8x8 currently trades at $3.10 per share and has shown little upside over the past six months, posting a middling return of 4.4%. The stock also fell short of the S&P 500’s 13% gain during that period.

Is there a buying opportunity in 8x8, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.We're cautious about 8x8. Here are three reasons why EGHT doesn't excite us and a stock we'd rather own.

Why Do We Think 8x8 Will Underperform?

Founded in 1987, 8x8 (NYSE:EGHT) provides software for organizations to efficiently communicate and collaborate with their customers, employees, and partners.

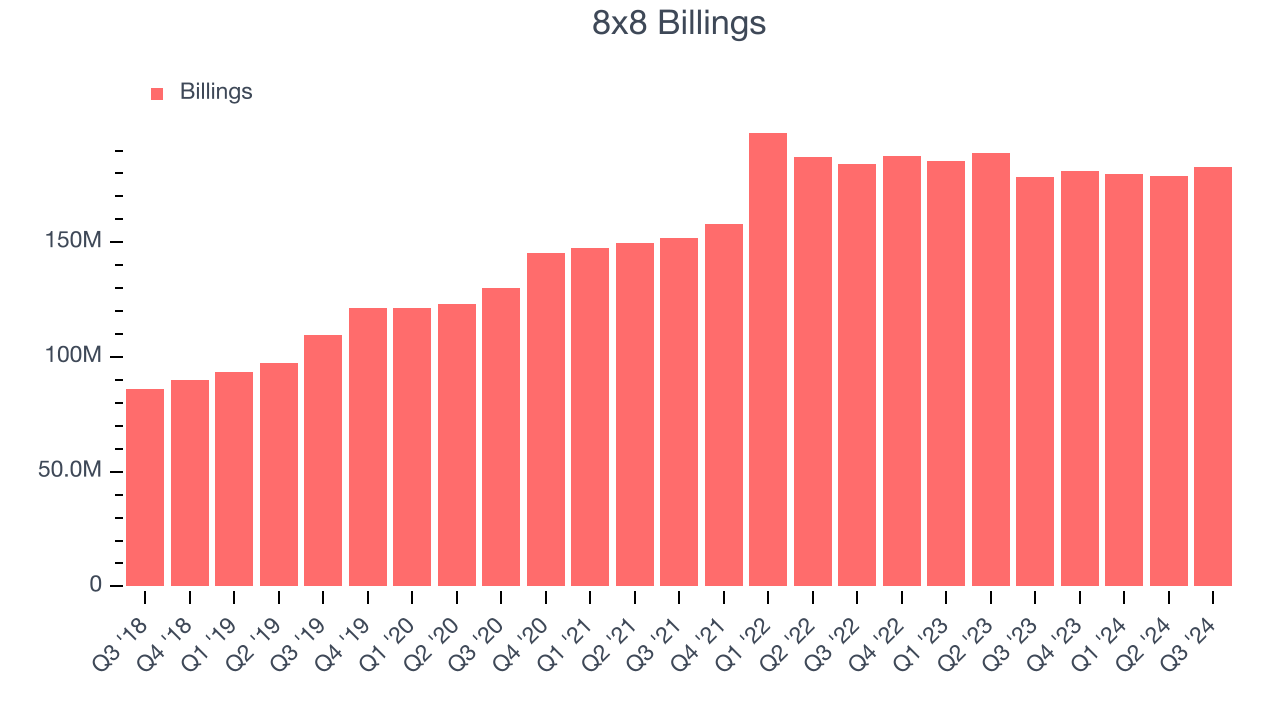

1. Declining Billings Reflect Product and Sales Weakness

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

8x8’s billings came in at $182.6 million in Q3, and it averaged 2.3% year-on-year declines over the last four quarters. This performance was underwhelming and shows the company faced challenges in acquiring and retaining customers. It also suggests there may be increasing competition or market saturation.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Sell-side analysts expect 8x8’s revenue to remain flat over the next 12 months, a deceleration versus its 7.4% annualized growth rate for the last three years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

3. Long Payback Periods Delay Returns

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

8x8’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between 8x8’s products and its peers.

Final Judgment

8x8 falls short of our quality standards. With its shares underperforming the market lately, the stock trades at 0.6x forward price-to-sales (or $3.10 per share). While this valuation is optically cheap, the potential downside is still huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. We’d recommend looking at MercadoLibre, the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of 8x8

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.