Based in Bethesda, Maryland, Lockheed Martin Corporation (LMT) develops advanced combat aircraft, missile systems, helicopters, radar platforms, cyber solutions, and satellites that anchor air, land, sea, and space operations.

With a market capitalization of nearly $152.9 billion, it occupies the “large-cap” territory, a league reserved for companies valued above $10 billion. This scale enables Lockheed Martin to integrate complex technologies across domains and deliver cohesive defense ecosystems.

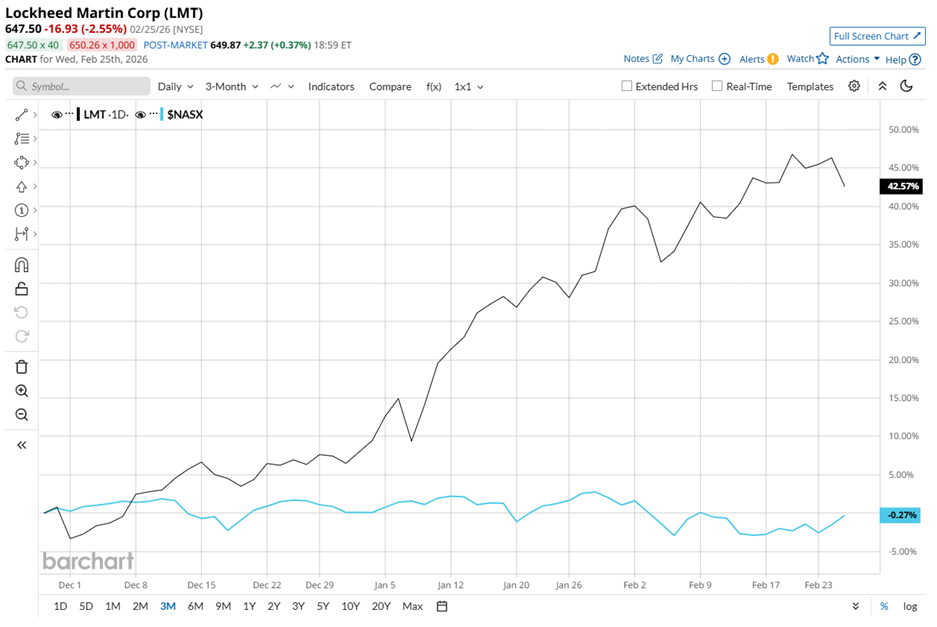

Momentum has followed fundamentals. The shares trade just 3.3% below their February high of $669.75 and have surged 43.1% over the past three months. Over the same period, the Nasdaq Composite ($NASX) has posted only marginal gains, underscoring Lockheed Martin’s relative outperformance in the near term.

Over the past 52 weeks, the stock has skyrocketed 44.4%, decisively outpacing the Nasdaq’s 21.7% gain, which signals sustained relative strength. Year-to-date (YTD), LMT stock remains up 33.9% even as the broader benchmark has slipped into negative territory, reinforcing its defensive leadership profile.

The technical structure confirms the move. Since January, the shares have held firmly above the 50-day moving average of $568.97 and the 200-day moving average of $491.68.

The inflection became clearer on Jan. 29 when shares rose 4.2% after the company released Q4 fiscal year 2025 results. Revenue increased 9.1% year over year to $20.3 billion, surpassing analyst expectations of $19.8 billion. EPS grew 161.3% from the year-ago value to $5.80 and came in ahead of the Street’s $5.75 forecast.

The company ended the year with a record $194 billion backlog, reinforcing long-term revenue visibility. Moreover, rising global demand prompted management to invest more than $3.5 billion during 2025 to expand production capacity and advance next-generation technologies.

For fiscal year 2026, management forecasts approximately 5% sales growth and a stronger 25% increase in reported segment operating profit year over year. The company expects free cash flow between $6.5 billion and $6.8 billion, above prior guidance, strengthening balance sheet flexibility and capital return potential.

Relative performance adds further context. Lockheed Martin’s rival, The Boeing Company (BA), has delivered a 29.2% gain over the past 52 weeks and stands up 6.1% YTD. Boeing’s rebound has been notable, yet Lockheed Martin’s advance is more decisive.

Owing to the company’s strong operational backdrop, record backlog, and expanding margins, Wall Street assigns the stock an overall rating of “Moderate Buy,” reflecting confidence in sustained execution. Moreover, the stock is already trading above its average price target of $627.14.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart