The September NFP was so smoking hot that it blew the outlook for interest rates out of the water. The headline figure alone was enough to alter the outlook, signaling healthy, resilient labor market conditions, and the revisions sealed the deal. Revisions averaged 72,000 higher monthly in July and August, belying fears that a recession was near. The takeaway for investors is that the FOMC is unlikely to continue with aggressive interest rate cuts and may even pause due to labor market health. Their dual mandate is in balance with labor markets showing strength, inflation trending quickly toward 2%, and the risk of inflationary acceleration back on the table.

Wage Growth Soars in September: Labor Market at an Inflection Point

Not only was job creation strong, but wage growth was robust. The average hourly wage rose by $0.13 with revisions, up 0.4% monthly and 4.0% compared to last year. The data is trending higher, with YoY wage-level inflation back at 4.0%, sufficient to give the FOMC reason to pause. The not-adjusted as-reported data is more compelling, with monthly gains at 0.8% and 4.5% YoY, suggesting sustained consumer health through the holiday season.

As reported by Challenger, Gray & Christmas, hiring intent is also strong. The 403,891 job openings announced in September are seasonally expected and show sustained labor market strength. However, only some of the news is good. The Challenger, Gray & Christmas report also shows the labor market at an inflection point where Senior Vice President Andrew Challenger says it could begin to stall or contract.

The most telling data points are the surge in job cuts, hiring intent, and trends. The 72,821 job cuts announced in September are up 53% compared to September 2023, hiring intent is down compared to last year, and September is the first month 2024 figures surpassed 2023. The 2024 YTD total is only 0.8% above 2023, but it is trending in the wrong direction and could lead to labor market contraction. Regarding the GDP outlook, the Atlanta Fed’s GDPNow tool continues to track in the 2.75% range, well above the analyst consensus and the forecasts for the year.

Overly Optimistic Market Still Expects Two More Cuts By December

The outlook for FOMC interest rate cuts, as forecasted by the CME’s FedWatch Tool, has softened but continues to price at an aggressive pace. The market is pricing in 100% chance for 25 basis points in November and December and another 100 bps by the end of the following year. While cuts will likely continue, the pace will likely be slower than what is currently priced in. The next FOMC meeting is weeks away, with numerous data points still due, including a reading of PCE and the CPI.

Oil has reemerged as a threat to inflation. The oil price is trading near the bottom of its long-term range but showing a clear bottom driven by geopolitical tensions. The market is well-supplied, but there is a significant risk of disruption in the Middle East, and price action in WTI is set to move higher, given the catalyst.

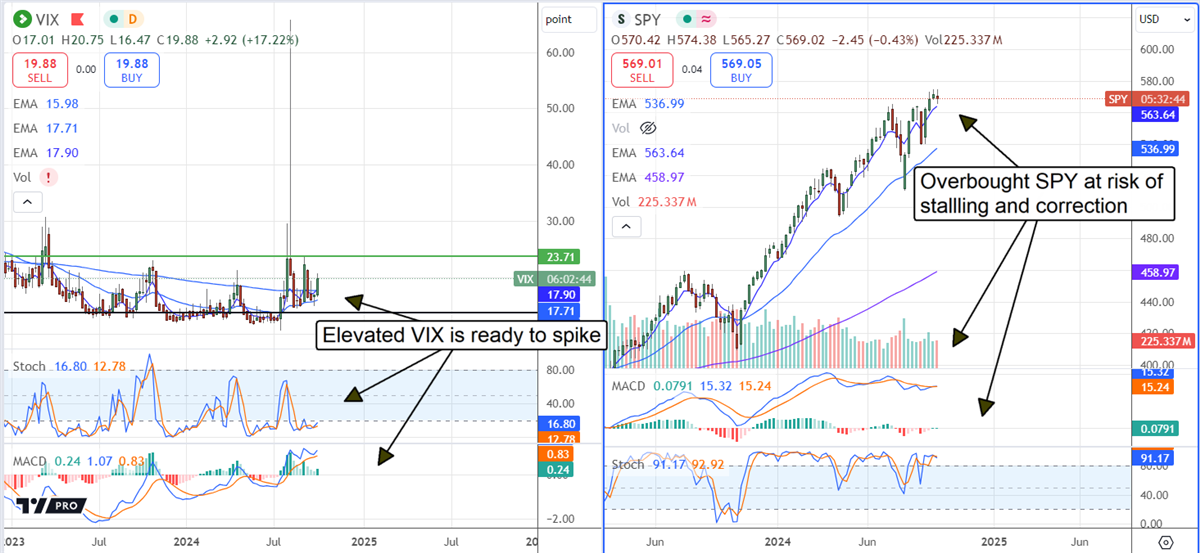

The S&P 500 Stalls Near Record Highs

The S&P 500 (NYSEARCA: SPY) responded favorably to the news, moving higher in early premarket trading, but could not hold the gains. Selling was equally tepid, leaving the market up daily but showing resistance at a critical level, just below the record highs. The takeaway is that market action remains mixed, with no clear indication of direction, and risk is skewed to the downside. As the VIX (CBOE: VIX) indicates, the risk of a major correction remains elevated, with the fear index trading well above the 2024 lows and indicated higher.