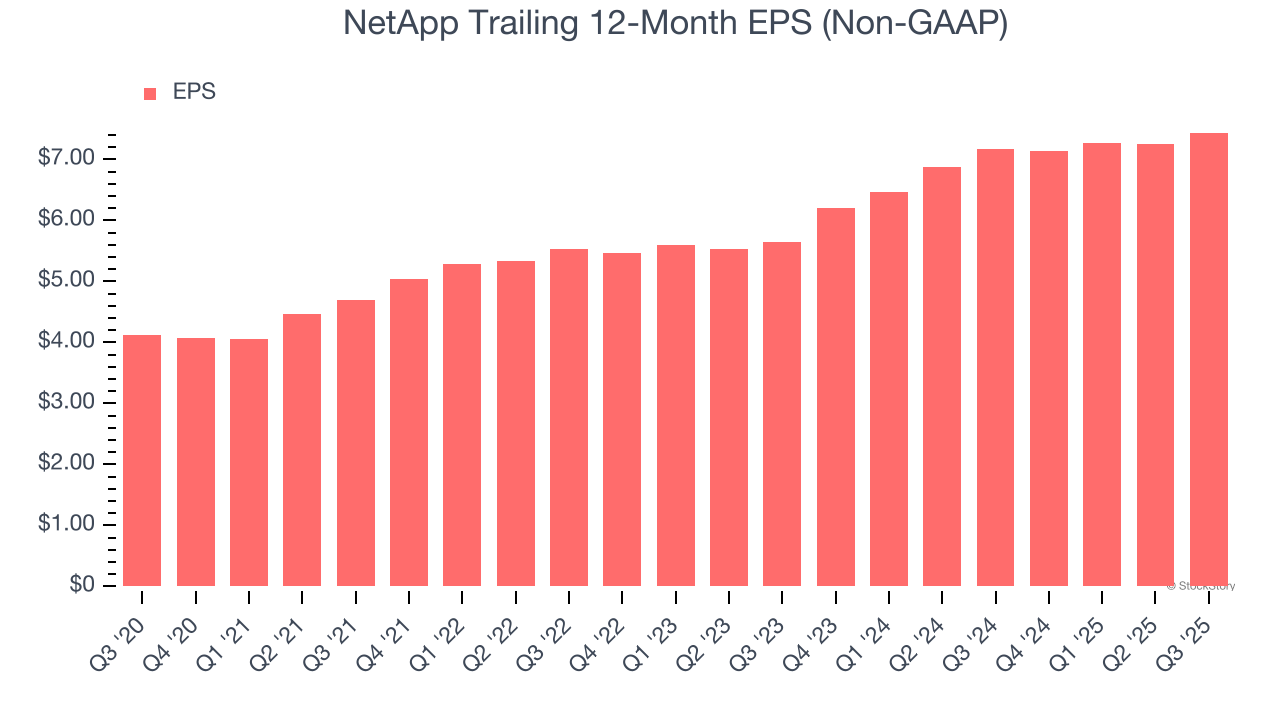

- Adjusted EPS: $2.05 vs analyst estimates of $1.88 (8.8% beat)

- Adjusted EBITDA: $553 million vs analyst estimates of $531.1 million (32.4% margin, 4.1% beat)

- The company reconfirmed its revenue guidance for the full year of $6.75 billion at the midpoint

- Management raised its full-year Adjusted EPS guidance to $7.90 at the midpoint, a 1.9% increase

