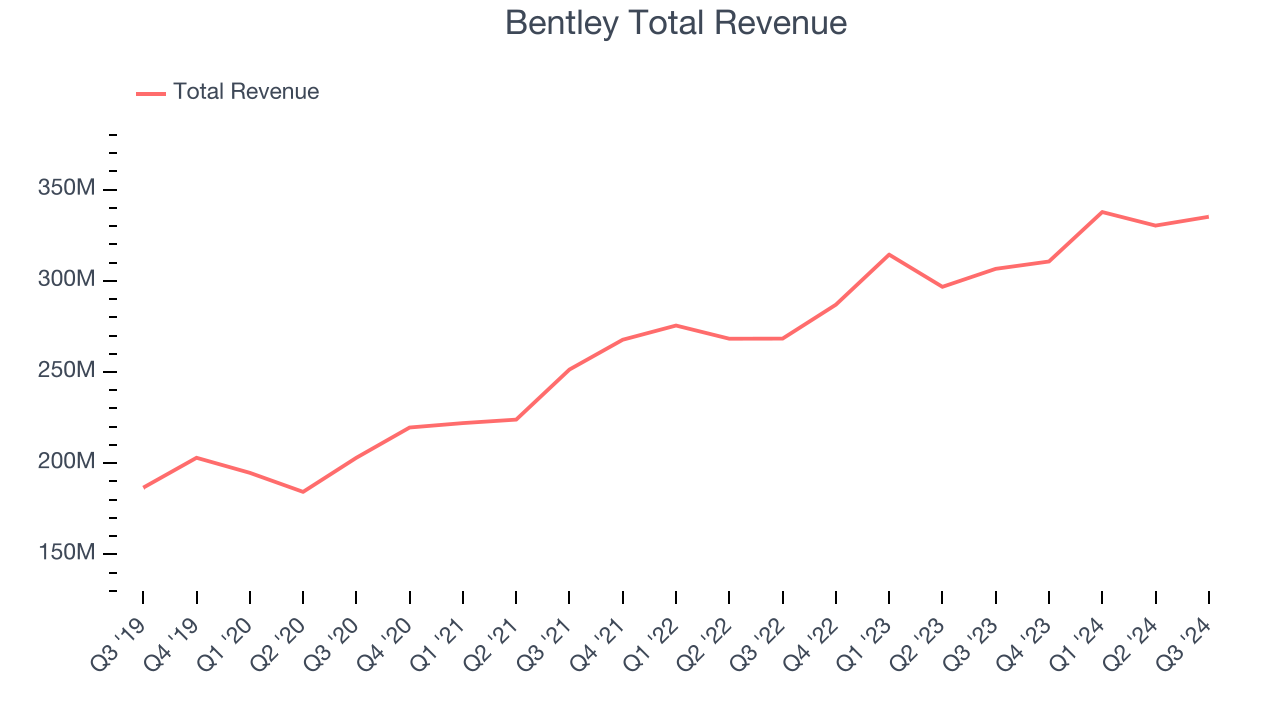

Infrastructure design software provider Bentley Systems (NASDAQ:BSY) missed Wall Street’s revenue expectations in Q3 CY2024, but sales rose 9.3% year on year to $335.2 million. Its non-GAAP profit of $0.24 per share was also 1.9% below analysts’ consensus estimates.

Is now the time to buy Bentley? Find out by accessing our full research report, it’s free.

Bentley (BSY) Q3 CY2024 Highlights:

- Revenue: $335.2 million vs analyst estimates of $341.1 million (1.7% miss)

- Adjusted EPS: $0.24 vs analyst expectations of $0.24 (1.9% miss)

- EBITDA: $110 million vs analyst estimates of $110.2 million (small miss)

