Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Xylem (NYSE: XYL) and the best and worst performers in the water infrastructure industry.

Trends towards conservation and reducing groundwater depletion are putting water infrastructure and treatment products front and center. Companies that can innovate and create solutions–especially automated or connected solutions–to address these thematic trends will create incremental demand and speed up replacement cycles. On the other hand, water infrastructure and treatment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 5 water infrastructure stocks we track reported a very strong Q2. As a group, revenues beat analysts’ consensus estimates by 4.1%.

Thankfully, share prices of the companies have been resilient as they are up 7.9% on average since the latest earnings results.

Xylem (NYSE: XYL)

Formed through a spinoff, Xylem (NYSE: XYL) manufactures and services engineered products across a wide variety of applications primarily in the water sector.

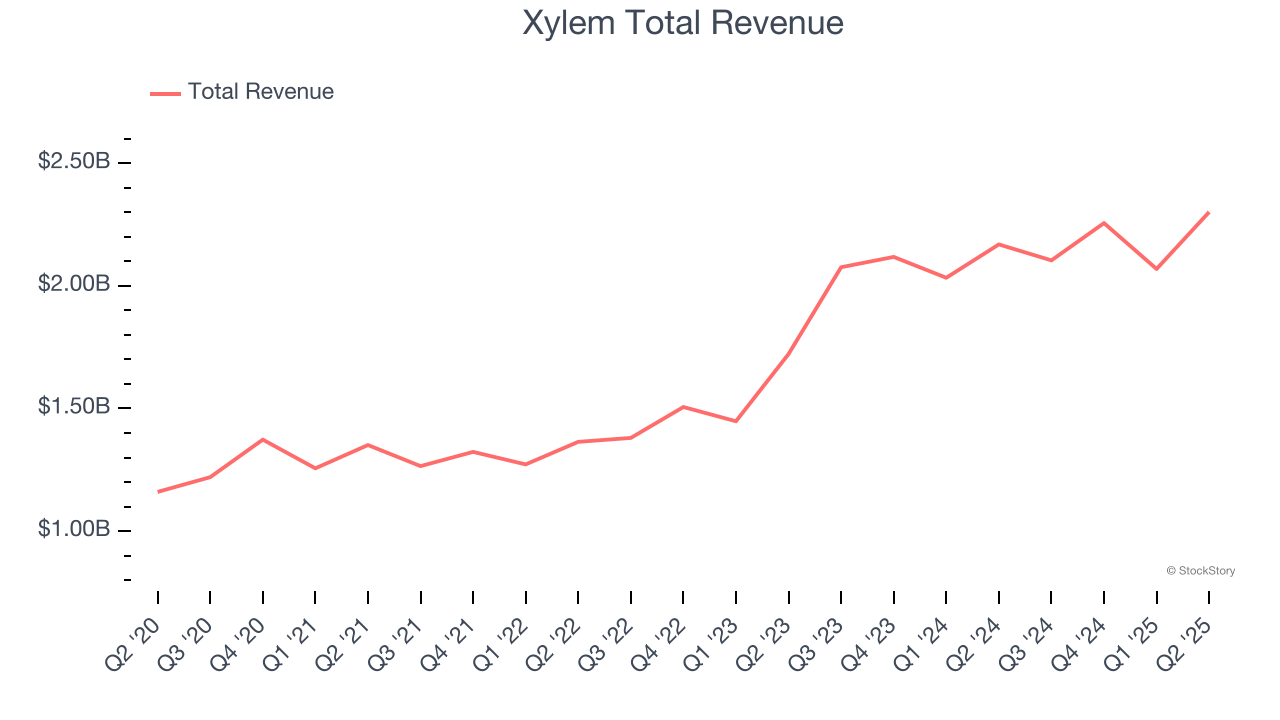

Xylem reported revenues of $2.30 billion, up 6.1% year on year. This print exceeded analysts’ expectations by 4.2%. Overall, it was a stunning quarter for the company with an impressive beat of analysts’ organic revenue estimates and a solid beat of analysts’ EBITDA estimates.

“Our team delivered another strong quarter, exceeding expectations with robust organic revenue growth across all segments, a record-high adjusted EBITDA margin, and double-digit EPS growth,” said Matthew Pine, Xylem’s president and CEO.

Xylem pulled off the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 14.7% since reporting and currently trades at $149.85.

Is now the time to buy Xylem? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q2: Energy Recovery (NASDAQ: ERII)

Having saved far more than a trillion gallons of water, Energy Recovery (NASDAQ: ERII) provides energy recovery devices to the water treatment, oil and gas, and chemical processing sectors.

