First Horizon’s 22.7% return over the past six months has outpaced the S&P 500 by 9%, and its stock price has climbed to $23.93 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy First Horizon, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Why Is First Horizon Not Exciting?

We’re happy investors have made money, but we're swiping left on First Horizon for now. Here are three reasons you should be careful with FHN and a stock we'd rather own.

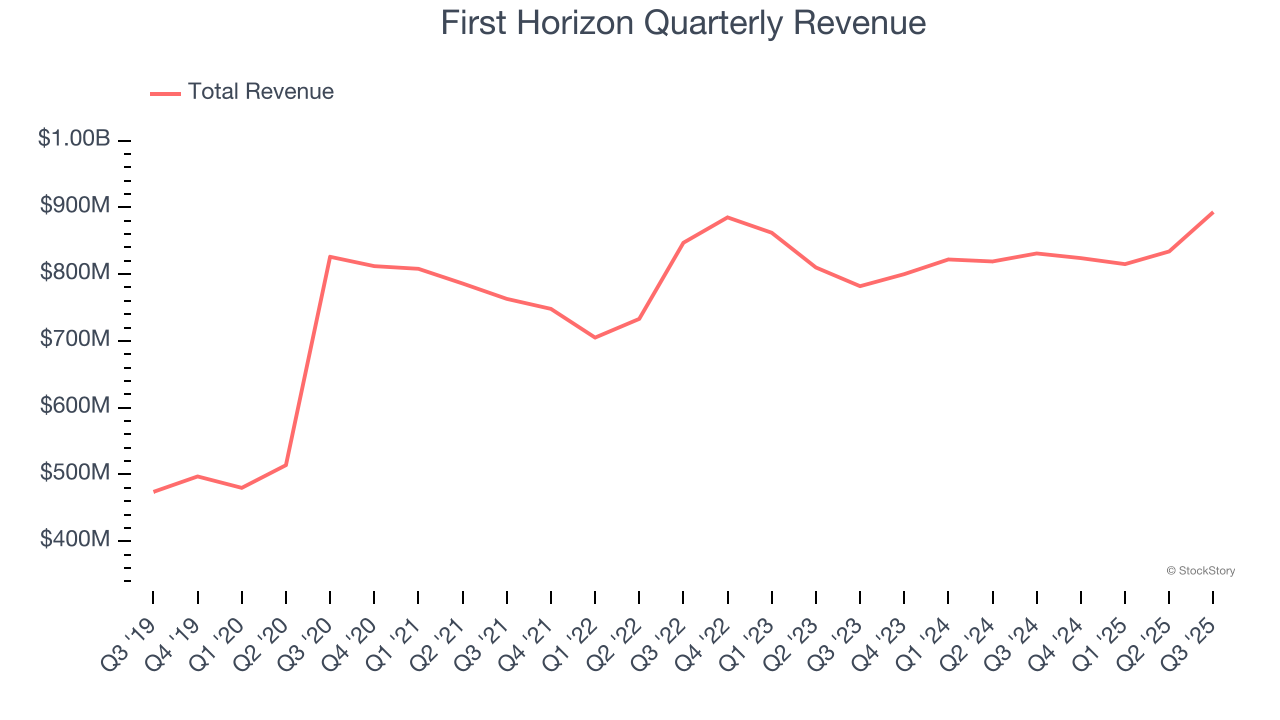

1. Long-Term Revenue Growth Disappoints

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities.

Over the last five years, First Horizon grew its revenue at a tepid 7.8% compounded annual growth rate. This fell short of our benchmark for the banking sector.

2. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect First Horizon’s net interest income to rise by 2%.

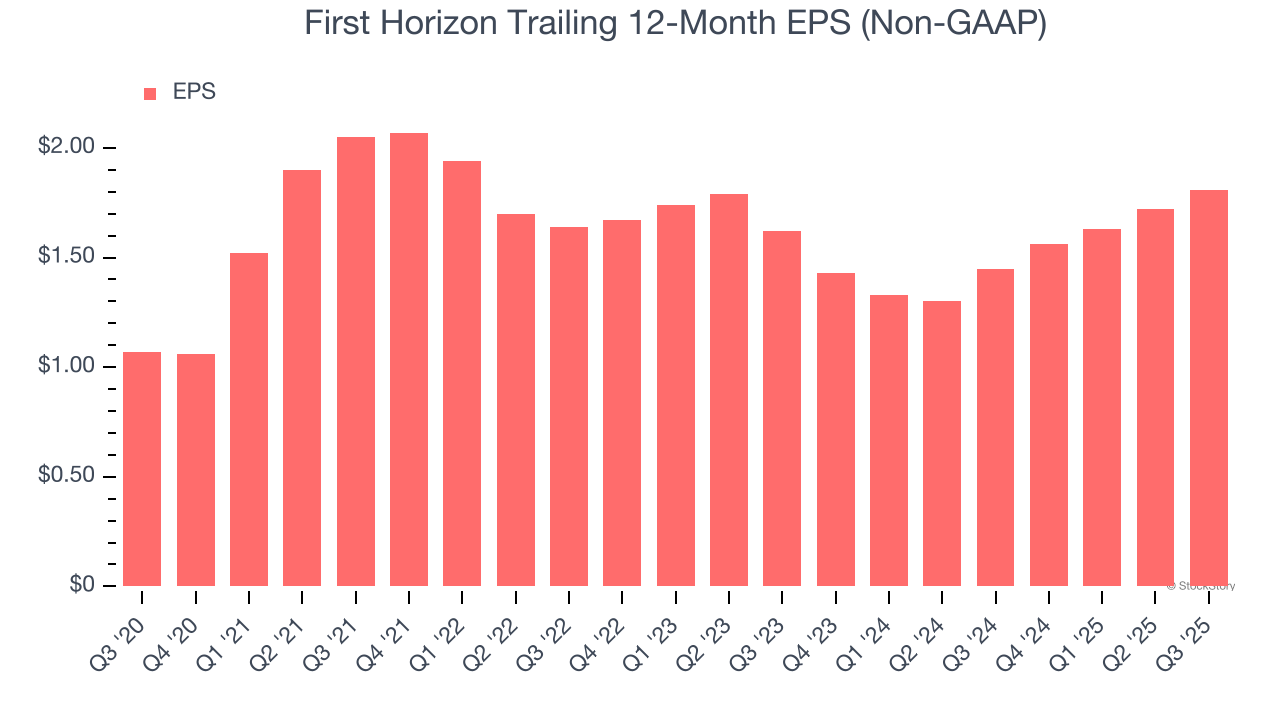

3. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

First Horizon’s EPS grew at a weak 5.7% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its flat revenue and tells us management responded to softer demand by adapting its cost structure.

Final Judgment

First Horizon’s business quality ultimately falls short of our standards. With its shares outperforming the market lately, the stock trades at 1.3× forward P/B (or $23.93 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere. We’d recommend looking at our favorite semiconductor picks and shovels play.

Stocks We Like More Than First Horizon

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.