- Gross Margin (GAAP): 80.7%, up from 78.9% in the same quarter last year

- Operating Margin: 20.5%, down from 24% in the same quarter last year

- EBITDA Margin: 32.8%, down from 35.6% in the same quarter last year

- Free Cash Flow Margin: 25.1%, up from 18% in the previous quarter

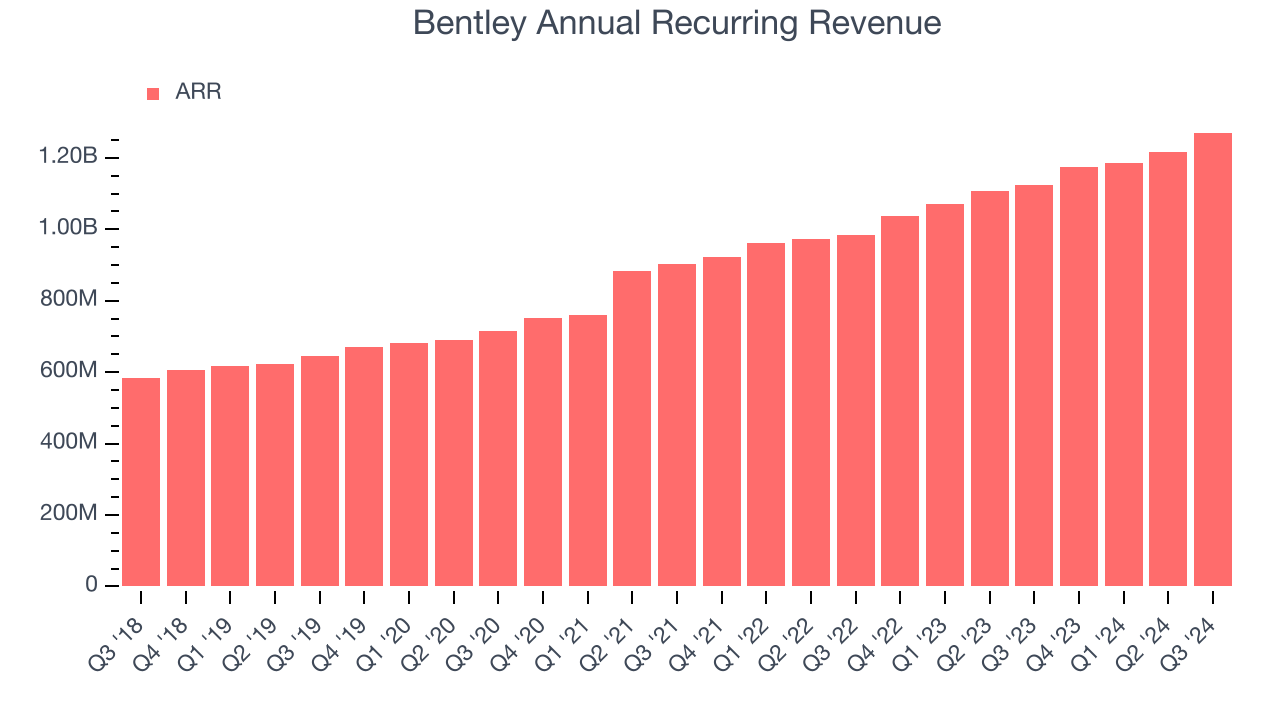

- Annual Recurring Revenue: $1.27 billion at quarter end, up 13% year on year

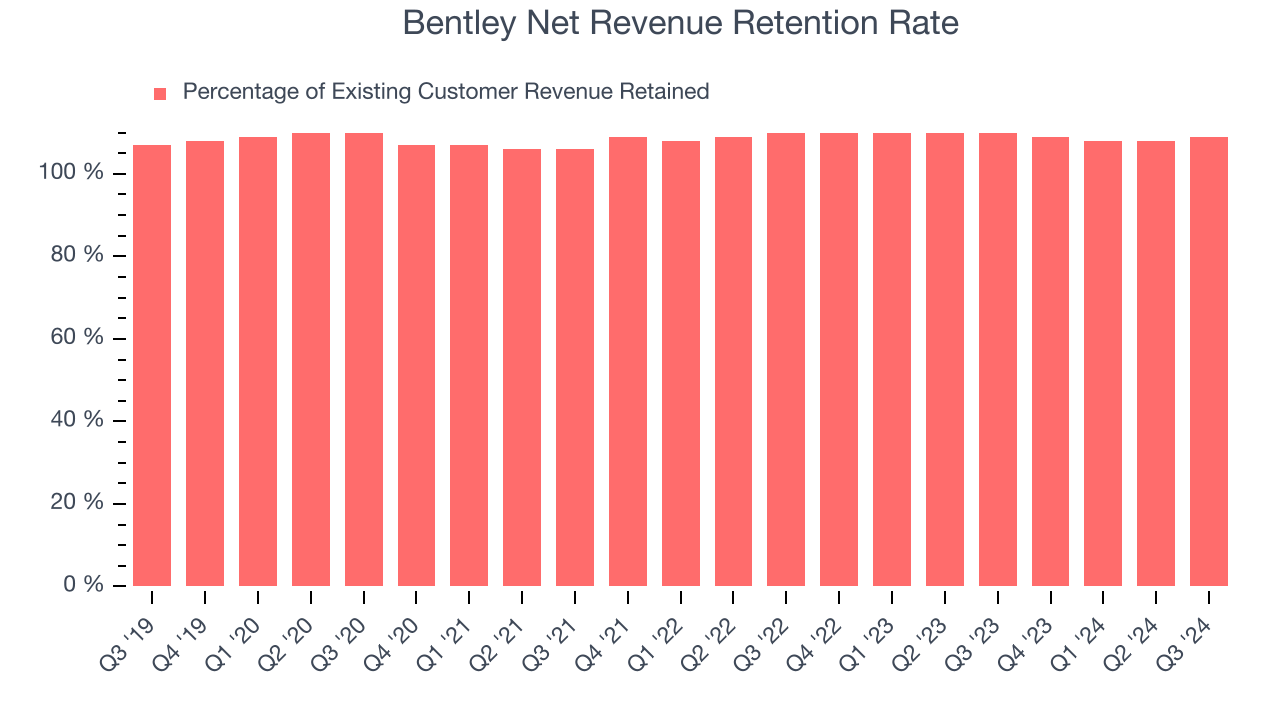

- Net Revenue Retention Rate: 109%, up from 108% in the previous quarter

- Billings: $318.5 million at quarter end, up 11.4% year on year

- Market Capitalization: $15.84 billion

CEO Nicholas Cumins said, “During my first 100 days as CEO, we unveiled ambitious strategic moves that will help propel our future growth: the acquisition of 3D geospatial company Cesium; a strategic partnership with Google to integrate their geospatial content; a new product portfolio for asset analytics and a new generation of engineering applications, both leveraging AI and digital twin technologies to improve the way infrastructure is designed, built, and operated. At the same time, we delivered strong quarterly operating results. Our year-over-year ARR growth on a constant currency basis accelerated to 12% in 24Q3 (12.5% excluding China). Strength was broad based across geographies and sectors as we continued to operate at a high level of performance, with favorable end-market conditions for the foreseeable future.”

Company Overview

Founded by brothers Keith and Barry Bentley, Bentley Systems (NASDAQ:BSY) offers a software-as-a-service platform that addresses the lifecycle of infrastructure projects such as road networks, tunnel systems, and wastewater facilities.

Vertical Software

Software is eating the world, and while a large number of solutions such as project management or video conferencing software can be useful to a wide array of industries, some have very specific needs. As a result, vertical software, which addresses industry-specific workflows, is growing and fueled by the pressures to improve productivity, whether it be for a life sciences, education, or banking company.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Regrettably, Bentley’s sales grew at a sluggish 12.7% compounded annual growth rate over the last three years. This shows it failed to expand in any major way, a rough starting point for our analysis.

This quarter, Bentley’s revenue grew 9.3% year on year to $335.2 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 11.9% over the next 12 months, similar to its three-year rate. This projection is above the sector average and shows the market thinks its newer products and services will help sustain its historical top-line performance.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Annual Recurring Revenue

Investors interested in Bentley should track its annual recurring revenue (ARR) in addition to reported revenue. While reported revenue for a SaaS company can include low-margin items like implementation fees, ARR is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Over the last year, Bentley’s ARR growth has slightly outpaced the sector, averaging 11.8% year-on-year increases and punching in at $1.27 billion in the latest quarter. This alternate topline metric has been growing faster than revenue, which likely means that the recurring portions of the business are growing faster than less predictable, choppier ones such as implementation fees. That could be a good sign for future revenue growth.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Bentley’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 109% in Q3. This means that even if Bentley didn’t win any new customers over the last 12 months, it would’ve grown its revenue by 8.5%.

Bentley has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

Key Takeaways from Bentley’s Q3 Results

It was good to see Bentley beat analysts’ ARR expectations this quarter. On the other hand, its revenue, billings, EPS, and EBITDA missed analysts’ expectations. Overall, this quarter could have been better. The stock traded down 2.2% to $48.80 immediately after reporting.

The latest quarter from Bentley’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.