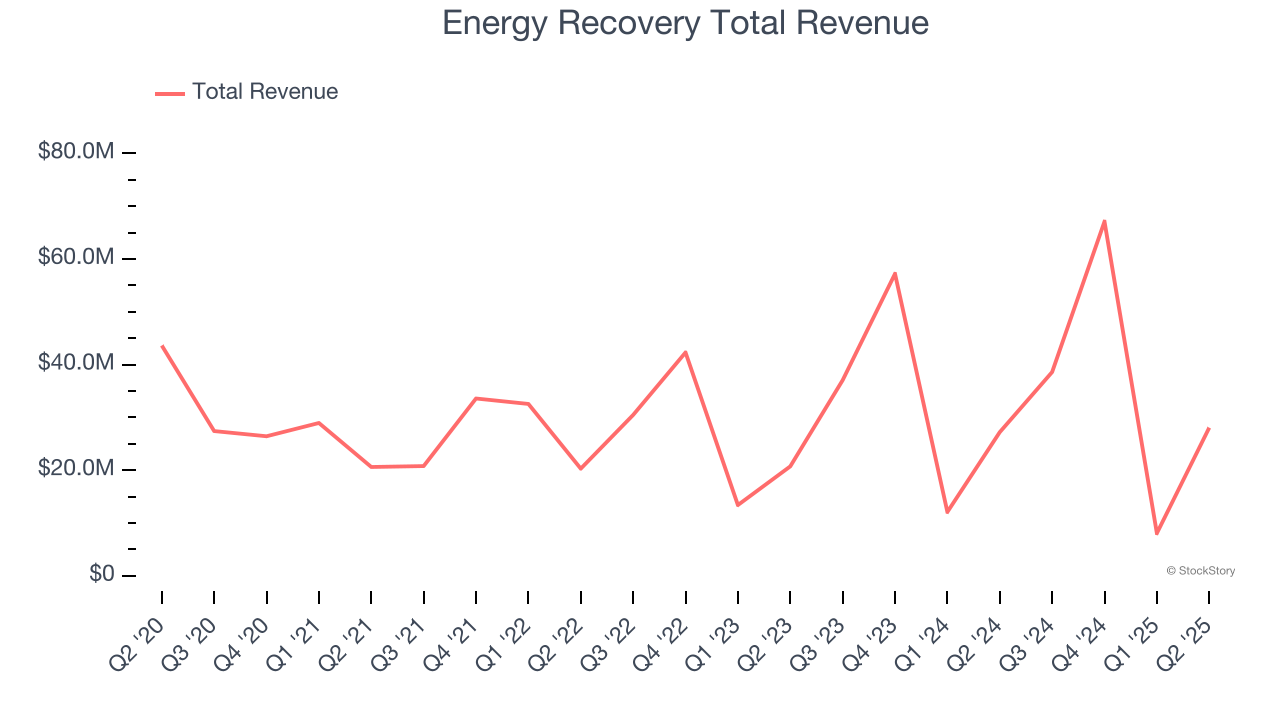

Energy Recovery reported revenues of $28.05 million, up 3.1% year on year, outperforming analysts’ expectations by 10.3%. The business had an incredible quarter with a beat of analysts’ EPS and EBITDA estimates.

Energy Recovery pulled off the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 7% since reporting. It currently trades at $14.56.

Is now the time to buy Energy Recovery? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q2: Tennant (NYSE: TNC)

As the world’s largest manufacturer of autonomous mobile robots, Tennant (NYSE: TNC) designs, manufactures, and sells cleaning products to various sectors.

Tennant reported revenues of $318.6 million, down 3.7% year on year, falling short of analysts’ expectations by 2.6%. It was a softer quarter as it posted a significant miss of analysts’ EPS and EBITDA estimates.

Tennant delivered the weakest performance against analyst estimates, slowest revenue growth, and weakest full-year guidance update in the group. The stock is flat since the results and currently trades at $82.81.

Read our full analysis of Tennant’s results here.

Mueller Water Products (NYSE: MWA)

As one of the oldest companies in the water infrastructure industry, Mueller (NYSE: MWA) is a provider of water infrastructure products and flow control systems for various sectors.

Mueller Water Products reported revenues of $380.3 million, up 6.6% year on year. This print surpassed analysts’ expectations by 3.4%. It was a very strong quarter as it also put up an impressive beat of analysts’ organic revenue estimates and full-year EBITDA guidance beating analysts’ expectations.

The stock is up 8.4% since reporting and currently trades at $25.96.

Read our full, actionable report on Mueller Water Products here, it’s free for active Edge members.

Watts Water Technologies (NYSE: WTS)

Founded in 1874, Watts Water (NYSE: WTS) specializes in manufacturing water products and systems for residential, commercial, and industrial applications globally.

Watts Water Technologies reported revenues of $643.7 million, up 7.8% year on year. This number beat analysts’ expectations by 5%. Overall, it was a stunning quarter as it also logged an impressive beat of analysts’ organic revenue estimates and a solid beat of analysts’ EBITDA estimates.

Watts Water Technologies delivered the fastest revenue growth among its peers. The stock is up 9.1% since reporting and currently trades at $288.36.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.