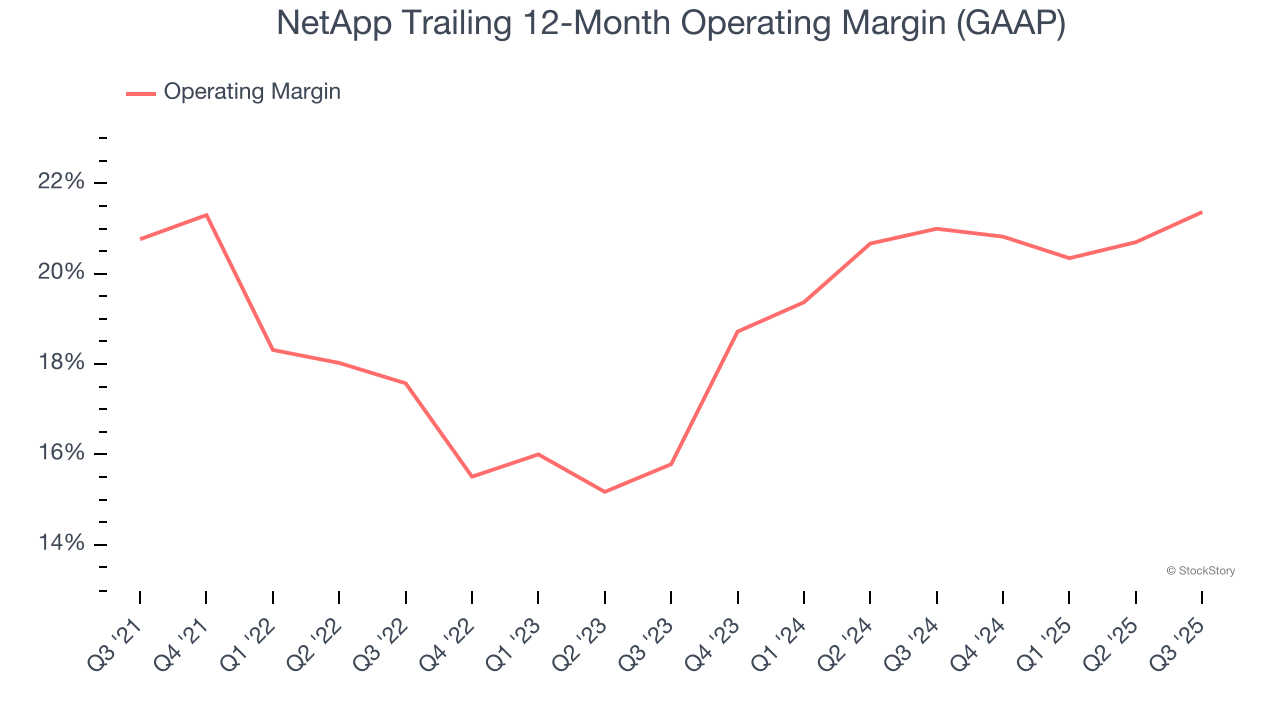

- Operating Margin: 23.4%, up from 20.8% in the same quarter last year

- Free Cash Flow Margin: 4.6%, similar to the same quarter last year

- Market Capitalization: $21.75 billion

Company Overview

Founded in 1992 as a pioneer in networked storage technology, NetApp (NASDAQ: NTAP) provides data storage and management solutions that help organizations store, protect, and optimize their data across on-premises data centers and public clouds.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $6.64 billion in revenue over the past 12 months, NetApp is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To expand meaningfully, NetApp likely needs to tweak its prices, innovate with new offerings, or enter new markets.

As you can see below, NetApp’s sales grew at a tepid 3.7% compounded annual growth rate over the last five years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. NetApp’s annualized revenue growth of 4.3% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, NetApp reported modest year-on-year revenue growth of 2.8% but beat Wall Street’s estimates by 1.1%. Company management is currently guiding for a 3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.4% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its newer products and services will not accelerate its top-line performance yet.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

NetApp’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 19.3% over the last five years. This profitability was elite for a business services business thanks to its efficient cost structure and economies of scale.

Analyzing the trend in its profitability, NetApp’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q3, NetApp generated an operating margin profit margin of 23.4%, up 2.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

NetApp’s EPS grew at a remarkable 12.5% compounded annual growth rate over the last five years, higher than its 3.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For NetApp, its two-year annual EPS growth of 14.9% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q3, NetApp reported adjusted EPS of $2.05, up from $1.87 in the same quarter last year. This print beat analysts’ estimates by 8.8%. Over the next 12 months, Wall Street expects NetApp’s full-year EPS of $7.44 to grow 11%.

Key Takeaways from NetApp’s Q3 Results

It was good to see NetApp beat analysts’ EPS expectations this quarter. We were also happy its full-year EPS guidance outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter slightly missed. Overall, this print had some key positives. The stock traded up 2.1% to $113.80 immediately following the results.

Is NetApp an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

More News

View More

Recent Quotes

View More

Quotes delayed at least 20 minutes.

By accessing this page, you agree to the Privacy Policy and Terms Of Service.